ECOC 2012 summary - Part 2: Finisar

Gazettabyte completes its summary of key optical announcements at the recent ECOC show held in Amsterdam. In Part 2, Finisar's announcements are detailed.

Part 2

"The general thought with system vendors is that the more they can shrink the in-line equipment into a fewer number of slots, the more slots they have open and available for revenue-generating transceiver and transponder cards"

Rafik Ward, Finisar

Finisar showed its board-mounted parallel optics module in use within a technology demonstrator from data storage firm Xyratex, showcased what it claims is the industry's first two-slot reconfigurable optical add/ drop multiplexer (ROADM) design, unveiled its first CFP2 pluggable transceiver and announced its latest WaveShaper products.

The data storage application uses Finisar's vertical-cavity surface-emitting laser (VCSEL)-based board mounted optical assembly. The optical assembly - or optical engine - comprises 24-channels, 12 transmitters and 12 receivers.

The optical engine sits on the board and is used for such applications as chip-to-chip interconnect, optical backplanes, and dense front panels, and supports a variety of protocols. These include PCI Express, Ethernet and Infiniband as well as proprietary schemes. Indeed the only limit is the VCSEL speed. The optical engine is designed to support traffic up to 28 Gigabit-per-second (Gbps) per channel, once 28 Gigabit VCSELs become available. Finisar have already demonstrated working 28Gbps VCSELs.

The ECOC demonstration showed the optical engine in use within Xyratex's demonstrator storage system. "They are carrying traffic between internal controller cards and the traffic being carried is 12-Gig SAS [serial attached SCSI]," says Rafik Ward, vice president of marketing at Finisar.

As well as the optical engine, the demonstration included polymer waveguides from Vario-optics which connect the optical engine to a backplane connector, built by Huber + Suhner, as well as SAS silicon from LSI.

Finisar first showed the waveguide and connector technologies in a demonstration at OFC 2012. "This is an early prototype but it's a very exciting one," says Ward. "It shows all elements of the ecosystem coming together and running in a live system."

Finisar also showcased what it claims is the industry's first two-slot ROADM line card. The line card was part of a Cisco Systems' platform, according to one analyst shown the demonstration.

The company-designed card uses a high port-count wavelength-selective switch (WSS) that enables both add and drop traffic. "We have built transmit and receive into the same line card using a high port-count device," says Ward. Finisar is not detailing the exact WSS used or how the system is implemented but describes it as a flexible spectrum, 2x1x17 port line card.

The advantage of a denser ROADM line card is that it frees up slots in a system vendor's chassis. A slot can be used for either in-line equipment - WSSes and amplifiers - or terminal equipment that host the transceivers and transponders.

"It is like valuable real-estate," says Ward. "The general thought with system vendors is that the more they can shrink the in-line equipment into a fewer number of slots, the more slots they have open and available for revenue-generating transceiver and transponder cards."

The company also detailed its first CFP2 100 Gigabit optical transceiver. The CFP2 uses a single TOSA comprising four distributed feedback (DFB) lasers, a shared thermo-electric cooler and the multiplexer. The CFP2 consumes under 8W by using the DFBs and an integrated transceiver optical sub-assembly (TOSA).

ECOC 2012 summary - Part 1: Oclaro

Gazettabyte completes its summary of key optical announcements at the recent ECOC show held in Amsterdam. Oclaro's announcements detailed here are followed by those of Finisar and NeoPhotonics.

Part 1: Oclaro

"Networks are getting more complex and you need automation so that they are more foolproof and more efficient operationally"

Per Hansen, Oclaro

Oclaro made several announcements at ECOC included an 8-port flexible-grid optical channel monitor, a new small form factor pump laser MSA and its first CFP2 module. The company also gave an update regarding its 100 Gigabit coherent optical transmission module as well as the company's status following Oclaro's merger with Opnext (see below).

The 8-port flexible grid optical channel monitor (OCM) is to address emerging, more demanding requirements of optical networks. "Networks are getting more complex and you need automation so that they are more foolproof and more efficient operationally," says Per Hansen, vice president of product marketing, optical networks solutions at Oclaro.

The 8-port device can monitor up to eight fibres, for example the input and seven output ports of a wavelength-selective switch or an amplifier's outputs.

The programmable OCM can do more than simply go from fibre to fibre, measuring the spectrum. The OCM can dwell on particular ports, or monitor a wavelength on particular ports when the system is adjusting or turning up a wavelength, for example.

"There is processing power included such that you can do a lot of data processing which can then be exported to the line card in the format required," says Hansen. This is important as operators start to adopt flexible-grid network architectures. "[With flexible-grid spectrum] you don't know where channels stop and start such that an OCM that looks at fixed slots in no longer enough," says Hansen.

The OCM can monitor bands finer than 6.25GHz through to the spectrum across the complete C-band.

Oclaro also detailed that its OMT-100 coherent 100 Gigabit optical module is entering volume production. "We have shipped well over 100 [units] to various customers," says Hansen. "There are a lot of system houses looking at this type of module this year." The OMT-100 was developed by Opnext and replaces Oclaro's own MI 8000XM 100 Gigabit module

The company also announced its first 100 Gigabit CFP2 module and its second-generation CFP module 16W power consumption that support the IEEE 100GBASE-LR4 10km standard.

A new small form factor multi-source agreement (MSA) for pump laser diodes was also announced at the show, involving Oclaro and 3S Photonics.

The 10-pin butterfly package is designed to replace the existing 14-pin design. "It is 75% smaller in volume - about two-thirds in each dimension," says Robert Blum, director of product marketing for Oclaro's photonic components. The MSA supports a single cooled or uncooled pump laser, and its smaller volume enables more integrated amplifier designs.

Oclaro says other companies have expressed interest in the MSA and it expects additional players to join.

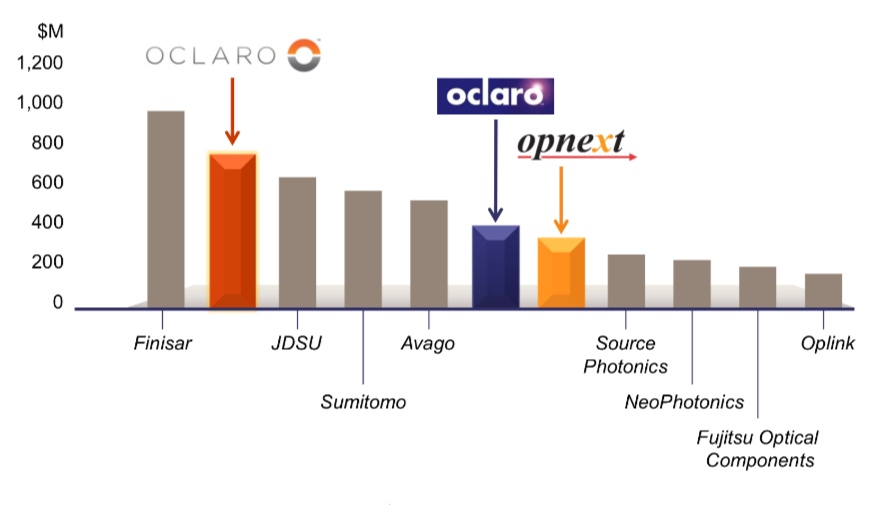

The New Oclaro

Source: Ovum

Oclaro also gave an update of the company's status following the merger with Opnext earlier this year. The now 3,000-strong company has estimated annual revenues of US $800m. This places the optical component company second only to Finisar.

The merger has broadened the company's product line, adding Opnext's strength in datacom pluggable transceivers to Oclaro's core networking products. The company is also more vertically integrated, using its optical components such as tunable laser and VCSEL technologies, modulators and receivers within its line-side transponders and pluggable optical transceivers.

"You can drive technologies in different directions and not just be out there buying components and throwing them together," says Hansen.

The company also has a range of laser diodes for industrial and consumer applications. "We [Oclaro] were already the largest merchant supplier of high-power laser diodes but now we have a complete portfolio that covers all the wavelengths from 400 up to 1500nm," says Blum.

The company has a broad range of technologies that include indium phosphide, gallium arsenide, lithium niobate, MEMS, liquid crystal and gallium nitride.

An extra business unit has also been created. To the existing optical networks solutions and the photonic components businesses there is now the modules and devices unit covering pluggable and high-speed client side transceivers, and which is based in Japan.

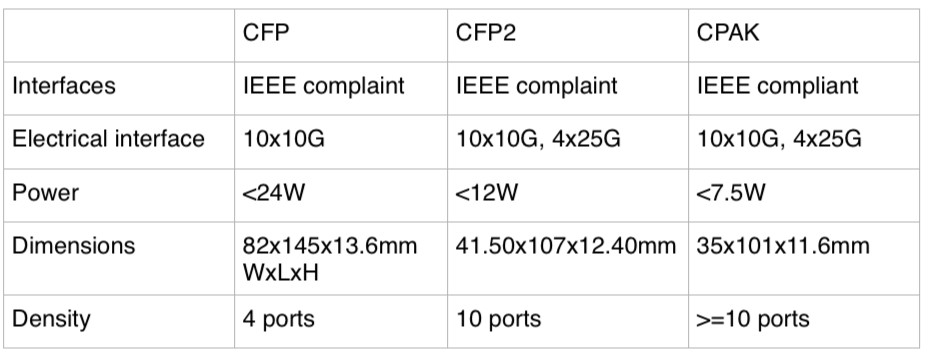

Does Cisco Systems' CPAK module threaten the CFP2?

Cisco Systems has been detailing over recent months its upcoming proprietary optical module dubbed CPAK. The development promises to reduce the market opportunity for the CFP2 multi-source agreement (MSA) and has caused some disquiet in the industry.

Source: Cisco Systems, Gazettabyte, see comments

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people," says Paul Brooks, director for JDSU's high speed transport test portfolio.

Brooks speculates that the advent of CPAK may even cause some module makers to skip the CFP2 and go straight to the smaller CFP4 given the time lag between the two MSAs is relatively short.

The CPAK module, smaller than the CFP2 MSA and three quarters its volume, has not been officially released and Cisco will not comment on the design but in certain company presentations the CPAK is compared with the CFP. The details are shown in the table above, with the CFP2’s details added.

The CPAK is the first example of Cisco's module design capability following its acquisition of silicon photonics player, Lightwire.

The development of the module highlights how the acquisition of core technology can give an equipment maker the ability to develop proprietary interfaces that promise costs savings and differentiation. But it also raises a question mark regarding the CFP2 and the merit of MSAs when a potential leading customer of the CFP2 chooses to use its own design.

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

Paul Brooks, JDSU

Industry analysts do not believe it undermines the CFP2 MSA. “I believe there is business for the CFP2,” says Daryl Inniss, practice leader, Ovum Components. “Cisco is shooting for a solution that has some staying power. The CFP2 is too large and the power consumption too high while the CFP4 is too small and will take too long to get to market; CPAK is a great compromise.”

That said, Inniss, in a recent opinion piece entitled: Optical integration challenges component/OEM ecosystem, writes:

“Cisco’s Lightwire acquisition provides another potential attack on the traditional ecosystem. Lightwire provides unique silicon photonics based technology that can support low power consumption and high-density modules. Cisco may adopt a proprietary transceiver strategy to lower cost, decrease time to market, and build competitive barriers. It need not go through the standards process, which would enable its competitors and provide them with its technology. Cisco only needs to convince its customers that it has a robust supply chain and that it can support its product.”

Vladimir Kozlov, CEO of market research firm, LightCounting, is not surprised by the development. “Cisco could use more proprietary parts and technologies to compete with Huawei over the next decade,” he says. “From a transceiver vendor perspective, custom-made products are often more profitable than standard ones; unless Cisco will make everything in house, which is unlikely, it is not bad news.”

JDSU has just announced that its ONT-100G test set supports the CFP2 and CFP4. The equipment will also support CPAK. "We have designed a range of adaptors that allows us to interface to other optics including one very large equipment vendor's - Cisco's - own CFP2-like form factor," says Brooks.

However, Brooks still expects the industry to align on a small number of MSAs despite the advent of CPAK. "The majority view is that the CFP2 and CFP4 will address most people's needs," says Brooks. "Although there is some debate whether a QSFP2 may be more cost effective than the CFP4." The QSFP2 is the next-generation compact follow-on to the QSFP that supports the 4x25Gbps electrical interface.

The CFP2 pluggable module gains industry momentum

Finisar and Oclaro unveiled their first CFP2 optical transceiver products at the recent ECOC exhibition in Amsterdam. JDSU also announced that its ONT-100G test equipment now supports the latest 100Gbps module form factor.

Source: Oclaro

Source: Oclaro

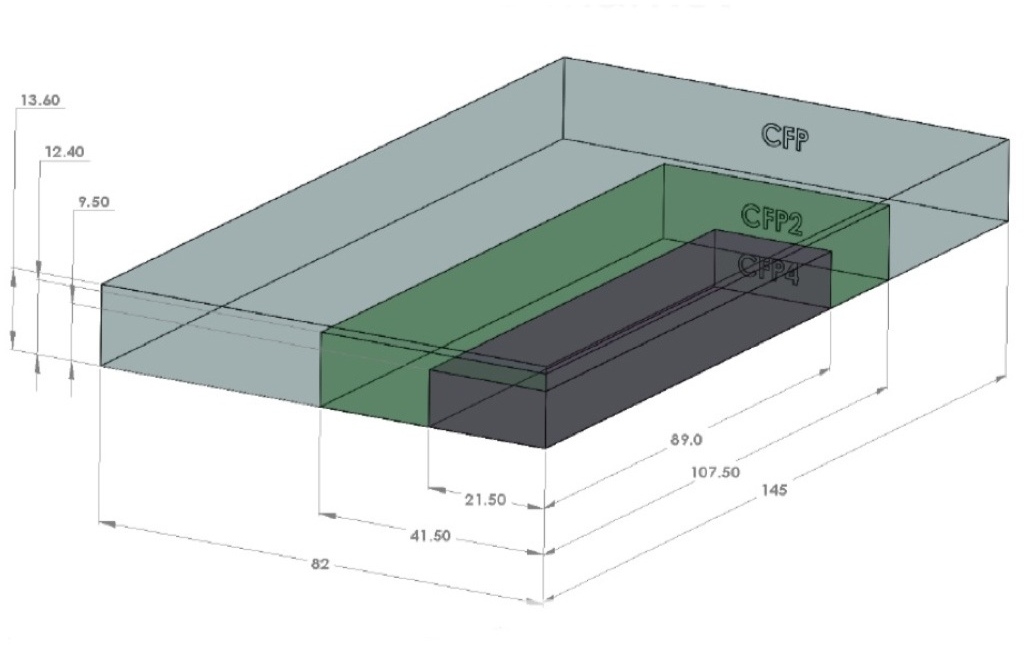

The CFP2 is the follow-on module to the CFP, supporting the IEEE 100 Gigabit Ethernet and ITU OTU4 standards. It is half the size of the CFP (see image) and typically consumes half the power. Equipment makers can increase the front-panel port density from four to eight by migrating to the CFP2.

Oclaro also announced a second-generation CFP supporting the 100GBASE-LR4 10km and OTU4 standards that reduces the power consumption from 24W to 16W. The power saving is achieved by replacing a two-chip silicon-germanium 'gearbox' IC with a single CMOS chip. The gearbox translates between the 10x10Gbps electrical interface and the 4x25Gbps signals interfacing to the optics.

The CFP2, in contrast, doesn’t include the gearbox IC.

"One of the advantages of the CFP2 module is we have a 4x25Gbps electrical interface," says Rafik Ward, vice president of marketing at Finisar. "That means that within the CFP2 module we can operate without the gearbox chip." The result is a compact, lower-power design, which is further improved by the use of optical integration.

"That 2.5x faster [interface of the CFP2] equates to about a 6x greater difficulty in signal integrity issues, microwave techniques etc"

Paul Brooks, JDSU

The transmission part of the CFP module typically comprises four externally modulated lasers (EMLs), each individually cooled. The four transmitter optical sub-assemblies (TOSAs) then interface to a four-channel optical multiplexer.

Finisar's CFP2 design uses a single TOSA holding four distributed feedback (DFB) lasers, a shared thermo-electric cooler and the multiplexer. The result of using DFBs and an integrated TOSA is that Finisar's CFP2 consumes just 8W.

Oclaro uses photonic integration on the receiver side, integrating four receiver optical sub-assemblies (ROSAs) as well as the optical demultiplexer into a single design, resulting in a 12W CFP2.

At ECOC, Oclaro demonstrated interoperability between its latest CFP and the CFP2. “It shows that the new modules will talk to existing ones,” says Robert Blum, director of product marketing for Oclaro's photonic components.

Meanwhile JDSU demonstrated its ONT-100G test set that supports the CFP2 and CFP4 MSAs.

"Initially the [test set] applications are focused on those doing the fundamental building blocks [for the 100G CFP2] – chip vendors, optical module vendors, printed circuit board developers," says Paul Brooks, director for JDSU's high speed transport test portfolio. "We will roll out more applications within the year that cover early deployment and production."

The standards-based client-side interfaces is an attractive market for test and measurement companies. For line-side optical transmission, much of the development work is proprietary such that developing a test set to serve vendors' proprietary solutions is not feasible.

The biggest engineering challenge for the CFP2 is its adoption of high-speed 25Gbps electrical interfaces. "The CFP was based on third generation, mature 10 Gig I/O [input/output]," says Brooks. "To get to cost-effective CFP2 [modules] is a very big jump: that 2.5x faster [interface] equates to about a 6x greater difficulty in signal integrity issues, microwave techniques etc."

The company says that what has been holding up the emergence of the CFP2 module has been the 104-pin connector: "The pluggable connector is the big headache," says Brooks. "The expectation is that very soon we should get some early connectors."

The test equipment also supports developers of the higher-density CFP4 module, and other form factors such as the QSFP2.

JDSU will start shipping its CFP2 test equipment in the first quarter of 2013.

Oclaro's second-generation CFP and the CFP2 transceivers are sampling, with volume production starting in early 2013.

Finisar's CFP2 LR4 product will sample in 2012 and enter volume production in 2013.

Industry underestimating 25 Gigabit parallel optics challenge

Ten Gigabit-based parallel optics is set to dominate the marketplace for several years to come. So claims datacom module specialist, Avago Technologies.

"One customer told us it has to keep the interface speed below 20Gbps due to the cost of the SerDes"

Sharon Hall, Avago

"People are underestimating what is going to be involved in doing 25 Gigabit [channels]," says Sharon Hall, product line manager for embedded optics at Avago Technologies. "Ten Gigabit is going to last quite a bit longer because of the price point it can provide."

Eventually 25 Gig-based parallel optics, with its lower lane count, will be cheaper than 10 Gigabit - but is will take several years. One challenge is the cost of 25 Gigabit-per-second (Gbps) electrical interfaces, due to the large relative size of the circuitry. One customer told Avago that it has to keep the interface speed below 20Gbps for now due to the cost of the serial/ deserialiser (SerDes).

Avago has announced that its 120 Gigabit aggregate bandwidth (12x10Gbps) MiniPod and CXP parallel optics products are now in volume production. The company first detailed the MiniPod and CXP technologies in late 2010 yet many equipment makers are still to launch their first designs.

The CXP is a pluggable optical transceiver while the MiniPod is Avago's packaged optical engine used for embedded designs. The 22x18mm MiniPod is based on Avago's 8x8mm MicroPod optical engine but uses a 9x9 electrical MegArray connector with its more relaxed pitch.

Equipment makers face a non-trivial decision as to whether to adopt copper or optical interfaces for their platform designs. "This is a major design decision with a lot of customers going back and forth deciding which way to go," says Hall. "They might do a mix with some short connections staying copper but if they need 10 Gig at anything longer than a few meters then they are going to go optical."

Having chosen parallel optics, the style of form factor - pluggable or embedded - is largely based on the interface density required. "Certain customers prefer field pluggability [of CXP] with its pay-as-you-go and ease of installation features, but are limited on port density due to the number of CXP transceivers that can physically fit on a 19 inch board," says Hall.

Up to 14 CXPs can fit onto a 19-inch board. In contrast, some 50-100 transmit and receive MiniPod pairs can fit on the 19-inch board. "You have the whole board space to work with," she says. The embedded optics sit closer to the board's ASICs, shortening the electrical path and solving signal integrity issues that can arise using edge-mounted pluggables. Thermal management - not having all the pluggable optics at the card edge furthest from the fans - is also simplified using embedded optics.

Generally, connections to data centre top-of-rack switches and between chassis use the pluggable CXP while internal backplane and mid-plane designs use the MiniPod. The CXP is also used by core switches and routers; Alcatel-Lucent's recently announced 7950 core router has a four-port CXP-based card. But Avago stresses that there are no hard rules: It has customers that have chosen the CXP and others the MiniPod for the same class of platform.

Source: Gazettabyte

Source: Gazettabyte

25 Gigabit parallel optics

Finisar recently demonstrated its board mounted optical assembly that it says will support channel speeds of 10, 14, 25 and 28Gbps, while silicon photonics vendors Luxtera and Kotura have announced 4x25Gbps optical engines. OneChip Photonics has announced photonic integrated circuits for the 4x25Gbps, 100GBase-LR4 10km standard that will also address short and mid-reach applications

Avago has yet to make an announcement regarding higher speed parallel optics. "It is just a matter of time," says Hall. "We have done a demonstration of our 25Gbps VCSEL in an SFP+ package over a year ago, and we are developing parallel optics 25Gbps solutions."

But 25Gbps will take time before it gets to volume production, says Hall: "It is going to be a long, long design cycle for system companies - doing 25Gbps on their boards and their systems is a completely new design."

Supercomputers and system mid-plane and backplane applications could happen a lot earlier than 4x25GbE applications. "Some customers are interested in getting 4x25Gbps samples in the 2013 timeframe," says Hall. "But we expect that volume is going to take at least another year from that."

Meanwhile, Avago says it has already shipped 600,000 MicroPods which has been generally available for over a year.

The CFP4 optical module to enable Terabit blades

Source: Gazettabyte, Xilinx

Source: Gazettabyte, Xilinx

The CFP2 is about half the size of the CFP while the CFP4 is half the size of the CFP2. The CFP4 is slightly wider and longer than the QSFP.

The two CFP modules will use a 4x25Gbps electrical interface, doing away with the need for a 10x10Gbps to 4x25Gbps gearbox IC used for current CFP 100GBASE-LR4 and -ER4 interfaces. The CFP2 and CFP4 are also defined for 40 Gigabit Ethernet use.

The CFP's maximum power rating is 32W, the CFP2 12W and the CFP4 5W. But vendors that put eight CFP2 or 16 CFP4s on a blade still want to meet the 60W total power budget.

Getting close: Four CFP modules deliver slightly less bandwidth than 48 SFP+ modules: 4x100Gbps versus 480Gbps. The four also consume more power - 60w versus 48W. Moving to the CFP2 module will double the blade's bandwidth without consuming more power while the CFP4 will do the same again. a blade with 16 CFP4 modules promises 1.6Tbps while requiring 60W. Source: Xilinx

Getting close: Four CFP modules deliver slightly less bandwidth than 48 SFP+ modules: 4x100Gbps versus 480Gbps. The four also consume more power - 60w versus 48W. Moving to the CFP2 module will double the blade's bandwidth without consuming more power while the CFP4 will do the same again. a blade with 16 CFP4 modules promises 1.6Tbps while requiring 60W. Source: Xilinx

The first CFP2 modules are expected this year - there could be vendor announcements as early as the upcoming OFC/NFOEC 2012 show to be held in LA in the first week in March. The first CFP4 products are expected in 2013.

Further reading

The CFP MSA presentation: CFP MSA 100G roadmap and applications

Reflections and predictions: 2011 & 2012 - Part 1

"For 2012, the macroeconomy is likely to dominate any other developments"

Martin Geddes, telecom consultant @martingeddes

Sometimes the important stuff is slow-burning: we're seeing a continued decline in the traditional network equipment providers, and the rise in Genband, Acme, Sonus and Metaswitch in their place. Smaller, leaner, and more used to serving Tier 2 and Tier 3 operators and enterprise players and their lower cost structures.

The recognition of the decline of SMS and telephony became mainstream in 2011 -- maybe I can close down my Telepocalypse blog as what I foresaw is reality.

We've seen absolute declines in revenue and usage of telco voice and messaging in leading markets like Norway and Netherlands. The creation of Telefonica Digital is a landmark reorganisation around new markets. No longer are those initiatives endlessly parked in business development whilst marketing dream up a new price plan for minutes, messages and megabytes.

If I had to pick one thing to characterise 2011, it was the year of the App.

For 2012, the macroeconomy is likely to dominate any other developments. The scenarios are "distress", "meltdown" and "collapse".

Telecoms is well-placed to weather the storm. Even £600 smartphones may remain in vogue as people defer purchases like cars and holidays, and hide their fiscal distress with status symbols hewn out of pure blocks of profit.

Voice will be much more prominent, after decades of languishing, as LTE sets up a complex dynamic of service innovation driven by over-the-top applications - which will increasingly come from telcos as well as telecoms outsiders. Microsoft's purchase of Skype is the one to watch - if they get it right, it joins Windows and Office in the hall of fame; get it wrong, and Microsoft is probably out of the smartphone game due to a lack of competitive differentiation and advantage.

So 2012 is the year when (mobile) voice gets vocal again - because we're going to have a lot to talk about, and want to do it much cheaper and better.

Brandon Collings, CTO for communications and commercial optical products at JDS Uniphase

For the course of 2011, the tunable XFP shipped in volume and it rather quickly supplanted the 300-pin transceiver. On the service/ market trend, over-the-top consumer video (Netflix) grew rapidly to be the dominant traffic on the internet.

"Solutions for the next generation ROADM networks - self aware networks - are now firm"

I expect the maturation of 100 Gigabit to continue through 2012 with the introduction of a number of new 100 Gigabit solutions, both network equipment makers and at the transceiver level.

Also, as the adoption percentage of consumers using over-the-top video usage still seems to be relatively small, yet is growing strongly and is already the dominant traffic on the internet, it will be interesting to see how this trend continues as it strongly drives bandwidth yet with potentially unfavorable revenue models for the network operators who need to deliver it.

Lastly, I expect that as the solutions for the next generation ROADM networks - self aware networks - are now firm, the practical assessment of the value and advantages of these networks can quantitatively take place.

Eve Griliches, managing partner, ACG Research @EveGr

The Juniper PTX announcement really caught the market by surprise. I'm not so much sure why but clearly it rocked some folks back on their heels. Momentum for the product has been good as well. I think you can count this as a success story.

Another one is the Infinera 500Gbps release with super-channels. A pretty impressive technology and service providers are waiting for final product to test.

The death of Steve Jobs rattled us all. I think it struck a note for everyone in how different he was and how he touched us all.

"Content providers ask for simple, scalable and low-featured products. Those who deliver will be rewarded for listening."

I continue to be amazed at how much optical equipment content providers [the Googles, Facebooks, MSNs of this world] are deploying and how few folks at the vendor level are doing anything about getting into their networks. Maybe that is a 2012 thing, I don't know.

As for 2012, we'll definitely see some mergers and acquisitions - expect low acquisition prices too - and some companies exiting this market. I love optics and it really pains me to say that, but there are just more companies out there who can't support the declining margins. I think margin erosion will be key to who survives.

Cisco and Infinera should be bringing some cool products to market in the next six months. We hope the products are good because it will generate debate for the final vendor choices for operators such as AT&T and Verizon.

Again, content providers ask for simple, scalable and low-featured products. Those who deliver will be rewarded for listening. Some don't listen, and will wonder what happened.

Peter Jarich, service director, service provider infrastructure, mobile ecosystem, Current Analysis @pnjarich

2012 is going to be the year for LTE-Advanced (LTE-A). Why? One, vendors always like to talk up what’s next, and LTE-A is what follows LTE (Long Term Evolution).

At the same time, operators who haven’t yet deployed LTE will want to look to start with the latest and greatest. Of course, LTE-A brings real advances for operators: carrier aggregation for dealing with fragmented spectrum assets; heterogeneous networks for dealing with the interaction of small cell and macrocell networks; relaying for improved cell edge performance.

Avi Shabtai, CEO of MultiPhy

The most significant development of 2011 was the availability of CMOS technology that allows next-generation optical transport solutions for 100 Gigabit. And specifically, metro-focused solutions that hit the cost and power numbers required by this industry.

On top of that, optical communication has entered the era of digital signal processing receivers. We have also seen the potential segmentation in 100 Gigabit of metro versus long-haul, each with its specific set of solutions.

"We will see a huge growth in video consumption. This has already started but it is just the tip of the iceberg."

The transition of the telecom and datacom market to 100 Gigabit has also begun - from the transport optical network all the way to copper backplanes - it's all a 4x25Gbps architecture. This year has also seen consolidation in the ecosystem, especially among module companies.

This consolidation will continue at all industry levels in 2012: semiconductors, subsystems, systems and the carriers. The consolidation will coincide with an across-the-board price reduction in emerging technologies like 100 Gigabit transport.

The increase in capacity demand will also force an increase in requirements for various solutions supporting 100 Gigabit. I expect to see more CMOS-based devices introduced.

From a services point or view, we will see a huge growth in video consumption. This has already started but it is just the tip of the iceberg. Video will have a tremendous influence on network evolution.

Gilles Garcia, director, wired communication at Xilinx @gllsgarcia

The CFP2 and CFP4 optical modules are arriving a lot faster than it took for the CFP to follow the XFP optical module.

The CFP standard took 3-4 years to complete while the standard for the CFP2 just closed after two years. Now the CFP4 standard has been launched and is expected to take 18 months only. The new form factors are being driving by the cost-per-port of 100 Gigabit and how to reduce it. The CFP2 doubles the density when compared to the CFP while the CFP4 doubles it again.

"Programmability is becoming the key trend among telecom system vendors as operators look to react faster to standards, new feature requests and deployment of new services."

Telecom application-specific standard product (ASSP) players have been relatively quiet in 2011. Word from customers is that such vendors are pushing out their roadmap/ product availability because of too much flux in the various IEEE and ITU-T telecom standards and difficulties to justify the return-on-investment. This is proving a perfect opportunity for FPGAs.

Large system vendors are growing their network services as operators continue to outsource their network management and maintenance. As reported in their financial reports, this is an important source of business for the likes of Ericsson, Huawei and Alcatel-Lucent.

It is leading the vendors to push more of their own hardware, as they look to add value-add services and integrate the services using their own platforms. Some equipment vendors realise they do not have a full portfolio and have established partnerships for the missing platforms. They are also starting to develop platforms to generate more revenue.

In 2012, I’m not expecting a telecom revolution but I do expect accelerated evolution. And I foresee big disruptions in the ASSP market as it continues to consolidate: I expect several mergers and acquisitions among the top 20 ASSP suppliers.

Programmability is becoming the key trend among telecom system vendors as operators look to react faster to standards, new feature requests and deployment of new services. Programmability also improves time-to-market to deliver these services and reduce time-to-revenue.

Mobile backhaul will be a market driver in 2012. The growth in mobile data terminals will lead to a new generation of mobile backhaul networks. This will drive the move from 1 to 10 Gigabit Ethernet, higher-feature packet processing, and traffic management integration into mobile infrastructure to better control and bill bandwidth usage i.e. pay for what you use.

The 'God box' - packet optical transport systems and the like - are back, but really it is network needs that is driving this.

And one topic to watch that will become clearer in 2012 is how cloud computing impacts the networking market with regard such issues as security, cacheing and higher speed links.

Google is becoming an important internal - for its own usage -networking equipment player. And Google will be joined by others - Facebook, Amazon etc. What impact will this have on the traditional system networking vendors? Such new players are defining and building networks platforms tailored for their needs. This is competition to the traditional system vendors who are not getting this piece of the business. Semiconductors, including FPGAs, could serve those companies directly.

Other issues to note: What will Intel do in the networking space? Intel acquired Fulcrum in 2011 and has invested in several networking companies.

There are also technology issues.

What will happen to ternary content addressable memory (TCAM)? Broadcom's acquisition of NetLogic Microsystems has created a hole in the TCAM market. Will Broadcom continue with TCAM? Will customers want to give their TCAM business to Broadcom?

Xilinx FPGAs have added network search engines IP in the solution portfolio as multi-core ‘search engine’ face increasing difficulty in sustaining the performance required.

And of course there is the continual issue of power optimisation.

For Part 2, click here

For Part 3, click here

100 Gigabit: An operator view

Gazettabyte spoke with BT, Level 3 Communications and Verizon about their 100 Gigabit optical transmission plans and the challenges they see regarding the technology.

Briefing: 100 Gigabit

Part 1: Operators

Operators will use 100 Gigabit-per-second (Gbps) coherent technology for their next-generation core networks. For metro, operators favour coherent and have differing views regarding the alternative, 100Gbps direct-detection schemes. All the operators agree that the 100Gbps interfaces - line-side and client-side - must become cheaper before 100Gbps technology is more widely deployed.

"It is clear that you absolutely need 100 Gig in large parts of the network"

Steve Gringeri, Verizon

100 Gigabit status

Verizon is already deploying 100Gbps wavelengths in its European and US networks, and will complete its US nationwide 100Gbps backbone in the next two years.

"We are at the stage of building a new-generation network because our current network is quite full," says Steve Gringeri, a principal member of the technical staff at Verizon Business.

The operator first deployed 100Gbps coherent technology in late 2009, linking Paris and Frankfurt. Verizon's focus is on 100Gbps, having deployed a limited amount of 40Gbps technology. "We can also support 40 Gig coherent where it makes sense, based on traffic demands," says Gringeri.

Level 3 Communications and BT, meanwhile, have yet to deploy 100Gbps technology.

"We have not [made any public statements regarding 100 Gig]," says Monisha Merchant, Level 3’s senior director of product management. "We have had trials but nothing formal for our own development." Level 3 started deploying 40Gbps technology in March 2009.

BT expects to deploy new high-speed line rates before the year end. "The first place we are actively pursuing the deployment of initially 40G, but rapidly moving on to 100G, is in the core,” says Steve Hornung, director, transport, timing and synch at BT.

Operators are looking to deploy 100Gbps to meet growing traffic demands.

"If I look at cloud applications, video distribution applications and what we are doing for wireless (Long Term Evolution) - the sum of all the traffic - that is what is putting the strain on the network," says Gringeri.

Verizon is also transitioning its legacy networks onto its core IP-MPLS backbone, requiring the operator to grow its base infrastructure significantly. "When we look at demands there, it is clear that you absolutely need 100 Gig in large parts of the network," says Gringeri.

Level 3 points out its network between any two cities has been running at much greater capacity than 100 Gbps so that demand has been there for years, the issue is the economics of the technology. "Right now, going to 100Gbps is significantly a higher cost than just deploying 10x 10Gbps," says Level 3's Merchant.

BT's core network comprises 106 nodes: 20 in a fully-meshed inner core, surrounded by an outer 86-node core. The core carries the bulk of BT's IP, business and voice traffic.

"We are taking specific steps and have business cases developed to deploy 40G and 100G technology: alternative line cards into the same rack," says Hornung.

Coherent and direct detection

Coherent has become the default optical transmission technology for operators' next-generation core networks.

BT says it is a 'no-brainer' that 400Gbps and 1 Terabit-per-second light paths will eventually be deployed in the network to accommodate growing traffic. "Rather than keep all your options open, we need to make the assumption that technology will essentially be coherent going forward because it will be the bandwidth that drives it," says Hornung.

Beyond BT's 106-node core is a backhaul network that links 1,000 points-of-presence (PoPs). It is this part of the network that BT will consider 40Gbps and perhaps 100Gbps direct-detection technology. "If it [such technology] became commercially available, we would look at the price, the demand and use it, or not, as makes sense," says Hornung. "I would not exclude at this stage looking at any technology that becomes available." Such direct-detection 100Gbps solutions are already being promoted by ADVA Optical Networking and MultiPhy.

However, Verizon believes coherent will also be needed for the metro. "If I look at my metro systems, you have even lower quality amplifiers, and generally worse signal-to-noise," says Gringeri. “Based on the performance required, I have no idea how you are going to implement a solution that isn't coherent."

Even for shorter reach metro systems - 200 or 300km- Verizon believes coherent will be the implementation, including expanding existing deployments that carry 10Gbps light paths and that use dispersion-compensated fibre.

Level 3 says it is not wedded to a technology but rather a cost point. As a result it will assess a technology if it believes it will address the operator's needs and has a cost performance advantage.

100 Gig deployment stages

The cost of 100Gbps technology remains a key challenge impeding wider deployment. This is not surprising since 100Gbps technology is still immature and systems shipping are first-generation designs.

Operators are willing to pay a premium to deploy 100Gbps light paths at network pinch-points as it is cheaper that lighting a new fibre.

Metro deployments of new technology such as 100Gbps occur generally occur once the long-haul network has been upgraded. The technology is by then more mature and better suited to the cost-conscious metro.

Applications that will drive metro 100Gbps include linking data centre and enterprises. But Level 3 expects it will be another five years before enterprises move from requesting 10 Gigabit services to 100 Gigabit ones to meet their telecom needs.

Verizon highlights two 100Gbps priorities: the high-end performance dense WDM systems and client-side 'grey' (non-WDM) optics used to connect equipment across distances as short as 100m with ribbon cable to over 2km or 10km over single-mode fibre.

"I would not exclude at this stage looking at any technology that becomes available"

Steve Hornung, BT

"Grey optics are very costly, especially if I’m going to stitch the network and have routers and other client devices and potential long-haul and metro networks, all of these interconnect optics come into play," says Gringeri.

Verizon is a strong proponent of a new 100Gbps serial interface over 2km or 10km. At present there are the 100 Gigabit interface and the 10x10 MSA. However Gringeri says it will be 2-3 years before such a serial interface becomes available. "Getting the price-performance on the grey optics is my number one priority after the DWDM long haul optics," says Gringeri.

Once 100Gbps client-side interfaces do come down in price, operators' PoPs will be used to link other locations in the metro to carry the higher-capacity services, he says.

The final stage of the rollout of 100Gbps will be single point-to-point connections. This is where grey 100Gbps comes in, says Gringeri, based on 40 or 80km optical interfaces.

Source: Gazettabyte

Source: Gazettabyte

Tackling costs

Operators are confident regarding the vendors’ cost-reduction roadmaps. "We are talking to our clients about second, third, even fourth generation of coherent," says Gringeri. "There are ways of making extremely significant price reductions."

Gringeri points to further photonic integration and reducing the sampling rate of the coherent receiver ASIC's analogue-to-digital converters. "With the DSP [ASIC], you can look to lower the sampling rate," says Gringeri. "A lot of the systems do 2x sampling and you don't need 2x sampling."

The filtering used for dispersion compensation can also be simpler for shorter-reach spans. "The filter can be shorter - you don't need as many [digital filter] taps," says Gringeri. "There are a lot of optimisations and no one has made them yet."

There are also the move to pluggable CFP modules for the line-side coherent optics and the CFP2 for client-side 100Gbps interfaces. At present the only line-side 100Gbps pluggable is based on direct detection.

"The CFP is a big package," says Gringeri. "That is not the grey optics package we want in the future, we need to go to a much smaller package long term."

For the line-side there is also the issue of the digital signal processor's (DSP) power consumption. "I think you can fit the optics in but I'm very concerned about the power consumption of the DSP - these DSPs are 50 to 80W in many current designs," says Gringeri.

One obvious solution is to move the DSP out of the module and onto the line card. "Even if they can extend the power number of the CFP, it needs to be 15 to 20W," says Gringeri. "There is an awful lot of work to get where you are today to 15 to 20W."

* Monisha Merchant left Level 3 before the article was published.

Further Reading:

100 Gigabit: The coming metro opportunity - a position paper, click here

Click here for Part 2: Next-gen 100 Gig Optics

100 Gigabit for the metro

The firm claims this is an industry first: a direct-detection-based 100 Gigabit-per-second (Gbps) design using four, 28Gbps channels rather than current 10x10Gbps schemes.

"Data centre operators want to make best use of the fibre insfrastructure and get lower overall cost, footprint and power consumption"

Jörg-Peter Elbers, ADVA Optical Networking

The card, designed for the FSP 3000 platform, delivers a 2.5x greater spectral efficiency compared to 10Gbps dense WDM (DWDM) systems. In turn, the 100Gbps metro card has half the cost of a 100 Gigabit coherent design while requiring half the power and space.

ADVA Optical Networking is using a CFP optical module to implement the 100Gbps metro design. This allows the card to use other CFP-based interfaces such at the IEEE 100 Gigabit Ethernet (GbE) standards. The design also benefits from the economies of scale of the CFP as the module of choice for 100GbE, and from future smaller modules such as the CFP2 and CFP4 being developed as the 100GbE market evolves.

The 100Gbps metro CFP's four, 28Gbps signals are modulated using optical duo-binary. By choosing duo-binary, cheaper 10Gbps optics can be used akin to a 4x10Gbps design. Duo-binary is also more resilient to dispersion than standard on-off keying.

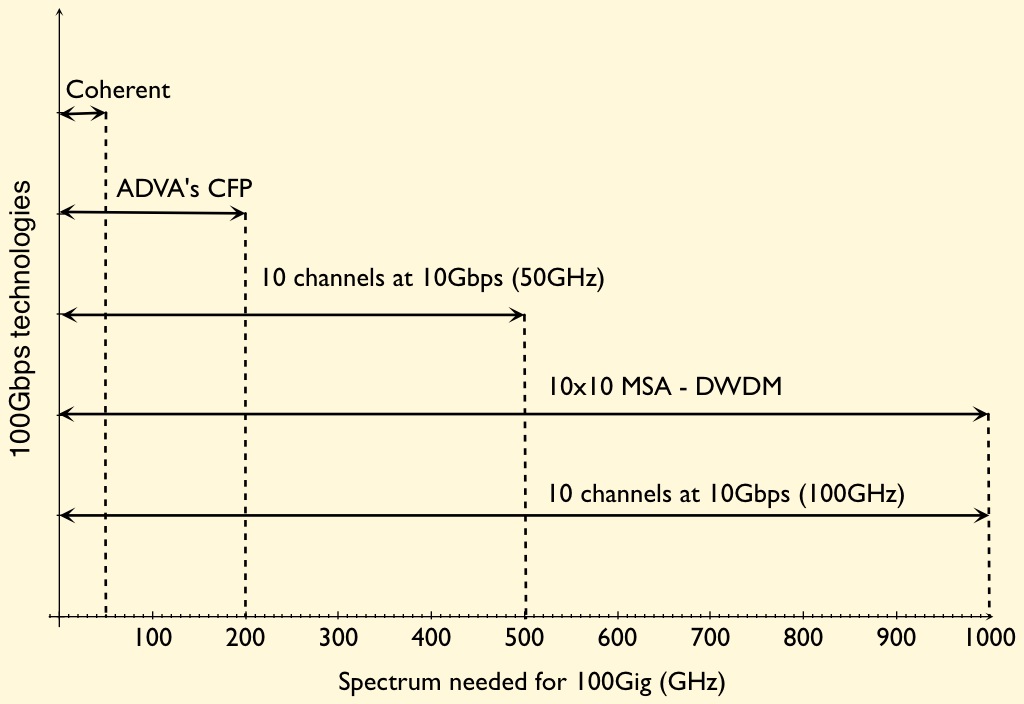

The CFP-based card requires 200GHz of spectrum for each 100Gbps light path. This is 2.5x more spectrally efficient than 10x10Gbps based on 50GHz channel spacings. However, while the design is cheaper, denser and less power hungry than 100Gbps coherent, it has only a quarter of the spectral efficiency of coherent (see chart).

Jörg-Peter Elbers, vice president, advanced technology at ADVA Optical Networking, says duo-binary delivers closer channel spacing such that a doubling in spectral density will be possible in a future design (100Gbps in a 100GHz channel). The 100Gbps metro card supports 500km links using dispersion-compensated fibre.

Non-coherent designs for the metro are starting to appear despite 100Gbps optical transport being in its infancy. Besides ADVA Optical Networking's design, a component vendor is promoting a 100Gbps direct detection DWDM design for the metro. The 10x10 MSA has also announced a DWDM extension that will support four and eight 100Gbps channels.

The 100G metro card showing the CFP. Source: ADVA Optical Networking

The 100G metro card showing the CFP. Source: ADVA Optical Networking

Metro direct-detection also faces competition from system vendors developing coherent designs tailored for the metro.

System vendors, module makers, optical and IC component companies all believe there is a market for lower cost 100Gbps metro transport. This is backed by keen interest from service providers and large content providers that want cheaper 100Gbps interfaces to connect data centres.

Elbers highlights two such applications that will first likely use the 100 Gigabit metro card.

One is connecting the data centres of enterprises that use rented fibre. "They have a multitude of interfaces and services - 10GbE, 8 Gigabit Fibre Channel - and they often rent fibre," says Elbers. "They need to get as much capacity as possible to make the fibre rent worthwhile while being constrained on rack space and power."

The second application is to connect 100GbE-enabled IP routers across the metro. Here service providers may not have heavily loaded DWDM networks and can afford to use a 100Gbps metro link rather than the more spectrally efficient, if more expensive, 100Gbps coherent interface. Equally, such links may be less than 500km while coherent is designed for long-haul links, 1000km or greater.

Elbers says samples of the metro card are available now with volume production beginning at the end of 2011.

Introducing 100G Metro (ADVA Optical video)

OFC announcements and market trends

More compact transceiver designs at 10, 40 and 100 Gigabit, advancements in reconfigurable optical add-drop multiplexer (ROADM) technology and parallel optical engine developments were all in evidence at this year’s OFC/NFOEC show held in Los Angeles in March.

“MSAs are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market”

“MSAs are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market”

Victor Krutul, Avago Technologies

Finisar said that the show was one of the busiest in recent years. “There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts,” says Rafik Ward, vice president of marketing at Finisar.

Ethernet interfaces

Opnext demonstrated an IEEE 100GBASE-ER4 module design at the show, the 100 Gigabit Ethernet (GbE) standard with a 40km reach. Based on the company’s CFP-based 100GBASE-LR4 10km module, the design uses a semiconductor optical amplifier (SOA) on the receive path to achieve the extended reach. The IEEE standard calls for an SOA in front of the photo-detectors for the 100GBASE-ER4 interface.

“We don’t have that [SOA] integrated yet, we are just showing the [design] feasibility,” says Jon Anderson, director of technology programme at Opnext. The extended reach interface will be used to connect IP core routers to transport system when the two platforms reside in separate facilities. Such a 40km requirement for a 100GbE interface is not common but is an important one to meet, says Anderson.

Opnext’s first-generation LR4, currently shipping, is a discrete design comprising four discrete transmitter optical sub-assemblies (TOSAs) and four receiver optical sub-assemblies (ROSAs) and an optical multiplexer and demultiplexer. The company’s next-generation design will integrate the four lasers and the optical multiplexer into a package and will be used in future more compact CFP2 and CFP4 modules.

The CFP2 module is half the size of the CFP module and the CFP4 is a quarter. In terms of maximum power, the CFP module is rated at 32W, the CFP2 12W and the CFP4 5W. “The CFP4 is a little bit wider and longer than the QSFP,” says Anderson. The first CFP2 modules are expected to become available in 2012 and the CFP4 in 2013.

System vendors are interested in the CFP4 as they want to support over one terabit of capacity on a 15-inch faceplate. Up to 16 ports can be supported –1.6Tbps – on a faceplate using the CFP4, and using a “belly-to-belly” configuration two rows of 16 ports will be possible, says Anderson.

Finisar demonstrated a distributed feedback laser (DFB) laser-based CFP module at OFC that implements the 10km 100GBASE-LR4 standard. The adoption of DFB lasers promises significant advantages compared to existing first-generation -LR4 modules that use electro-absorption modulated lasers (EMLs). “If you look at current designs, ours included, not only do they use EMLs which are significantly more expensive, but each is in its own package and has its own thermo-electric cooler,” says Ward.

Finisar’s use of DFBs means an integrated array of the lasers can be packaged and cooled using a single thermo-electric cooler, significantly reducing cost and nearly halving the power to 12W. “Now that the power [of the DFB-based] LR4 is 12W, we can place it within a CFP2 with its 25-28 Gigabit-per-second (Gbps) electrical I/O,” says Ward.

Moving to the faster input/output (I/O) compared to the CFP’s 10Gbps I/O means that that serialiser/ deserialiser (serdes) chipset can be replaced with simpler clock data recovery (CDR) circuitry. “By the time we move to the CFP4, we remove the CDRs completely,” says Ward. “It’s an un-retimed interface.” Finisar’s existing -LR4 design already uses an integrated four-photodetector array.

An early application of the 100GbE -LR4, as with the -ER4, is linking core routers with optical transport systems in operators’ central offices. Many Ethernet switch vendors have chosen to focus their early high-data efforts at 40GbE but Finisar says the move to 100GbE has started.

Finisar argues that the adoption of DFBs will ultimately prove the cost-benefits of a 4-channel 100GbE design which faces competition from the emerging 10x10 multi-source agreement (MSA). “Everything we have heard about the 10x10 [MSA] has been around cost,” says Ward. “The simple view inside Finisar is that by the time the Gen2 100GbE module that we showed at OFC gets to market, this argument [4x25Gig vs. 10x10Gig] will be a moot point.”

“40Gig is definitely still strong and healthy”

“40Gig is definitely still strong and healthy”

Jon Anderson, Opnext

By then the second-generation -LR4 module design will be cost competitive if not even lower cost than the 10x10 MSA. “If you look at optoelectronic components, at the end of the day what really drives cost is yield,” says Ward. “If we can get our yields of 25Gig DFBs down to a level that is similar to 10Gig DFB yields- it doesn’t have to match, just in the ballpark - then we have a solution where the 4x25Gig looks like a 4x10Gig solution and then I believe everyone will agree that 4x25Gig is a less expensive architecture.” Finisar expects the Gen2 CFP -LR4 in production by the first half of 2012.

Opnext demonstrated a 40GBASE- LR4 (40Gbps, up to 10km) standard in a QSFP+ module at OFC. Anderson says it is seeing demand for such a design from data centre operators and from switch and transport vendors.

Avago Technologies announced a 40Gbps QSFP+ module at OFC that implements the 100m IEEE 40GBASE-SR4. “It will interoperate with Avago’s SFP+ modules,” says Victor Krutul, director of marketing for the fibre optics division at Avago Technologies. The QSFP+ can interface to another QSFP+ module or to four 10Gbps SFP+ modules.

Avago also announced a proprietary mini-SFP+ design, 30% smaller than the standard SFP+ but which is electrically compatible. According to Krutul, the design came about following a request from one of its customers: “What it allows is the ability to have 64 ports on the front [panel] rather than 48.”

Did Avago consider making the mini-SFP+ design an MSA? “What we found with MSAs is that they are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market,” says Krutul.

Krutul was previously a marketing manager for Intel’s LightPeak before joining Avago over half a year ago.

“There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts”

“There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts”

Rafik Ward, Finisar.

Line-side interfaces

Opnext will be providing select customers with its 100Gbps DP-QPSK coherent module for trialling this quarter. The module has a 5-inch by 7-inch footprint and uses a 168-pin connector. “We are working to try and meet the OIF spec [with regard power consumption] which is 80W.” says Anderson. “It is challenging and it may not be met in the first generation [design].”

The company is also moving its 40Gbps 2km very short reach (VSR) transponder to support the IEEE 40GBASE-FR standard within a CFP module, dubbed the “tri-rate” design. “The 40BASE-FR has been approved, with the specification building on the ITU’s 40Gig VSR,” says Anderson. “It continues to support the [OC-768] SONET/SDH rate, it will support the new OTN ODU3 40Gbps and the intermediate 40 Gigabit Ethernet.”

Opnext and Finisar are both watching with interest the emerging 100Gbps direct detection market, an alternative to 100 Gigabit coherent aimed shorter reach metro applications.

“We certainly are watching this segment and do have an interest, but we don’t have any product plans to share at this point,” says Anderson.

“The [100Gbps] direct-detection market is very interesting,” says Ward. Coherent is not going to be the only way people will deploy 100Gbps light paths. “There will be a market for shorter reach, lower performance 100 Gigabit DWDM that will be used primarily in datacentre-to-datacentre,” he says. Tier 2 and tier 3 carriers will also be interested in the technology for use in shorter metro reaches. “There is definitely a market for that,” says Ward.

Opnext also announced its small form-factor – 3.5-inch by 4.5-inch - 40Gbps DPSK module. “With a smaller form factor, the next generation could move to a CFP type pluggable,” says Anderson. “But that is if our customers are interested in migrating to a pluggable design for DPSK and DQPSK.”

Are there signs that the advent of 100 Gigabit is affecting 40Gbps uptake? “We definitely not seeing that,” says Anderson. “We are continuing to see good solid demand for both 40G line side – DPSK and DQPSK – and a lot of pull to being this tri-rate VSR.”

Such demand is not just from China but also North Ametican carriers. “40 Gig is definitely still strong and healthy,” says Anderson “But there are some operators that are waiting to see how 100G does and approved in for major build-outs.”

At 10Gbps, Opnext also had on show a tunable TOSA for use in an XFP module, while Finisar announced an 80km, 10Gbps SFP+ module. “SFP+ has become a very successful form factor at 10Gbps,” says Ward. “All the market data I see show SFP+ leads in overall volumes deployed by a significant margin.” Its success has been achieved despite being a form factor was not designed to achieve all the 10Gbps reaches required initially. This is some achievement, says Ward, since the XFP+ form factor used for 80km has a power rating of 3.5W while the 80km SFP+ has to work within a less than 2W upper limit.

Parallel Optics

Avago detailed its main parallel optic designs: the CXP module and its two optical engine designs.

The company claims it seeing much interested from high-performance computing vendors such as IBM and Fujitsu for its CXP 120 Gigabit (12x10Gbps) parallel transceiver module. Avago is sampling the module and it will start shipping in the summer.

The company also announced the status of its embedded parallel optics devices (PODs). Such parallel optic designs offer several advantages, says Krutul. Embedding the optics on the motherboard offers greater flexibility in cooling since the traditional optics is normally at the edge of the card, furthest away from the fans. Such optics also simplify high-speed signal routing on the printed circuit board since fibre is used.

Avago offers two designs – the 8x8mm MicroPod and the 22x18mm MiniPod. The 12x10Gbps MicroPods are being used in IBM’s Blue Gene computer and Avago says it is already shipping tens of thousands of the devices a month. “The [MicroPod’s] signal pins have a very tight pitch and some of our customers find that difficult to do,” says Krutul. The MiniPod design tackles this by using the MicroPod optical engine but a more relaxed pitch. At OFC, Avago said that the MiniPod is now sampling.

Gridless ROADMs

Finisar demonstrated what it claims is the first gridless wavelength-selective switch (WSS) module at the show. A gridless ROADM supports variable channel widths beyond the fixed International Telecommunication Union's (ITU) defined spacings. Such a capability enables ROADMs to support variable channel spacings that may be required for transmission rates beyond 100Gbps: 400Gbps, 1Tbps and beyond.

“We have an increasing amount of customer interest in this [FlexGrid], and from what we can tell, there is also an increasing amount of carrier interest as well,” says Ward, adding that the company is already shipping FlexGrid WSSs to customers.

Finisar is a contributing to the ongoing ITU work to define what the grid spacings and the central channels should be for future ROADM deployments. Finisar demonstrated its FlexGrid design implementing integer increments of 12.5GHz spacing. “We could probably go down to 1GHz or even lower than that,” says Ward. “But the network management system required to manage such [fine] granularity would become incredibly complicated.” What is required for gridless is a balance between making good use of the fibre’s spectrum while ensuring the system in manageable, says Ward.