Achieving 56 Gigabit VCSELs

A Q&A with Finisar's Jim Tatum, director of new product development. Tatum talks about the merits of the vertical-cavity surface-emitting laser (VCSEL) and the challenges to get VCSELs to work at 56 Gigabit.

Briefing: VCSELs

VCSELs galore! A wafer of 28 Gig devices Source: Finisar

VCSELs galore! A wafer of 28 Gig devices Source: Finisar

Q. What are the merits of VCSELs compared to other laser technologies?

A: VCSELs have been a workhorse for the datacom industry for some 15 years. In that time there have been some 500 million devices deployed for data infrastructure links, with Finisar being a major producer of these VCSELs.

The competition is copper which means you need to be at a cost that makes such [optical] links attractive. This is where VCSELs have value: operating at 850nm which means running on multi-mode fibre.

Coupling VCSELs to multi-mode fibre [the core diameter] is in the tens of microns whereas it is one micron for single-mode fibre and that is where the cost is. Also with VCSELs and multi-mode fibre, we don't need optical isolators which add significant cost to the assemblies. It is not the cost of the laser die itself; the difference in terms of the link [approaches] is the cost of the optics and getting light in and out of the fibre.

There are also advantages to the VCSEL itself: wafer-level testing that allows rapid testing of the die before you commit to further packaging costs. This becomes more important as the VCSEL speed gets higher.

What are the differences with 850nm VCSELs compared to longer wavelength (1300nm and 1550nm) VCSELs?

At 850nm you are growing devices that are all epitaxial - the laser mirrors are grown epitaxially and the quantum wells are grown in one shot. At the other wavelengths, it is much harder.

People have managed it at 1300nm but it is not yet proven to be a reliable material system for getting high-speed operation. When you go to 1550nm, you are doing wafer bonding of the mirrors and active regions or you are doing more complex epitaxial processing.

That is where 850nm VCSELs has a nice advantage in that the whole thing is done in one shot; the epitaxy and the fabrication are relatively simple. You don't have the complex manufacturing of chip parts that you do at 1550nm.

What link distances are served by 850nm VCSELs?

The longest standards are for 500m. As we venture to higher speeds - 28 Gigabit-per-second (Gbps) - 100m is more the maximum. And this trend will continue, at 56Gbps I would anticipate less than 50m and maybe 25m.

The good news is that the number of links that become economically viable at those speeds grows exponentially at these shorter distances. Put another way, copper is very challenged at 56Gbps lane rates and we'll see optics and VCSEL technology move inside the chassis for board-to-board and even chip-to-chip interconnects. Such applications will deliver much higher volumes.

"Taking that next step - turning the 28Gbps VCSEL into a product - is where all the traps lie"

What are the shortest distances?

There are the edge-mounted connections and those are typically 1-5m. There is also a lot of demonstrated work with VCSELs on boards doing chip-to-chip interconnect. That is a big potential market for these devices as well.

The 28Gbps VCSEL has been demonstrated but commercial products are not yet available. It is difficult to sense whether such a device is relatively straightforward to develop or a challenge.

Achieving a 28Gbps VCSEL is hard. Certainly there have been many companies that have demonstrated a modulation capability at that speed. However, it is one thing to do it one time, another to put a reliable VCSEL product into a transceiver with everything around it.

Taking that next step - turning the 28Gbps VCSEL into a product - is where all the traps lie. That is where the bulk of the work is being done today. Certainly this year there will be 25Gbps/ 28Gbps products out in customers' hands.

"With a VCSEL, you have to fill up a volume of active region with enough carriers to generate photons and you can only put in so many, so fast. The smaller you can make that volume, the faster you can lase."

What are the issues that dictate a VCSEL's speed?

When you think about going to the next VCSEL speed, it helps to think about where we came from.

All the devices shipped, from 1 to 10 Gig, had gallium arsenide active regions. It has lots of wonderful attributes but one of its less favourable ones is that it is not the highest speed. Going to 14Gbps and 28Gbps we had to change the active region from gallium arsenide to indium gallium arsenide and that gives us an enhancement of the differential gain, a key parameter for controlling speed.

What you really want to do when you are dealing with speed is that for every incremental bit of current I give the [VCSEL] device, how much more does that translate into gain, or more photons coming out? If you can make that happen more efficiently, then the edge speed of the device increases. In other words, you don't have to deal with other parasitics - carriers going into non-recombination centres and that sort of thing; everything is going into the production of photons rather than other parasitic things.

With a VCSEL, you have to fill up a volume of active region with enough carriers to generate photons and you can only put in so many, so fast. The smaller you can make that volume, the faster you can lase.

Differential gain is a measure of the efficiency in terms of the number of photons generated by a particular carrier. If I can increase that efficiency of making photons, then my transition speed and my edge speed of the laser increases.

Shown is the chart on the y-axis is the differential gain and on the x-axis is the current density going into the part. The decay tells you that if I'm running really high currents, the differential gain is worse for indium gallium arsenide parts. So you want to operate your device with a carrier density that maximises the differential gain.

Part of that maximisation is using less carriers in smaller quantum wells so that it ramps up the curve. You want to operate at a lower current density while also doing a better job of each carrier transitioning into photons.

What else besides differential gain dictates VCSEL performance?

The speed of the laser increases above threshold as the square root of the current. That gives you a return-on-investment in terms of how much current you put into the device.

However, the reliability of the part degrades with the cube of the current you put into it. So you get to a boundary condition where speed varies as the square root of the current and you have the reliability which is degrading with the cube of the current. The intersection of those two points is where you are willing to live in terms of reliability.

That is the trade-off we constantly have to deal with when designing lasers for high speed communications.

Having explained the importance of this region of operation, what changes in terms of the laser when operating at 28Gbps and at 56Gbps?

At 14Gbps and even at 28Gbps the lasers are directly modulated with little analogue trickery. That said, 28Gbps Fibre Channel does allow you to use equalisation at the receiver.

My feeling today is that at 56Gbps, direct modulation of the laser is going to be pretty tricky. At that speed there is going to have to be dispersion compensation or equalisation built into the optical system.

There are a lot of ways to incorporate some analogue or even digital methods to reduce the effective bandwidth of the device from 56Gbps to running less. One of these is a little bit of pre-emphasis and equalisation. Another way is to use analogue modulation levels. Alternatively, you can start borrowing a whole lot more from the digital communication world and look at sub-carrier multiplexing or other more advanced modulation schemes. In other words pull the bandwidth of the laser down instead of doing 1, 0 on-off stuff. At 56 Gig those things are going to be a requirement.

The bottom line is that a 28Gbps VCSEL design maybe something pretty similar to a 56 Gig part with the addition of bandwidth enhancements techniques.

"I can see [VCSEL] modulation rates going to 100Gbps"

So has VCSEL technology already reached its peak?

In terms of direct modulation of a VCSEL - pushing current into it and generating photons - 28 Gig is a reasonable place. And 56 Gig or 40Gig VCSELs may happen with some electronic trickery around it.

The next step - and even at 56Gbps - there is a fair amount of investigation of alternate modulation techniques for VCSELs.

Instead of modulating the current in the active region, you can do passive modulation of an external absorber inside the epitaxial structure. That starts to look like a modulated laser you would see in the telecom industry but it is all grown expitaxially. Once you are modulating a passive component, the modulation speed can get significantly higher. I can see modulation rates going to 100Gbps, for example.

The VCSEL roadmap isn't running out then, but it is getting more complicated. Will it take longer to achieve each device transition: from 28 to 56Gbps, and from 56Gbps to 112Gbps?

A question that is difficult to answer.

The time line will probably scale out every time you try to scale the bandwidth. But maybe not if you are able to do things like combine other technologies at 56Gbps or you do things that are more package related. For example, one way to achieve a 56 Gig link is to multiplex two lasers together on a multi-core fibre. That is significantly less challenging thing to do from a technology development point of view than lasers fundamentally capable of 56Gbps. Is such a solution cost optimised? Well, it is hard to say at this point but it may be time-to-market optimised, at least for the first generation.

Multi-core fibre is one way, another is spatial-division multiplexing. In other words, coarse WDM, making lasers at 850nm, 980nm, 1040nm - a whole bunch of different colours and multiplexing them.

There is more than one way to achieve a total aggregate throughput.

Does all this make your job more interesting, more stressful, or both?

It means I have options in my job which is always a good thing.

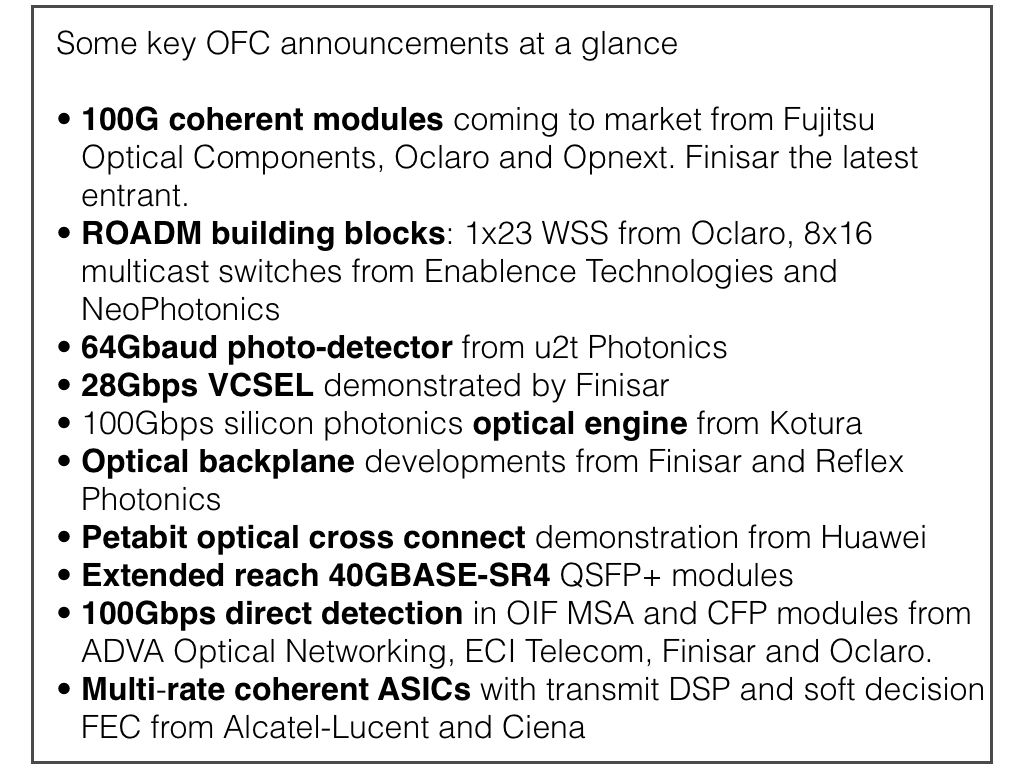

OFC/NFOEC 2012: Some of the exhibition highlights

A round-up of some of the main announcements and demonstrations at the recent OFC/NFOEC 2012 exhibition and conference.

100 Gigabit coherent

Finisar demonstrated its first 100 Gigabit coherent receiver transponder. The 5x7inch dual-polarisation, quadrature phase-shift keying (DP-QPSK) module complies with the Optical Internetworking Forum's (OIF) multi-source specification. The companies joins Fujitsu Optical Components, Opnext and Oclaro that have already detailed their 100 Gigabit coherent modules. Since OFC/NFOEC, Oclaro and Opnext have announced their intention to merge.

"We can take off-the-shelf DSP technology and match it with vertically-integrated optics and come up with a module that is cost effective while enabling higher density for system vendors," says Rafik Ward, vice president of marketing at Finisar. "This will start the shift away from the system vendors' proprietary line cards."

Opnext announced it has demonstrated interoperability between its OMT-100 100 Gigabit-per-second (Gbps) coherent module and 100 Gigabit systems from Fujitsu Optical Systems and NEC. All three designs use NTT Electronics' (NEL) DSP-ASIC coherent receiver chip. "For those that use the same NEL modem chip, we can interoperate with each other," says Ross Saunders, general manager, next-generation transport for Opnext Subsystems.

They come back to folks like us and say: 'If you can hit this price point, then we will use you'

Ross Saunders, Opnext

Oclaro's MI 8000XM 100Gbps module also uses the NEL DSP-ASIC but was not part of the interoperability test sponsored by Japanese operator, NTT.

Oclaro announced its 100Gbps coherent module is now being manufactured using all its own optical components. These include a micro integrated tunable laser assembly (ITLA) - the latest ratified MSA that is more compact and has a higher output power, its modulator and its coherent receiver module.

Using its components enables the company to control performance-cost tradeoffs, says Per Hansen, vice president of product marketing, optical networks solutions at Oclaro: "This [vertical integration] gives us a flexibility we didn’t have in the past."

Finisar is not saying which merchant DSP-ASIC it is using. But like the NEL device, the DSP-ASIC supports soft-decision forward error correction (SD-FEC) to achieve a reach of over 2,000km.

Meanwhile, the module makers' 100Gbps modules are starting to be shipped to customers.

"We shipped [samples] to four customers last quarter and we are probably going to ship to another four or five by the end of this quarter," says Opnext's Saunders.

Opnext says nearly all of its early customers do not have their own in-house 100Gbps developments. However, the systems vendors that have internal 100Gbps programmes have designed their line cards using the same 168-pin interface. This allows them to replace their own 100Gbps daughter cards with a merchant 5x7-inch module.

"This [vertical integration] gives us a flexibility we didn’t have in the past."

"This [vertical integration] gives us a flexibility we didn’t have in the past."

Per Hansen, Oclaro

The company also announced its OTS-100FLX 100Gbps muxponder, transponder and regenerator line cards that use the OTM-100 module and which slot into its OTS-4000 chassis. The chassis supports eight 100Gbps cards. Opnext's smaller 4RU OTS-mini platform hosts two 100Gbps line cards, mounted horizontally. Over half of Opnext's revenues are from subsystems sales which it brands and sells to system vendors.

As for the other 100Gbps transponder makers, Oclaro is sending out its first module samples now. Finisar says its module will be generally available by the year-end, while Fujitsu Optical Components' module was released in April.

Optical components for 200Gbps DP-QPSK

u2t Photonics announced its latest 64Gbaud photo-detector that points to the next speed shift in line-side transmission. The photo-detector is one key building block to the eventual development of a single-carrier DP-QPSK capable of 200Gbps or using 16-QAM, 400Gbps.

"We can already support the higher interface speed and data throughput"

Jens Fiedler, u2t Photonics

"System companies are looking for two things: to increase the baud rate and to use more complex modulation schemes," says Jens Fiedler, vice president sales and marketing at u2t Photonics. "[With this announcement] from the optical component perspective, we can already support the higher interface speed and data throughput."

1x23 Wavelength-selective switch

Oclaro announced a 1x23 wavelength selective switch at OFC. According to Oclaro, the 1x23 WSS has come about due to the operators' desire to support 12-degree nodes: an input port (1 degree) and through-connections on 11 other ports. The remaining 12 [of the WSS's 24 ports] are used as drop ports.

"If for each of those ports you have a fan-out that is steerable to 8 ports, you have 12x8 or 96 as the total channels you can support for a full add-drop," says Hansen. Such a 12-degree, 96-channel requirement was set by operators early on, or at least it was an industry desire, says Hansen.

Switching elements that address these drop requirements - multicast switches - were announced by NeoPhotonics and Enablence Technologies at OFC. The switches, planar lightwave circuit (PLC) hybrid integration designs, implement 8x16 multicast switches.

"The multicast switch takes signals from eight different inputs - 8 different directions in a ROADMs node and distributes those signals to up to 16 drop ports," says Ferris Lipscomb, vice president of marketing at NeoPhotonics.

Such PLC designs are complex, comprising power splitters, waveguide switching, variable optical attenuators and photo-detectors for channel monitoring.

According to NeoPhotonics, the number of optical functions used to implement the multicast switch is in the hundreds.

Enablence already has 8x8 and 8x12 multicast switches and has launched its 8x16 device. Although the company is a hybrid PIC specialist and has PLC technology, it uses polymer PLCs for the multicast designs, claiming they are lower power. NEL is another company offering 8x8 and 8x12 multicast switches.

Passive optical networking

Finisar also demonstrated a mini-PON network, highlighting its optical line terminal (OLT) transceivers, splitters and its latest GPON-stick, an GPON optical network unit built into an SFP. The demo involved using the ONU SFP transceiver in an Ethernet switch port as part of a PON network to deliver high-definition video and audio from the OLT to a high-definition TV.

The company also introduced two splitter products a 1:128 port splitter and a 2:64 (used for redundancy). These high-split ratios are being prepared for the advent of 10 Gigabit PON.

Enablence also demonstrated a WDM-PON 32-channel receiver module at OFC. "It takes 32 TO-can receivers and replaces them with a small module which includes the AWG (arrayed waveguide grating demultiplexer) and the 32 receivers," says Matt Pearson, vice president, technology, optical components division at Enablence Technologies. The design promises to increase system density by fitting two such receivers on a single blade.

Optical engines

Silicon photonics firm, Kotura, detailed its 100Gbps optical engine chip, implemented as a 4x25Gbps design. The optical engine consumes 5W and has a reach of at least 10km, making it suitable for requirements in the data centre including the 100 Gigabit Ethernet IEEE 100GBASE-LR4 standard.

"The 100Gbps chip - 5mmx6mm - is small enough to fit in the QSFP+ and emerging CFP4 optical modules

Arlon Martin, Kotura

Kotura demonstrated to select customers its optical engine. "We are not announcing the product yet," says Arlon Martin, vice president of marketing at Kotura.

Optical engines are used in several applications: pluggable modules on a system's face-plate, the optics at each end of an active optical cable, and for board-mounted embedded applications.

For embedded applications, the optical engine is mounted deeper within the line card, close to high-speed chips, for example, with the signals routed over fibre to the face-plate connector. Using optics rather than high-speed copper traces simplifies the printed circuit board design.Embedded optical engines will also be used for optical backplane-based platforms.

Kotura's silicon photonics-based optical engine integrates all the functions needed for the transmitter and receiver on-chip. These include the 25Gbps optical modulators and drivers, the 4:1 multiplexer and 1:4 demultiplexer and four photo-detectors. To create the lasers, an array of four gain blocks are coupled to the chip. Each of laser's wavelength, around 1550nm, is set using on-chip gratings.

The 100Gbps chip, measuring about 5mmx6mm, is small enough to fit in the QSFP+ and emerging CFP4 optical modules, says Martin. The QSFP+ is likely to be the first application for Kotura's 100Gbps optical engine, used to connect switches within the data centre.

Finisar demonstrated its own VCSEL-based board mount optical assembly - also an optical engine - to highlight the use of the technology for future optical backplanes.

The demonstration, involving Vario-optics and Huber + Suhner, included boards in a chassis. The board includes the optical engine coupled to polymer waveguides from Vario-optics which connect it to a backplane connector, built by Huber + Suhner. "The idea is to show what an integrated optical chassis will look like," says Ward.

Finisar's optical backplane demo using board-mounted optics. Source: Finisar

Finisar's optical backplane demo using board-mounted optics. Source: Finisar

The optical engine comprises 24 channels - 12 transmitters at 10Gbps and 12 receivers in a single board-mounted package. The optics can operate at 10, 12, 14, 25 and 28Gbps, says Finisar. The connector allows the optical engines on different cards to interface via the waveguides. The advantage of polymer waveguides is that they are relatively easy to etch on printed circuit boards and since they replace fibre, they remove fibre management issues. However the technology needs to be proven before system vendors will use such waveguides as standard in their platforms.

Interconnect specialist Reflex Photonics demonstrated an 8.6Tbps optical backplane at OFC. The demonstrator uses Reflex's LightABLE optical engines to implement 864 point-to-point optical fibre links to achieve 8.6Tbps in a single chassis.

The optical fabric comprises six layers of 12x12 fully connected broadcast meshes. Each line card supports 720Gbps into the optical backplane and 60Gbps direct bandwidth between any two cards.

32G Fibre channel

Finisar also highlighted its 28Gbps VCSEL that will be used for the 32 Gigabit Fibre Channel standard. The actual line rate for 32Gbps Fibre Channel is 28.05Gbps. The VCSEL is packaged into a transmitter optical sub-assembly (TOSA) that fits inside a SFP+ module.

"We view 28Gbps VCSEL as strategic due to all the applications it will enable," says Ward.

Besides 32Gbps Fibre Channel, the high-speed VCSEL is suited for the next Infiniband data rate - enhanced data rate (EDR) at 4x25Gbps or 12x25Gbps. There is also standards work in the IEEE for a new 100Gbps Ethernet standard that can use 4x25Gbps VCSELs.

Further reading:

Gazettabyte's full OFC NFOEC 2012 coverage

LightCounting: Notes from OFC 2012: Onset of the Terabit Age

Ovum's OFC coverage

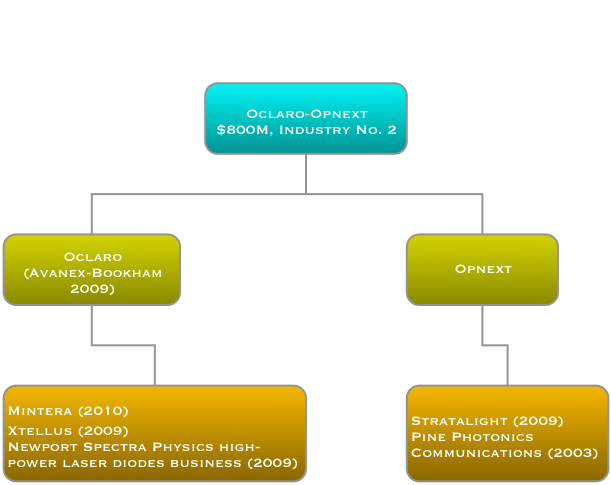

Oclaro-Opnext merger will create second largest optical component company

Oclaro has announced its plan to merge with Opnext. The deal, valued at US $177M, will result in Opnext's shareholders owning 42% of the combined company. The merger of the fifth and sixth largest optical component players, according to Ovum, will create a company with annual revenues of $800M, second only to Finisar. The deal is expected to be completed in the next 3-6 months.

Source: Gazettabyte

Source: Gazettabyte

Other details of the merger include:

- Combining the two companies will save between $35M-45M but will take 18 months to achieve.

- Restructuring and system integration will cost $20M-$30M.

- All five of the new company's fabs will be kept. The fabs are viewed as key assets.

- The new company will continue its use of contract manufacturers in Asia. Oclaro announced a recent deal with Venture, and that included the possibility of an Oclaro-Opnext merger.

- Oclaro's CEO, Alain Couder, will become the CEO of the new company. Harry Bosco, Opnext's CEO, will join the company's board of directors, made up of six Oclaro and four Opnext members.

- In 4Q 2011, Oclaro reported three customers, each accounting for greater than 10% sales: Fujitsu, Infinera and Ciena. Opnext reported 43% of its sales to Cisco Systems and Hitachi in the same period.

Industry scale

The motivation for the merger is to achieve industry scale, says Oclaro. "We have never been shy [of mergers and acquisitions] - we did Avanex and Bookham," says Yves LeMaitre, chief marketing officer for Oclaro. "We believe industry scale allows you to absorb certain fixed costs like fab infrastructure and the sales force." Scale also increases the absolute amount that can be invested in R&D, estimated at 12-13% of its revenues.

"It [the acquisition] is really about building a company that directly competes with Finisar," says Daryl Inniss, practice leader, components at Ovum. "It creates a stronger, vertically integrated company that starts at chips and goes all the way to the line card."

"We will be one of the most vertically integrated suppliers for 100 Gigabit coherent technology"

Mike Chan, Opnext

LightCounting believes the Oclaro-Opnext merger will be a success. Moreover, the market research firm expects further optical component M&As. Since the Oclaro-Opnext was announced, Sumitomo Electric Device Innovations has announced it will acquire Emcore's VCSEL and associated transceiver technology for $17M.

Meanwhile, Morgan Stanley Research is less positive about the merger, believing that the Opnext acquisition carries 'material risk'. It argues that the stated synergies are aggressive and that the integration of the two firms could distract Oclaro and lower its share price.

Products and technology

The deal expands Oclaro's transceiver portfolio, enhancing its offerings in telecom and strengthening its presence in datacom. It also expands the customer base: Opnext supplies Juniper, Google and H-P, new customers for Oclaro.

Common products shared by the two firms are limited, for high-end products the overlap is mainly 100 Gigabit coherent and tunable laser XFPs. LightCounting also points out that the two share some legacy SONET/SDH, WDM and Ethernet products: "Nothing that reduces competition significantly," it says in a research note.

"[With the Avanex-Bookham merger] There was a little bit of overlap in a few areas which we managed," says Oclaro's LeMaitre. "It is even easier in this case."

"We see potential, further down the road, for new very-short-reach optical interfaces"

Yves LeMaitre, Oclaro

Opnext acquired optical transmission subsystem vendor StrataLight in 2009 while Oclaro acquired Mintera in 2010. Both Oclaro and Opnext have used the expertise of the two subsystem vendors to become early market entrants of 100 Gigabit 168-pin multi-source modules.

But Oclaro makes the optical components for the modules - tunable lasers, lithium niobate modulators and integrated coherent transceivers - items that Opnext has to buy for its 100 Gig coherent module, says Ovum's Inniss: "Opnext has built decent gross margins when you consider that a lot of the optics they don't own themselves.” Oclaro's components will be used within Opnext's modules.

"We will be one of the most vertically integrated suppliers for key 100 Gigabit coherent technology moving forward," says Mike Chan, executive vice president of business development and marketing at Opnext.

Opnext stresses that it has its own programmes for integrated photonics. "We have been telling our customers that we have been working on some of these integrated photonics [for 100G coherent]," says Chan. "The StrataLight portion of Opnext also has a lot of work done, and IP created, in the coherent modem area."

Currently both companies' 100 Gigabit modules use NEL's coherent receiver DSP-ASIC. Oclaro has also made an investment in coherent chip start-up, ClariPhy. But for future coherent adaptive-rate designs, the joint company will be able to develop its own coherent chip. "We have the in-house know-how for the coherent modem chip," says Chan.

The merged company is well positioned to address client-side 100 Gigabit-ber-second (Gbps) transceivers. "Here the challenge is to achieve high density and low power [interfaces]," says Chan. Oclaro has VCSEL technology that can be used for very short reach 4x28Gbps arrays. Oclaro says it is the world's leading supplier of VCSELs for a variety of commercial applications and has now shipped over 150M units.

At OFC/NFOEC Opnext demonstrated a 1310nm LISEL (Lens-integrated Surface-Emitting distributed feedback Laser) array operating at 25-40Gbps. The surface-emitting distributed feedback (DFB) laser can also be used for the same 4x28Gbps design, says Chan. "Within the data centre 500m is the sweet-spot," says Chan. "It is not just the physical distance but the link-budget as the signal may have to go through a patch panel." The DFB can be used with multi-mode and single-mode fibre and Opnext believes it can achieve a 1km reach.

Oclaro does not rule out using its VCSEL technology to address such applications as optical engines, connecting racks and for backplanes. "We see potential, further down the road, for new very-short-reach optical interfaces into consumer, backplane, and board-to-board to really expand our addressable market," says LeMaitre

Further mergers

LightCounting argues that the 2011 floods in Thailand have added urgency to industry consolidation, with the Oclaro and Opnext merger being the first of several. Oclaro and Opnext were among the most impacted by the flood with Q4 2011 revenues being down 18% and 38%, respectively, says LightCounting.

Ovum also expects further mergers as companies strengthen their coherent and ROADM technologies.

Inniss believes ROADMs is the next area that Oclaro is likely to strengthen. Oclaro has acquired Xtellus but Ovum says the main ROADM leaders are Finisar, JDS Uniphase and CoAdna. Companies to watch include JDS Uniphase, Fujitsu Optical Components, CoAdna and Sumitomo, says Inniss.

A day after Ovum's and LightCounting's M&A comments, Sumitomo announced the acquisition of Emcore's VCSEL business unit.

Oclaro points its laser diodes at new markets

“To succeed in any market ... you need to be the best at something, to have that sustainable differentiator”

Yves LeMaitre, Oclaro

Now LeMaitre is executive vice president at Oclaro, managing the company’s advanced photonics solutions (APS) arm. The APS division is tasked with developing non-telecom opportunities based on Oclaro’s high-power laser diode portfolio, and accounts for 10%-15% of the company’s revenues.

“The goal is not to create a separate business,” says LeMaitre. “Our goal is to use the infrastructure and the technologies we have, find those niche markets that need these technologies and grow off them.”

Recently Oclaro opened a design centre in Tucson, Arizona that adds packing expertise to its existing high-power laser diode chip business. The company bolstered its laser diode product line in June 2009 when Oclaro gained the Newport Spectra Physics division in a business swap. “We became the largest merchant vendor for high-power laser diodes,” says LeMaitre.

The products include single laser chips, laser arrays and stacked arrays that deliver hundred of watts of output power. “We had all that fundamental chip technology,” says LeMaitre. “What we have been less good at is packaging those chips - managing the thermals as well as coupling that raw chip output power into fibre.”

The new design centre is focussed on packaging which typically must be tailored for each product.

Laser diodes

There are three laser types that use laser diodes, either directly or as ‘pumps’:

- Solid-state laser, known as diode-pumped solid-state (DPSS) lasers.

- Fibre laser, where the fibre is the medium that amplifies light.

- Direct diode laser - here the semiconductor diode itself generates the light.

All three types use laser diodes that operate in the 800-980nm range. Oclaro has much experience in gallium arsenide pump-diode designs for telecom that operate at 920nm wavelengths and above.

Laser diode designs for non-telecom applications are also gallium arsenide-based but operate at 800nm and above. They are also scaled-up designs, says LeMaitre: “If you can get 1W on a single mode fibre for telecom, you can get 10W on a multi-mode fibre.” Combining the lasers in an array allows 100-200W outputs. And by stacking the arrays while inserting cooling between the layers, several hundreds of watts of output power are possible.

The lasers are typically sold as packaged and cooled designs, rather than as raw chips. The laser beam can be collimated to precisely deliver the light, or the beam may be coupled when fibre is the preferred delivery medium.

“The laser beam is used to heat, to weld, to burn, to mark and to engrave,” says LeMaitre. “That beam may be coming directly from the laser [diode], or from another medium that is pumped by the laser [diode].” Such designs require specialist packaging, says LeMaitre, and this is what Oclaro secured when it acquired the Spectra Physics division.

Applications

Laser diodes are used in four main markets which Oclaro values at US$800 million a year.

One is the mature, industrial market. Here lasers are used for manufacturing tasks such as metal welding and metal cutting, marking and welding of plastics, and scribing semiconductor wafers.

Another is high-quality printing where the lasers are used to mark large printing plates. This, says LeMaitre, is a small specialist market.

Health care is a growing market for lasers which are used for surgery, although the largest segment is now skin and hair treatment.

The final main market is consumer where vertical-cavity surface-emitting lasers (VCSELs) are used. The VCSELs have output powers in the tens or hundreds of milliwatts only and are used in computer mouse interfaces and for cursor navigation in smartphones.

“These are simple applications that use lasers because they provide reliable, high-quality optical control of the device,” says LeMaitre. “We are talking tens of millions of [VCSEL] devices [a year] that we are shipping right now for these types of applications.”

Oclaro is a supplier of VCSELs for Light Peak, Intel’s high-speed optical cable technology to link electronic devices. “There will be adoptions of the initial Light Peak starting the end of this year or early next year, and we are starting to ramp up production for that,” says LeMaitre. “In the meantime, there are many alternative [designs] happening – the market is extremely active – and we are talking to a lot of players.” Oclaro sells the laser chips for such interface designs; it does not sell optical engines or the cables.

Is Oclaro pursuing optical engines for datacom applications, linking large switch and IP router systems? “We are actively looking at that but we haven’t made any public announcements,” he says.

Market status

LeMaitre has been at Oclaro since 2008 when Avanex merged with Bookham (to become Oclaro). Before that, he was CEO at optical component start-up, LightConnect.

How does the industry now compare with that of a decade ago?

“At that time [of the downturn] the feeling was that it was going to be tough for maybe a year or two but that by 2002 or 2003 the market would be back to normal,” says LeMaitre. “Certainly no-one expected the downturn would last five years.” Since then, nearly all of the start-ups have been acquired or have exited; Oclaro itself is the result of the merger of some 15 companies.

“People were talking about the need for consolidation, well, it has happened,” he says. Oclaro’s main market – optical components for metro and long haul transmission – now has some four main players. “The consolidation has allowed these companies, including Oclaro, to reach a level of profitability which has not been possible until the last two years,” says LeMaitre.

Demand for bandwidth has continued even with the recent economic downturn, and this has helped the financial performance of the optical component companies.

“The need for bandwidth has still sustained some reasonable level of investment even in the dark times,” he says. “The market is not as sexy as it was in those [boom] days but it is much more healthy; a sign of the industry maturing.”

Industry maturity also brings corporate stability which LeMaitre says provides a healthy backdrop when developing new business opportunities.

The industrial, healthcare and printing markets require greater customisation than optical components for telecom, he says, whereas the consumer market is the opposite, being characterised by vastly greater unit volumes.

“To succeed in any market – this is true for this market and for the telecom market – you need to be the best at something, to have that sustainable differentiator,” says LeMaitre. For Oclaro, its differentiator is its semiconductor laser chip expertise. “If you don’t have a sustainable differentiator, it just doesn’t work.”