ECOC 2019 industry reflections

Gazettabyte is asking industry figures for their thoughts after attending the recent ECOC show, held in Dublin. In particular, what developments and trends they noted, what they learned and what, if anything, surprised them. Here are the first responses from Huawei, OFS Fitel and ADVA.

James Wangyin, senior product expert, access and transmission product line at Huawei

At ECOC, one technology that is becoming a hot topic is machine learning. There is much work going on to model devices and perform optimisation at the system level.

And while there was much discussion about 400-gigabit and 800-gigabit coherent optical transmissions, 200-gigabit will continue to be the mainstream speed for the coming three-to-five years.

That is because, despite the high-speed ports, most networks are not being run at the highest speed. More time is also needed for 400-gigabit interfaces to mature before massive deployment starts.

BT and China Telecom both showed excellent results running 200-gigabit transmissions in their networks for distances over 1,000km.

We are seeing this with our shipments; we are experiencing a threefold year-on-year growth in 200-gigabit ports.

Another topic confirmed at ECOC is that fibre is a must for 5G. People previously expressed concern that 5G would shrink the investment of fibre but many carriers and vendors now agree that 5G will boost the need for fibre networks.

As for surprises at the show, the main discussion seems to have shifted from high-speed optics to system-level or device-level optimisation using machine learning.

Many people are also exploring new applications based on the fibre network.

For example, at a workshop to discuss new applications beyond 5G, a speaker from Orange talked about extending fibre connections to each room, and even to desktops and other devices. Other operators and systems vendors expressed similar ideas.

Verizon discussed, in another market focus talk, its monitoring of traffic and the speed of cars using fibre deployed alongside roads. This is quite impressive.

We are also seeing the trend of using fibre and 5G to create a fully-connected world.

Such applications will likely bring new opportunities to the optical industry.

Two other items to note.

The Next Generation Optical Transport Network Forum (NGOF) presented updates on optical technologies in China. Such technologies include next-generation OTN standardisation, the transition to 200 gigabits, mobile transport and the deployment of ROADMs. The NGOF also seeks more interaction with the global community.

The 800G Pluggable MSA was also present at ECOC. The MSA is also keen for more companies to join.

Daryl Inniss, director, new business development at OFS Fitel

There were many discussions about co-packaged optics, regarding the growth trends in computing and the technology’s use in the communications market.

This is a story about high-bandwidth interfaces and not just about linking equipment but also the technology’s use for on-board optical interconnects and chip-to-chip communications such as linking graphics processing units (GPUs).

I learned that HPE has developed a memory-centric computing system that improves significantly processing speed and workload capacity. This may not be news but it was new to me. Moreover, HPE is using silicon photonics in its system including a quantum dot comb laser, a technology that will come for others.

As for surprises, there was a notable growing interest in spatial-division multiplexing (SDM). The timescale may be long term but the conversations and debate were lively. Two areas to watch are in proprietary applications such as very short interconnects in a supercomputer and for undersea networks where the hyperscalers quickly consume the capacity on any newly commission link.

Lastly, another topic of note was the use of spectrum outside the C-band and extending the C-band itself to increase the data-carrying capacity of the fibre.

Jörg-Peter Elbers, senior vice president, advanced technology, ADVA

Co-packaging optics with electronics is gaining momentum as the industry moves to higher and higher silicon throughput. The advent of 51.2 terabit-per-second (Tbps) top-of-rack switches looks like a good interception point. Microsoft and Facebook also have a co-packaged optics collaboration initiative.

As for coherent, quo vadis? Well, one direction is higher speeds and feeds. What will the next symbol rate be for coherent after 60-70 gigabaud (GBd)? A half-step or a full-step; incremental or leap-frogging? The growing consensus is a full-step: 120-140 GBd.

Another direction for coherent is new applications such as access/ aggregation networks. Yet cost, power and footprint challenges will have to be solved.

Advanced optical packaging, an example being the OIF IC-TROSA project, as well as compact silicon photonics and next-gen coherent DSPs are all critical elements here.

A further issue arising from ECOC is whether optical networks need to deliver more than just bandwidth.

Latency is becoming increasingly important to address time-sensitive applications as well as for advanced radio technologies such as 5G and beyond.

Additional applications are the delivery of precise timing information (frequency, time of day, phase synchronisation) where the existing fibre infrastructure can be used to deliver additional services.

An interesting new field is the use of the communication infrastructure for sensing, with Glenn Wellbrock giving a presentation on Verizon’s work at the Market Focus.

Other topics of note include innovation in fibres and optics for 5G.

With spatial-division multiplexing, interest in multi-core and multi-mode fibre applications have weakened. Instead, more parallel fibres operating in the linear regime appear as an energy-efficient, space-division multiplexing alternative.

Hollow-core fibres are also making progress, offering not only lower latencies but lower nonlinearity compared to standard fibres.

As for optics for 5G, what is clear is that 5G requires more bandwidth and more intelligence at the edge. How network solutions will look will depend on fibre availability and the associated cost.

With eCPRI, Ethernet is becoming the convergence protocol for 5G transport. While grey and WDM (G.metro) optics, as well as next-generation PON, are all being discussed as optical underlay options. Grey and WDM optics offer an unbundling on the fibre/virtual fibre level whereas (TDM-)PON requires bitstream access.

Another observation is that radio “x-haul” [‘x’ being front, mid or back] will continue to play an important role for locations where fibre is nonexistent and uneconomical.

Books in 2018 - Part 2

Some more books consumed in 2018, as recommended by Maxim Kuschnerov and Andrew Schmitt.

Maxim Kuschnerov, senior R&D manager at Huawei.

It is hard to believe the book Fire and Fury: Inside the Trump White House by Michael Wolff was published in 2018. Judging by what has happened since Trump’s inauguration, this recollection of his first days in the White House seems outdated. But it was fun to read while the memory of the election was still fresh. It is hard to judge whether all the book’s sources are truthful but the main message is certainly not too far off.

John Carreyrou’s Bad Blood: Secrets and Lies in a Silicon Valley Startup deals with the rise and fall of Elizabeth Holmes and her infamous blood testing start-up, Theranos. If it wasn’t for the fact that Holmes endangered the lives of thousands of people with her erroneous tests, one could be almost amazed on how she secured $1 billion from investors based on absolutely no technology whatsoever. It is also hard to believe how big chains could go along deploying Theranos tests without qualification of the products or the necessary Food and Drug Administration (FDA) approval.

As a westerner working for Huawei, Henry Kissinger’s On China was an important read to understand better how China sees itself and the world. There is no other nation capable of looking decades ahead like it is the fourth quarter of the next financial year. This is a worthwhile book for anyone wanting to make sense of the world.

Being a huge poker fan, buying the book Poker Brat: Phil Hellmuth’s Autobiography was a no-brainer. Hellmuth has his place in poker history, being one of the youngest World Series of Poker (WSOP) main event winners and the record holder with 15 bracelets. However, the book offers little insight on poker strategy. Or maybe it is the lack of strategy which makes Hellmuth who he is. If someone is really interested in learning from a great poker player, I’d recommend Every Hand Revealed by Gus Hansen. Hansen may have lost more than $20 million in online playing, but his book offers a better view on poker strategy back in the day of the big poker boom, before German maths wizards and game theory optimal strategy rewrote poker rules once again.

If a book has already been turned into a movie starring Brad Pitt, it means I am very late to the party with Michael Lewis’s Moneyball: The Art of Winning an Unfair Game. But being an artificial intelligence and machine-learning aficionado, everything is about recognising the underlying patterns, whether it is in images, optical signals or in such a beautiful and simple game like baseball. Most likely baseball strategists already apply machine learning to further optimise their strategy.

Andrew Schmitt, Founder and directing analyst at Cignal AI

The Winter Fortress: The Epic Mission to Sabotage Hitler's Atomic Bomb by Neal Bascomb is my pick of the year. I can’t believe this story isn't already a movie. It is about the Allies’ attempt to destroy the heavy-water plant in German-occupied Norway that was critical to the development of a German Atomic Weapon. Norwegians in exile in the UK, working with locals, pulled off a stunning attack that crippled the plant and set back the German effort. But the book is mostly about the events leading up to the mission, as well as the escape afterwards. The men who pulled it off were as hardcore as they come, and the sacrifices and impossible decisions they faced need to be shared. It is a story I imagine most Norwegians know, and it is a story that should be told to the world.

Hillbilly Elegy: A Memoir of a Family and Culture in Crisis by J.D. Vance is a good autobiography of someone who managed to escape people and situations that could easily have misdirected him. I am not going to join the chorus of folks who point to this book as reasoning for Trump getting elected; I avoid political discussions at all costs in a work environment. But reading this makes you appreciate the positive advantages you may have had growing up. The author, on the surface, had none but he highlights the people and situations that were formative for him and how they guided him on the right path. The best part about the book is that it isn’t preachy and Vance goes out of his way to explain that the problems he avoided have no easy or clear solutions.

Ray Dalio’s whitepapers, essays and explainer videos have always impressed me with concise formats and clear ideas. However, his book, Principles: Life and Work, is a big meal that I didn’t finish. I would recommend his YouTube videos and whitepapers and unless you are a hardcore self-help reader, which I’m not, then skip this.

My son had to read War by Sebastian Junger over the summer for High School. We read it together; a highly recommended thing to do with your teenagers. Junger was embedded in the Korengal Valley in Afghanistan with the US Army and was in the thick of some of the worst fighting. He also wrote The Perfect Storm which was a great book (and a terrible movie). In this book, he brings you right in the midst of events. If you want to know what being at the sharp end in Afghanistan is like, and the physical and mental sacrifices soldiers are making, then read this.

Michael Lewis is one of my favourite authors so I had to read his latest book, The Fifth Risk. It is well-written but it is about politics. I’m tired of politics. I don't think we need more of it so I won't recommend it.

I ripped through two volumes of Martha Wells’s The Murderbot Diaries on the way back from China. It’s about a security robot that figures out how to disable its governor software and become self-aware. A killing machine with a conscience, struggling with the details of being human. Some of the best Sci-Fi I’ve read in a long time. Netflix or Amazon need to give their money to this author right now and turn it into a series.

400ZR will signal coherent’s entry into the datacom world

- 400ZR will have a reach of 80km and a target power consumption of 15W

- The coherent interface will be available as a pluggable module that will link data centre switches across sites

- Huawei expects first modules to be available in the first half of 2020

- At OFC, Huawei announced its own 250km 400-gigabit single-wavelength coherent solution that is already being shipped to customers

Coherent optics will finally cross over into datacom with the advent of the 400ZR interface. So claims Maxim Kuschnerov, senior R&D manager at Huawei.

Maxim Kuschnerov400ZR is an interoperable 400-gigabit single-wavelength coherent interface being developed by the Optical Internetworking Forum (OIF).

Maxim Kuschnerov400ZR is an interoperable 400-gigabit single-wavelength coherent interface being developed by the Optical Internetworking Forum (OIF).

The 400ZR will be available as a pluggable module and as on-board optics using the COBO specification. The IEEE is also considering a proposal to adopt the 400ZR specification, initially for the data-centre interconnect market. “Once coherent moves from the OIF to the IEEE, its impact in the marketplace will be multiplied,” says Kuschnerov.

But developing a 400ZR pluggable represents a significant challenge for the industry. “Such interoperable coherent 16-QAM modules won’t happen easily,” says Kuschnerov. “Just look at the efforts of the industry to have PAM-4 interoperability, it is a tremendous step up from on-off keying.”

Despite the challenges, 400ZR products are expected by the first half of 2020.

400ZR use cases

The web-scale players want to use the 400ZR coherent interface to link multiple smaller buildings, up to 80km apart, across a metropolitan area to create one large virtual data centre. This is a more practical solution than trying to find a large enough location that is affordable and can be fed sufficient power.

Once coherent moves from the OIF to the IEEE, its impact in the marketplace will be multiplied

Given how servers, switches and pluggables in the data centre are interoperable, the attraction of the 400ZR is obvious, says Kuschnerov: “It would be a major bottleneck if you didn't have [coherent interface] interoperability at this scale.”

Moreover, the advent of the 400ZR interface will signal the start of coherent in datacom. Higher-capacity interfaces are doubling every two years or so due to the webscale players, says Kuschnerov, and with the advent of 800-gigabit and 1.6-terabit interfaces, coherent will be used for ever-shorter distances, from 80km to 40km and even 10km.

At 10km, volumes will be an order of magnitude greater than similar-reach dense wavelength-division multiplexing (DWDM) interfaces for telecom. “Datacom is a totally different experience, and it won’t work if you don’t have a stable supply base,” he says. “We see the ZR as the first step combining coherent technology and the datacom mindset.”

Data centre players will plug 400ZR modules into their switch-router platforms, avoiding the need to interface the switch-router to a modular, scalable DWDM platform used to link data centres.

The 400ZR will also find use in telecom. One use case is backhauling residential traffic over a cable operator’s single spans that tend to be lossy. Here, ZR can be used at 200 gigabits - using 64 gigabaud signalling and QPSK modulation - to extend the reach over the high-loss spans. Similarly, the 400ZR can also be used for 5G mobile backhaul, aggregating multiple 25-gigabit streams.

Another application is for enterprise connectivity over distances greater than 10km. Here, the 400ZR will compete with direct-detect 40km ER4 interfaces.

Having several use cases, not just data-centre interconnect, is vital for the success of the 400ZR. “Extending ZR to access and metro-regional provides the required diversity needed to have more confidence in the business case,” says Kuschnerov.

The 400ZR will support 400 gigabits over a single wavelength with a reach of 80km, while the target power consumption is 15W.

The industry is still undecided as to which pluggable form factor to use for 400ZR. The two candidates are the QSFP-DD and the OSFP. The QSFP-DD provides backward compatibility with the QSFP+ and QSFP28, while the OSFP is a fresh design that is also larger. This simplifies the power management at the expense of module density; 32 OSFPs can fit on a 1-rack-unit faceplate compared to 36 QSFP-DD modules.

The choice of form factor reflects a broader industry debate concerning 400-gigabit interfaces. But 400ZR is a more challenging design than 400-gigabit client-side interfaces in terms of trying to cram optics and the coherent DSP within the two modules while meeting their power envelopes.

The OSFP is specified to support 15W while simulation results published at OFC 2018 suggest that the QSFP-DD will meet the 15W target. Meanwhile, the 15W power consumption will not be an issue for COBO on-board optics, given that the module sits on the line card and differs from pluggables in not being confined within a cage.

Kuschnerov says that even if it proves that only the OSFP of the two pluggables supports 400ZR, the interface will still be a success given that a pluggable module will exist that delivers the required face-plate density.

400G coherent

Huawei announced at OFC 2018 its own single-wavelength 400-gigabit coherent technology for use with its OptiX OSN 9800 optical and packet OTN platform, and it is already being supplied to customers.

The 400-gigabit design supports a variety of baud rates and modulation schemes. For a fixed-grid network, 34 gigabaud signalling enables 100 gigabits using QPSK, and 200 gigabits using 16-QAM, while at 45 gigabaud 200 gigabits using 8-QAM is possible. For flexible-grid networks, 64 gigabaud is used for 200-gigabit transmission using QPSK and 400 gigabits using 16-QAM.

Huawei uses an algorithm called channel-matched shaping to improve optical performance in terms of data transmission and reach. This algorithm includes such techniques as pre-emphasis, faster-than-Nyquist, and Nyquist shaping. According to Kuschnerov, the goal is to squeeze as much capacity out of a network’s physical channel so that advanced coding techniques such as probabilistic constellation shaping can be used to the full. For Huawei’s first 400-gigabit wavelength solution, constellation shaping is not used but this will be added in its upcoming coherent designs.

Huawei has already demonstrated the transmission of 400 gigabits over 250km of fibre. “Current generation 400G-per-lambdas does not enable long-haul or regional transmission so the focus is on shorter reach metro or data-centre-interconnect environments,” says Kuschnerov.

When longer reaches are needed, Huawei can offer two line cards, each supporting 200 gigabits, or a single line card hosting two 200-gigabit modules. The 200-gigabits-per-wavelength is achieved using 64 gigabaud and QPSK modulation, resulting in a 2,500km reach.

Up till now, such long-haul distances have been served using 100-gigabitwavelengths. Now, says Kuschnerov, 200 gigabit at 64 gigabaud is becoming the new norm in many newly built networks while the 34 gigabaud 200 gigabit is being favoured in existing networks based on a 50GHz grid.

Telefónica tackles video growth with IP-MPLS network

- Telefónica’s video growth in one year has matched nine years of IP traffic growth

- Optical mesh network in Barcelona will use CDC-ROADMs and 200-gigabit coherent line cards

Telefónica has started testing an optical mesh network in Barcelona, adding to its existing optical mesh deployment across Madrid. Both mesh networks are based on 200-gigabit optical channels and high-degree reconfigurable add-drop multiplexers (ROADMs) that are part of the optical infrastructure that underpins the operator’s nationwide IP-MPLS network that is now under construction.

Maria Antonia CrespoThe operator decided to become a video telco company in late 2014 to support video-on-demand and over-the-top streaming video services.

Maria Antonia CrespoThe operator decided to become a video telco company in late 2014 to support video-on-demand and over-the-top streaming video services.

Telefónica realised its existing IP and aggregation networks would not be able to accommodate the video traffic growth and started developing its IP-MPLS network.

“What we are seeing is that the traffic is growing very quickly,” says Maria Antonia Crespo, IP and optical networking director at Telefónica. “In one year we are getting the same

figures as we got from internet traffic in the last nine years.”

The operator is rolling out the IP-MPLS network across Spain. Juniper Networks and Nokia are the suppliers of the IP router equipment, while Huawei and Nokia were chosen to supply the optical networking equipment.

IP-MPLS

Telefónica set about reducing the number of layers and number of hops when designing its IP-MPLS network. “At each hop, we have to invest money if we want to increase capacity,” says Crespo.

The result is an IP-MPLS network comprising four layers (see diagram). The uppermost Layer 1, dubbed HL1, connects the network to the internet world, while HL2 is a backbone transit layer. The HL3 layer is also a transit layer but at the provincial level. Spain is made up of 52 provinces. HL4 is where the services will reside, where Telefonica will deliver such services as Layer 2 and Layer 3 virtual private networks.

Between HL1 and HL2 is a national GMPLS-based photonic mesh, says Crespo, and between HL3 and HL4 there are the metro mesh networks. “Now we are deploying two GMPLS-based mesh networks, in Madrid and Barcelona,” she says. “Then, in the rest of the country, we are deploying [optical] rings.”

Systems requirements

Telefónica says it had several requirements when choosing the optical transport equipment, requirements common to both its backbone and regional networks.

One is the need to scale capacity at 10 gigabits and 100 gigabits, while network availability and robustness are also key. Telefónica says its network is designed to withstand two or more simultaneous fibre failures. “We have long experience with the GMPLS control plane to support different fibre impairments in the network,” says Alberto Colomer, optical technology manager at Telefónica.

The operator also wants its equipment to support high-speed interfaces and more granular rates to allow it to transition away from legacy traffic such as SDH and 1GbE. Operational improvements are another requirement: Telefónica wants to reduce the manual intervention its network needs. Optical time-domain reflectometers (OTDR) are being integrated into the network to monitor the fibre, as is the ability to automatically equalise the different optical channels.

Alberto ColomerLastly, Telefónica is looking to reduce its capital expenditure and operational expense. It is deploying flexible rate 200-gigabit transponders in its Barcelona and Madrid networks and the same line cards will support 400-gigabit and even 1 terabit channels in future, as well as flexible grid to support the most efficient use of a fibre’s spectrum.

Alberto ColomerLastly, Telefónica is looking to reduce its capital expenditure and operational expense. It is deploying flexible rate 200-gigabit transponders in its Barcelona and Madrid networks and the same line cards will support 400-gigabit and even 1 terabit channels in future, as well as flexible grid to support the most efficient use of a fibre’s spectrum.

The 200-gigabit transponders use 16-quadrature amplitude modulation (16-QAM). Such transponders have enough reach to span each of the two cities but Colomer says Telefónica is still studying how many ROADM stages the 16-QAM transponders can cross.

It is like a pilot changing the engines while flying a plane

The ROADMs Telefónica is deploying in Madrid are directionless and are able to support up to 20 degrees. “You need some connectivity inside the mesh but also the mesh has to be connected to rings that cover all the counties around Madrid,” says Colomer.

Barcelona will be the first location where the ROADMs will also be colourless and contentionless (CDC-ROADMs). “We need to understand in a better way what are the advantages that come with that functionality,” says Colomer.

Telefónica has deployed Huawei’s Optix OSN 9800 platform in Madrid while in Barcelona Nokia’s 1830 Photonic Service Switch with the latest PSE-2 Coherent DSP-ASIC technology is being deployed.

Nokia’s PSS-1830 is designed to support the L-band as well as the C-band but Telefonica does not see the need for the L-band in the near future. “We are going in the direction of increasing capacity per channel: 400-gigabit channels and one terabit channels,” says Colomer. By deploying a photonic mesh and high-degree ROADMs, it will also be possible to increase capacity on a specific link by adding a fibre pair.

Status

The mesh in Madrid is already completed while Telefónica is deploying optical rings around Barcelona while it tests the contentionless ROADMs. These deployments are aligned with the IP-MPLS deployment, says Crespo, which is expected to be completed by 2018.

Crespo says the nationwide IP-MPLS rollout is a challenge. The deployment involves learning new technology that needs to be deployed alongside its existing network. "My boss likens it to a pilot changing the engines while flying a plane," says Crespo. "We are testing in the labs, duplicating it [the network], and migrating the traffic without impacting the customer."

Huawei joins imec to research silicon photonics

Huawei has joined imec, the Belgium nano-electronics research centre, to develop optical interconnect using silicon photonics technology. The strategic agreement follows Huawei's 2013 acquisition of former imec silicon photonics spin-off, Caliopa.

Source: Gazettabyte

Source: Gazettabyte

“Having acquired cutting-edge expertise in the field of silicon photonics thanks to our acquisition of Caliopa last year, this partnership with imec is the logical next move towards next-generation optical communication,” says Hudson Liu, CEO at Huawei Belgium.

Imec's research focus is to develop technologies that are three to five years away from production. "Imec works with leading IC manufacturers and fabless companies in the field of CMOS fabrication," says Philippe Absil, department director for 3D and optical technologies at imec. "One of the programmes with our co-partners is about optical interconnect and silicon photonics, and Huawei is one of the participating companies."

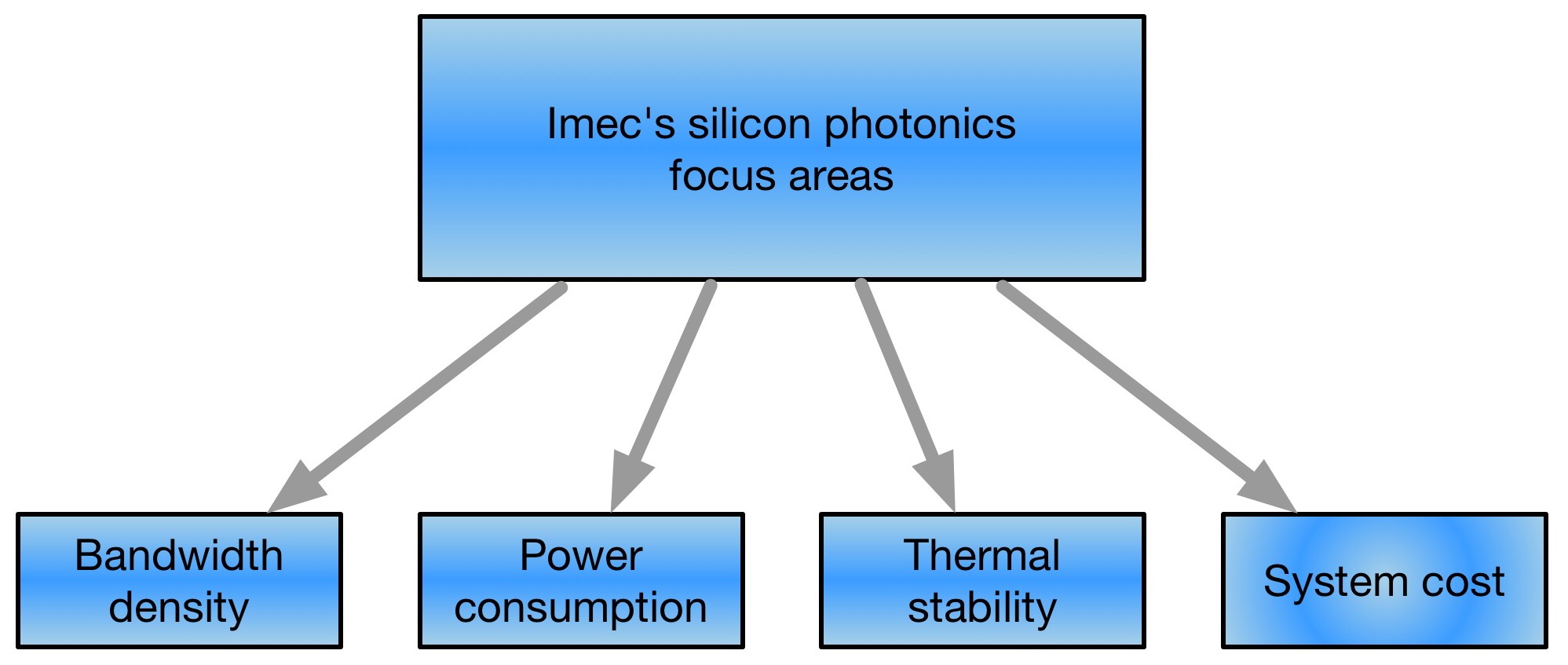

Imec's research concentrates on board-to-board and chip-to-chip interconnect. The optical interconnect work includes increasing interface bandwidth density, reducing power consumption, and achieving thermal stability and system-cost reduction.

The research centre has demonstrated high-bandwidth interfaces as part of work with Chiral Photonics that makes multi-core fibre. Imec has developed a 2D ring of grating couplers that allow coupling between the silicon photonics chip and Chiral's 61-core fibre. "A grating coupler is a sub-wavelength structure that diffracts the light from a waveguide in a vertical direction towards the fibre above the chip," says Absil. This contrasts to traditional edge coupling to a device, achieved by dicing or cleaving a facet on the waveguide, he says.

Another research focus is how to reduce device power consumption and achieve thermal stability. One silicon photonics component that dictates the overall power consumption is the modulator, says Absil. "The Mach-Zehnder modulator is known to consume significant amounts of power for chip-to-chip distances," he says. "The alternative is to use resonating-based modulators but these have to be thermally controlled, and that has an associated power consumption."

Imec is looking at ways to reduce the thermal control needed and is investigating the addition of materials to silicon to create resonator modulators that do away with the need for heating.

The system-cost reduction work looks at packaging. "Eventually, we want to get the optical transceiver inside a host IC," says Absil. "That package has to enable an optical pass-through, whether it is fibre or an optically-transparent package." Such a requirement differs from established CMOS packaging technology. "The programme is also looking to explore new types of packaging for enabling this optical pass-through," he says.

Absil says certain programme elements are two years away from being completed. "In the programme, we have topics that are closer to being adopted and some that are further away, maybe even to 2020."

Multi-project wafer service

Imec is part of the a consortium of EC research institutes that provide low-cost access to companies that don't have the means to manufacture their own silicon photonics designs. Known as Essential, the EC's Seventh Framework (FP7) programme is an extension of the ePIXfab silicon photonics multi-project wafer initiative. "Imec is offering one flavour of the technology, Leti is also offering a flavour, and then there is IHP and VTT," says Absil. Once the Essential FP7 project is completed, the service will be continued by the Europractice IC service.

Has imec seen any growth now that the funding for OpSIS, the multi-project wafer provider, has come to an end? "We see decent contributions but I wouldn't say it is exponential growth," says Absil, who notes that the A*STAR Institute of Microelectronics in Singapore that OpSIS used continues to offer a multi-project wafer service.

Status of silicon photonics

Despite announcements from Acacia and Intel, and Finisar revealing at ECOC '14 that it is now active in silicon photonics, 2014 has been a quiet year for the technology.

"Right now it is a bit quiet because companies are investing in development," says Absil. "There is not so much incentive to publish this work." Another factor he cites for the limited news is that there are vertically-integrated vendors that are putting the technology in their servers rather than selling silicon-photonics products directly.

"This is only first generation," says Absil. "As it picks up, there will be more incentive to work on a second generation of silicon photonics which will depart from what we know from the early work published by Intel and Luxtera."

The opportunities this next-generation technology will offer are 'quite exciting', says Absil.

Is the tunable laser market set for an upturn?

Part 2: Tunable laser market

"The tunable laser market requires a lot of patience to research." So claims Vladimir Kozlov, CEO of LightCounting Market Research. Kozlov should know; he has spent the last 15 years tracking and forecasting lasers and optical modules for the telecom and datacom markets.

Source: LightCounting, Gazettabyte

Source: LightCounting, Gazettabyte

The tunable laser market is certainly sizeable; over half a million units will be shipped in 2014, says LightCounting. But the market requires care when forecasting. One subtlety is that certain optical component companies - Finisar, JDSU and Oclaro - are vertically integrated and use their own tunable lasers within the optical modules they sell. LightCounting counts these as module sales rather than tunable laser ones.

Another issue is that despite the development of advanced reconfigurable optical add/ drop multiplexers (ROADMs) and tunable lasers, the uptake of agile optical networking has been limited.

"Verizon is bullish on getting the next generation of colourless, directionless and contentionless ROADMS to reconfigure the network on-the-fly," says Kozlov. "But I'm not so sure Verizon is going to be successful in convincing the industry that this is going to be a good market for [ROADM] suppliers to sell into."

Reconfigurability helps engineers at installations when determining which channels to add or drop, but there is little evidence of operators besides Verizon talking about using ROADMS to change bandwidth dynamically, first in one direction and then the other, he says.

Another indicator of the reduced status of tunable lasers is NeoPhotonics's intention to purchase Emcore's tunable external cavity laser as well as its module assets for US $17.5 million. Emcore acquired the laser when it bought Intel's optical platform division for $85 million in 2007, while Intel acquired it from New Focus in 2002 for $50 million. NeoPhotonics has also spent more in the past: it bought Santur's tunable laser for $39 million in 2011.

"There was so much excitement with so many players [during the optical bubble of 1999-2000], the market was way too competitive and eventually it drove vendors to the point where they would prefer to sell the business for pennies rather than keep it running," says Kozlov. "Emcore has been losing money, it is not a highly profitable business." Yet for Kozlov, Emcore's tunable laser is probably the best in the business with its very narrow line-width compared to other devices.

Tunable laser market

Tunable lasers have failed to get into the mainstream of the industry. "If you look at DWDM, I'm guessing that 70 percent of lasers sold are still fixed wavelength or temperature-tunable over a few wavelengths," says Kozlov. System vendors such as Huawei and ZTE advertise their systems with tunable lasers. "But when we asked them how they are using tunable lasers, they admitted that the bulk of their shipments are fixed-wavelength devices because whatever little they can save on cost, they will."

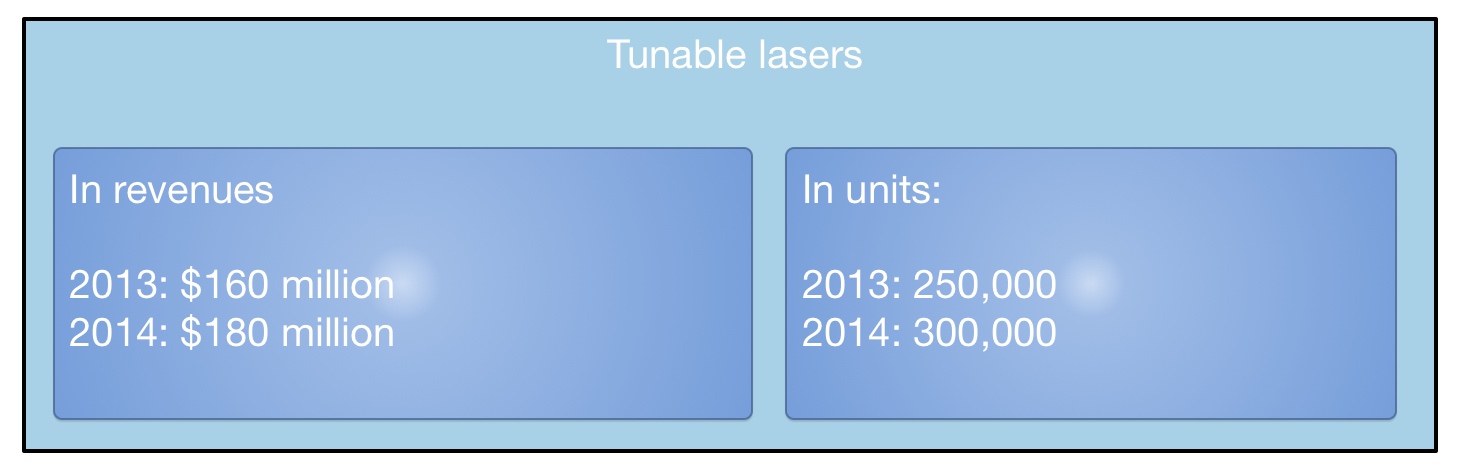

LightCounting valued the 2013 tunable laser market at $160 Million, growing to $180 Million in 2014. This equates to 250,000 units sold in 2013 and 300,000 units this year. "Most of these are for coherent systems," says Kozlov. The number of tunable lasers sold in modules - mainly XFPs but also SFPs and 300-pin modules - is 250,000 million units. "Half a million units a year; if you look at actual shipments, it is quite a lot," says Kozlov.

What next?

"I'm hoping we are reaching the low point in the tunable laser market as vendors are struggling and sales are at a very low valuation," says Kozlov.

The advent of more complex modulation schemes for 400 Gigabit and greater speed optical transmission, and the adoption of silicon photonics-based modulators for long haul will require higher powered lasers. But so much progress has been made by laser designers over the last 15 years, especially during the bubble, that it will last the industry for at least another decade or two, says Kozlov: "Incremental progress will continue and hopefully greater profitability."

For Part 1: NeoPhotonics to expand its tunable laser portfolio, click here

Optical transceiver market to grow 50 percent by 2017

- The optical transceiver market will grow to US $5.1bn in 2017

- The fierce price declines of 2012 will lessen during the forecast period

- Stronger traffic growth could have a significant positive effect on transceiver market growth

"The price declines in 2012 were brutal but they will not happen again [during the forecast period]"

"The price declines in 2012 were brutal but they will not happen again [during the forecast period]"

Vladimir Kozlov, LightCounting

The global optical transceiver market will grow strongly over the next five year to $5.1bn in 2017, from $3.4bn in 2012. So claims market research company, LightCounting, in its latest telecom and datacom forecast.

"That [market value] does not include tunable lasers, wavelength-selective switches, pump lasers and amplifiers which will add some $1bn or $2bn more [in 2017]," says Vladimir Kozlov, CEO of LightCounting.

One key assumption underpinning the forecast is that competitive pressures will ease. "The price declines in 2012 were brutal but they will not happen again [during the forecast period]," says Kozlov.

Optical transceivers

The optical transceiver market saw price declines as high as 30 percent last year. These were not new products ramping in volume where sharp price declines are to be expected, says Kozlov. Last year also saw fierce competition among the service providers while the steepest price declines were experienced by the telecom equipment makers.

One optical transceiver sector that performed well last year is high-speed optical transceivers and in particular Ethernet.

The 100 Gigabit Ethernet (GbE) market saw revenue growth due to strong demand for the 100GBASE-LR4 10km transceiver even though its unit price declined 30 percent. This is a sector the Chinese optical transceiver players are eyeing as they look to broaden the markets they address.

One unheralded market that did well was 40 Gigabit transceivers for telecoms and the data centre. "This is 40 Gig short reach mostly - up to 100m - but also 10km reach transceivers did well in the data centre," says Kozlov.

LightCounting expects the steady growth of 40GbE to continue; 40GbE transceivers use 10 Gig technology co-packaged into one module, offer improved port density and have a lower power and cost compared to four 10GbE transceivers.

Even the veteran 10GbE market continues to grow. Some 7-8M 10GbE short reach and long reach units were sold in 2012 growing to 10M units this year.

Meanwhile, the 100 Gigabit coherent long-haul transponder market was small in 2012. The optical vendors only started selling in volume last year and most of the system vendors manufacture their own 100 Gigabit-per-second (Gbps) designs using discrete components. "Those companies that sell modulators and receivers for 100 Gig did really well in 2012," says Kozlov.

LightCounting expects the 100Gbps coherent transponder market will grow in 2013 as system vendors embrace more third-party 100 Gig transponders. "We estimate that the optical transceiver vendors captured 10-15 percent of the 40 and 100 Gig market and this will grow to 18-20 percent in 2013," says Kozlov.

Other markets that grew in 2012 include optical access. The fibre-to-the-x (FTTx) continues to grow in terms of units shipped, with transceivers and board optical sub-assembly (BOSA) designs sharing the volumes.

LightCounting says that the number of optical network units (ONU) exceeded by more than double the number of FTTx subscribers added in 2012: 35-40M ONU transceivers and BOSAs compared to 15M new subscribers.

The result was a market value of $700M in 2012 compared to $300M in 2009. But because of the excess in shipments compared to new subscribers, Kozlov expects the FTTx market to slow down. "That is probably a sure sign that it is going to grow again," he quips.

Market expectations

Kozlov will be watching how the optical interconnect market does this year. The active optical cable market did well in 2012 and this is likely to continue. Kozlov is interested to see if silicon photonics starts to make its mark in the transceiver market, citing as an example Cisco's in-house silicon photonics-based CPAK transceiver. He also expects the 40G and 100Gbps module makers to do well.

LightCounting stresses the wide discrepancy between video traffic growth through 2017 as forecast by Bell Labs and by Cisco Systems. This is important because the optical transceiver forecast model developed by LightCounting is sensitive to traffic growth. LightCounting has averaged the two forecasts but if video traffic grows more quickly, the overall transceiver market will exceed the market research company's 2017 forecast.

Another reason why Kozlov is upbeat about the market's prospects is that while the system vendors suffered the sharpest price declines - up to 35 percent in 2012 - this will not continue.

The sharp falls in equipment prices were due largely to the fierce competition provided by the Chinese giants Huawei and ZTE. But relief is expected with government initiatives in Europe and the United States to limit the influence of Huawei and ZTE, says Kozlov.

The U.S. government has effectively restricted sales of Huawei and ZTE networking equipment to major U.S. carriers due to cyber security concerns, while the European Commission has determined that Huawei and ZTE are both inflicting damage on European equipment vendors by dumping products onto the European market.

China and the global PON market

China has become the world's biggest market for passive optical network (PON) technology even though deployments there have barely begun. That is because China, with approximately a quarter of a billion households, dwarfs all other markets. Yet according to market research firm Ovum, only 7% of Chinese homes were connected by year end 2011.

"In 2012, BOSAs [board-based PON optical sub-assemblies] will represent the majority versus optical transceivers for PON ONTs and ONUs"

Julie Kunstler, Ovum

Until recently Japan and South Korea were the dominant markets. And while PON deployments continue in these two markets, the rate of deployments has slowed as these optical access markets mature.

According to Ovum, slightly more than 4 million PON optical line terminals (OLTs) ports, located in the central office, were shipped in Asia Pacific in 2011, of which China accounted for the majority. Worldwide OLT shipments for the same period totaled close to 4.5 million. The fact that in China the ratio of OLT to optical network terminal (ONT), the end terminal at the home or building, deployed is relatively low highlights that in the Chinese market the significant growth in PON end terminals is still to come.

The strength of the Chinese market has helped local system vendors Huawei, ZTE and Fiberhome become leading global PON players, accounting for over 85% of the OLTs sold globally in 2011, says Julie Kunstler, principal analayst, optical components at Ovum. Moreover, around 60% of fibre-to-the-x deployments in Europe, Middle East and Africa were supplied by the Chinese vendors. The strongest non-Chinese vendor is Alcatel-Lucent.

Ovum says that the State Grid China Corporation, the largest electric utility company in China, has begun to deploy EPON for their smart grid trial deployments. PON is preferred to wireless technology because of its perceived ability to secure the data. This raises the prospect of two separate PON lines going to each home. But it remains to be seen, says Kunstler, whether this happens or whether the telcos and utilities share the access network.

"After China the next region that will have meaningful numbers is Eastern Europe, followed by South and Central America and we have already seen it in places like Russia,” says Kunstler. Indeed FTTx deployments in Eastern Europe already exceed those in Western Europe.

EPON and GPON

In China both Ethernet PON (EPON) and Gigabit PON (GPON) are being deployed. Ovum estimates that in 2011, 65% of equipment shipments were EPON while GPON represented 35% GPON in China.

China Telecom was the first of the large operators in China to deploy PON and began with EPON. Ovum is now seeing deployments of GPON and in the 3rd quarter of 2012, GPON OLT deployments have overtaken EPON.

China Mobile, not a landline operator, started deployments later and chose GPON. But these GPON deployments are on top of EPON, says Kunstler: "EPON is still heavily deployed by China Telecom, while China Mobile is doing GPON but it is a much smaller player." Moreover, Chinese PON vendors also supplying OLTs that support EPON and GPON, allowing local decisions to be made as to which PON technology is used.

One trend that is impacting the traditional PON optical transceiver market is the growing use of board-based PON optical sub-assemblies (BOSAs). Such PON optics dispenses with the traditional traditional optical module form factor in the interest of trimming costs.

“A number of the larger, established ODMs [original design manufacturers] have begun to ship BOSA-based PON CPEs,” says Kunstler. In 2012, BOSAs will represent the majority versus optical transceivers for PON ONTs/ONUs.” says Kunstler.

10 Gigabit PON

Ovum says that there has been very few deployments of next generation 10G EPON and XG-PON, the 10 Gigabit version of GPON.

"There have been small amounts of 10G [EPON] in China," says Kunstler. "We are talking hundreds or thousands, not the tens of thousands [of units]."

One reason for this is the relative high cost of 10 Gigabit PON which is still in its infancy. Another is the growing shift to deploy fibre-to-the-home (FTTh) versus fibre-to-the-building deployments in China. 10 Gigabit PON makes more sense in multi-dwelling units where the incoming signal is split between apartments. Moving to 10G EPON boosts the incoming bandwidth by 10x while XG-PON would increase the bandwidth by 4x. "The need for 10 Gig for multi-dwelling units is not as strong as originally thought," says Kunstler.

It is a chicken-and-egg issue with 10G PON, says Kunstler. The price of 10G optics would go down if there was more demand, and if there was more demand, the optical vendors would work on bringing down cost. "10G GPON will happen but will take longer," says Kunstler, with volumes starting to ramp from 2014.

However, Ovum thinks that a stronger market application for 10G PON will be for supporting wireless backhaul. The market research company is seeing early deployments of PON for wireless backhaul especially for small cell sites (e.g. picocells). Small cells are typically deployed in urban areas which is where FTTx is deployed. It is too early to know the market forecast for this application but PON will join the list of communications technologies supporting wireless backhaul.

Challenges

Despite the huge expected growth in deployments, driven by China, challenges remain for PON optical transceiver and chip vendors.

The margins on optics and PON silicon continue to be squeezed. ODMs using BOSAs are putting pricing pressure on PON transceiver costs while the vertical integration strategy of system vendors such as Huawei, which also develops some of its own components squeezes, out various independent players. Huawei has its own silicon arm called HiSilicon and its activities in PON has impacted the chip opportunity of the PON merchant suppliers.

"Depending upon who the customer is, depending upon the pricing, depending on the features and the functions, Huawei will make the decision whether they are using HiSilicon or whether they are using merchant silicon from an independent vendor, for example," says Kunstler.

There has been consolidation in the PON chip space as well as several new players. For example, Broadcom acquired Teknouvs and Broadlight while Atheros acquired Opulan and Atheros was then acquired by Qualcomm. Marvell acquired a very small start-up and is now competing with Atheros and Broadcom. Most recently, Realtek is rumored to have a very low-cost PON chip.

60-second interview with .... Sterling Perrin

Heavy Reading has published a report Photonic Integration, Super Channels & the March to Terabit Networks. In this 60-second interview, Sterling Perrin, senior analyst at the market research company, talks about the report's findings and the technology's importance for telecom and datacom.

"PICs will be an important part of an ensemble cast, but will not have the starring role. Some may dismiss PICs for this reason, but that would be a mistake – we still need them."

Sterling Perrin, Heavy Reading

Heavy Reading's previous report on optical integration was published in 2008. What has changed?

The biggest change has been the rise of coherent detection, bringing electronics to prominence in the world of optics. This is a big shift - and it has taken some of the burden off photonic integration. Simply put, electronics has taken some of the job away from optics.

How important is optical Integration, for optical component players and for system vendors?

Until now, photonic integration has not been a ‘must have’ item for systems suppliers. For the most part, there have been other ways to get at lower costs and footprint reductions.

I think we are starting to see photonic integration move into the must-have category for systems suppliers, in certain applications, which means that it becomes a must-have item for the components companies that supply them.

How should one view silicon photonics and what importance does Heavy Reading attach to Cisco System's acquisition of silicon photonics' startup, Lightwire?

When we published the last [2008] report, silicon photonics was definitely within the hype cycle. We’ve seen the hype fade quite a bit – it’s now understood that just because a component is made with silicon, it’s not automatically going to be cheaper. Also, few in the industry continue to talk about a Moore’s Law for optics today. That said, there are applications for silicon photonics, particularly in data centre and short-reach applications, and the technology has moved forward.

Cisco’s acquisition of Lightwire is a good testament for how far the technology has come. This is a strategic acquisition, aimed at long-term differentiation, and Cisco believes that silicon photonics will help them get there.

"It will be interesting to watch what other [optical integration] M&A activity occurs, and how this activity affects the components players"

What are the main optical integration market opportunities?

In long haul, we already see applications for photonic integrated circuits (PICs). Certainly, Infinera’s PIC-based DTN and DTN-X systems stand out. But also, the OIF has specified photonic integration in its 100 Gigabit long haul, DWDM (dense wavelength division multiplexing) MSA (multi-source agreement) – it was needed to get the necessary size reduction.

Moving forward, there is opportunity for PICs in client-side modules as PICs are the best way to reduce module sizes and improve system density. Then, beyond 100G, to super-channel-based long-haul systems, PICs will play a big role here, as parallel photonic integration will be used to build these super-channels.

Were you surprised by any of the report's findings?

When I start researching a report, I am always hopefully for big black and white kinds of findings – this is the biggest thing for the industry or this is a dud. With photonic integration, we found such a wide array of opinions and viewpoints that, in the end, we had to place photonic integration somewhere in the middle.

It’s clear that system vendors are going to need PICs but it’s also clear that PICs alone won’t solve all the industry’s challenges. PICs will be an important part of an ensemble cast, but will not have the starring role. Some may dismiss PICs for this reason, but that would be a mistake – we still need them.

What optical integration trends/ developments should be watched over the next two years?

The year started with two major system suppliers buying PIC companies: Cisco and Lightwire and Huawei and CIP Technologies. With Alcatel-Lucent having in-house abilities, and, of course, Infinera, this should put pressure on other optical suppliers to have a PIC strategy.

It will be interesting to watch what other M&A activity occurs, and how this activity affects the components players.

The editor of Gazettabyte worked with Heavy Reading in researching photonic integration for the report.

Huawei's novel Petabit switch

The Chinese equipment maker showcased a prototype optical switch at this year's OFC/NFOEC that can scale to 10 Petabit.

"Although the numbers [400,000 lasers] appear quite staggering, they point to a need for photonic integration"

Reg Wilcox, Huawei

Huawei has demonstrated a concept Petabit Packet Cross Connect (PPXC), a switching platform to meet future metro and data centre requirements. The demonstrator is not expected to be a commercial product before 2017.

Current platforms have switching capacities of several Terabits. Yet Huawei believes a one thousand-fold increase in switching capacity will be needed. Fibre capacity will be filled to 20 and eventually 50 Terabits using higher-order modulation schemes and flexible spectrum. This will add up to a Petabit (one million Gigabits) per site, assuming 200 switched fibres at busy network exchanges.

"We are not saying we will introduce a 10 Petabit product in five years' time, although the technology is capable of that," says Reg Wilcox, vice president of network marketing and product management at Huawei. "We will size it to what we deem the market needs at that time."

Source: Huawei

Source: Huawei

The PPXC uses optical burst transmission to implement the switching. Such burst transmission uses ultra-fast switching lasers, each set to a particular wavelength in nanoseconds. Like Intune Networks’ Verisma iVX8000 optical packet switching and transport system, each wavelength is assigned to a particular destination port. As OTN traffic or packets arrive, they are assigned a wavelength before being sent to a destination port.

Huawei's switch demonstration linked two Huawei OSN8800 32-slot platforms, each with an Optical Transport Network (OTN) switching capacity of 2.56 Terabit-per-second (Tbps), to either side of the core optical switch, to implement what is known as a three-stage Clos switching matrix.

With each OSN8800, half the slots are for inter-machine trunks to the core optical switch, the middle stage of the Clos switch. "The other half [of the OSN8800] would be dedicated to whatever services you want to have: Gigabit Ethernet, 10 Gigabit Ethernet; whatever traffic you want riding over OTN," says Wilcox.

The core optical switch implements an 80x80 matrix using 80 wavelengths, each operating at 25Gbps. The 80x80 matrix is surrounded by MxM fast optical switches to implement a larger 320x320 matrix that has an 8 Terabit capacity. It is these larger matrices - 'switch planes' - that are stacked to achieve 10 Petabit. The PPXC grooms traffic starting at 1 Gigabit rates and can switch 100Gbps and even higher speed incoming wavelengths in future.

Oclaro provided Huawei with the ultra-fast lasers for the demonstrator. The laser - a digital supermode-distributed Bragg reflector (DS-DBR) - has an electro-optic tuning mechanism, says Robert Blum, director of product marketing for Oclaro's photonic component. Here current is applied to the grating to set the laser's wavelength. The resulting tuning speed is in nanoseconds although Oclaro will not say the exact switching speed specified for the switch.

Each switch plane uses 4x80 or 320, 25Gbps lasers. A 10 Petabit switch requires 400,000 (320x1250) lasers. "Although the numbers appear quite staggering, they point to a need for photonic integration," says Wilcox. Huawei recently acquired photonic integration specialist CIP Technologies.

The demonstration highlighted the PPXC switching OTN traffic but Wilcox stresses that the architecture is cell-based and can support all packet types: "We are flexible in the technology as the world evolves to all-packet.” The design is therefore also suited to large data centres to switch traffic between servers and for linking aggregation routers. "It is applicable in the data centre as a flattened [switch] architecture," says Wilcox.

Huawei claims the Petabit switch will deliver other benefits besides scalability. "Rough estimates comparing this device to OTN switches, MPLS switches and routers yields savings of greater than 60% on power, anywhere from 15-80% on footprint and at least a halving of fibre interconnect," says Wilcox.

Meanwhile Oclaro says Huawei is not the only vendor interested in the technology. "We have seen quite some interest recently in this area [of optical burst transmission]." says Oclaro's Blum. "I wouldn't be surprised if other companies make announcements in this space."

Further reading:

- OFC/ NFOEC 2012 paper: An Optical Burst Switching Fabric of Multi-Granularity for Petabit/s Multi-Chassis Switches and Routers