Boosting the 100 Gigabit addressable market

Alcatel-Lucent has enhanced the optical performance of its 100 Gigabit technology with the launch of its extended reach (100G XR) line card. Extending the reach of 100 Gigabit systems helps makes the technology more attractive when compared to existing 40 Gigabit optical transport.

"We have built some rather large [data centre to data centre] networks with spans larger that 1,000km in totality"

"We have built some rather large [data centre to data centre] networks with spans larger that 1,000km in totality"

Sam Bucci, Alcatel-Lucent

Used with the Alcatel-Lucent 1830 Photonic Service Switch, the line card improves optical transmission performance by 30% by fine-tuning the algorithm that runs on its coherent receiver ASIC. The system vendor says the typical optical reach extends to 2,000km.

When Alcatel-Lucent first announced its 100 Gigabit technology in June 2010, it claimed a reach of 1,500-2,000km. Now this upper reach limit is met for most networking scenarios with the extended reach performance.

"By announcing the extended reach, Alcatel-Lucent is able to highlight the 2,000km reach as well as draw attention to the fact that it has many deployments already, and that some of those customers are using 100 Gig in 1,000km+ applications," says Sterling Perrin, senior analyst at Heavy Reading.

Market research firm Ovum views the 100G XR announcement as a specific evolutionary improvement.

"But it is significant in that it makes the case for 100 Gig versus 40 Gig more attractive for terrestrial longer-reach applications," says Dana Cooperson, network infrastructure practice leader at Ovum. “The higher the performance vendors can make 100 Gig for more demanding applications - bad fiber, ultra long-haul and ultimately submarine - the quicker it will eclipse 40 Gig.” That said, Ovum does not expect 40 Gig to be eclipsed anytime soon.

100G XR

The line card's improved optical performance equates to transmission across longer fibre spans before optical regeneration is required. This, says the vendor, saves on equipment cost, power and space.

More complex network topologies can also be implemented such as mesh networks where the signal can encounter varying-length paths based on differing fibre types as well as multiple ROADM stages. Alcatel-Lucent says it has implemented a 1,700km link with 20 amplifiers and seven ROADM stages without the need for signal regeneration.

The improved optical performance of the 100G XR has been achieved without changing the line card's hardware. The card uses the same analogue-to-digital converter, digital signal processor (DSP) ASIC and the same forward error correction scheme used for its existing 100 Gigabit line card.

What has changed is the dispersion compensation algorithm that runs on the DSP, making use of the experience Alcatel-Lucent has gained from existing 100 Gigabit deployments.

"We can tune various parameters, such as power and the way it [the algorithm] deals with impairments," says Sam Bucci, vice president, terrestrial portfolio management at Alcatel-Lucent. In particular the 100G XR has increased tolerance to polarisation mode dispersion and non-linear impairments.

Cooperson says Alcatel-Lucent has adjusted the receiver ASIC performance after 'mining' data from coherent deployments, something the company is used to doing with its wireless networks. She says Alcatel-Lucent has also worked closely with component vendors to achieve the improved performance.

Perrin points out that Alcatel-Lucent's 100 Gig design uses a single laser while Ciena's system is dual laser. "Alcatel-Lucent is saying that over an identical plant the two-laser approach has no distance advantages over the one laser approach," he says. However, other system vendors have announced distances at and beyond 2,000km. "So Alcatel-Lucent's enhanced system is not record-setting," says Perrin.

100 Gigabit Market

Alcatel-Lucent says it has more than 45 deployments comprising over 1,200 100 Gig lines since the launch of its 100 Gigabit system in 2010.

"It appears that Alcatel-Lucent has shipped more 100G line cards than anyone," says Cooperson. "Alcatel-Lucent has a good opportunity to make some serious 100 Gig inroads here, along with Ciena, while everyone else gears up to get their solutions to market in 2012."

Cooperson also says the 100G XR announcement dovetails nicely with Alcatel-Lucent’s recent CloudBand announcement. Indeed Bucci says that its deployments of 100 Gig include connecting data centres: "We have built some rather large [data centre to data centre] networks with spans larger that 1,000km in totality."

The 100G XR card is being tested by customers and will be generally available starting December 2011.

Is optical components becoming a buyer's market?

"An organisation's gross margins ride on these new products"

Daryl Inniss, Ovum Components.

The global optical component market was down 2% in the second quarter of 2011 at US $1.55 billion, according to Ovum.

The good news is that the market research company is forecasting that modest growth will resume this quarter now that the build-up in component inventory that led to the market contraction has largely been worked through.

But Ovum is warning that there are signs that the continued weak market conditions and fierce competition could lead to sharp price declines even for newer, high-valued products. "An organisation's gross margins ride on these new products," says Daryl Inniss, practice leader, Ovum Components.

Oclaro's CEO on a recent earnings call said he was being asked for price concessions on 40Gbps products. Ovum also says the ROADM and tunable laser XFPs markets are becoming more crowded and competitive.

Inniss stresses that there is no evidence that companies are cutting prices to gain an edge but while he expects volumes will grow, intense pricing pressure should now be expected.

LightCounting points out that the slowdown in sales of optical component and modules in early 2011 has been limited to products that did very well in 2010 or which had long lead times, like wavelength-selective switches for ROADMs and 40Gbps modules. It says there is little, if any, excess inventory of components accumulated across the broader market.

"The telecom transceiver market remained steady in Q1 2011, but it declined further in Q2 mostly due to lower sales of 40Gig client-side modules," says Vladimir Kozlov, CEO of LightCounting. "We expect that by the end of this year, the telecom market segment will be strong again."

Best in a decade

The second quarter market dip follows a period where the optical components industry experienced its strongest yearly growth for a decade. The market reached US $6 billion for the year ending first quarter 2011 - a first since 2001.

So long as network expansion keeps up with traffic, we are looking at sustainable growth”

So long as network expansion keeps up with traffic, we are looking at sustainable growth”

Vladimir Kozlov, LightCounting

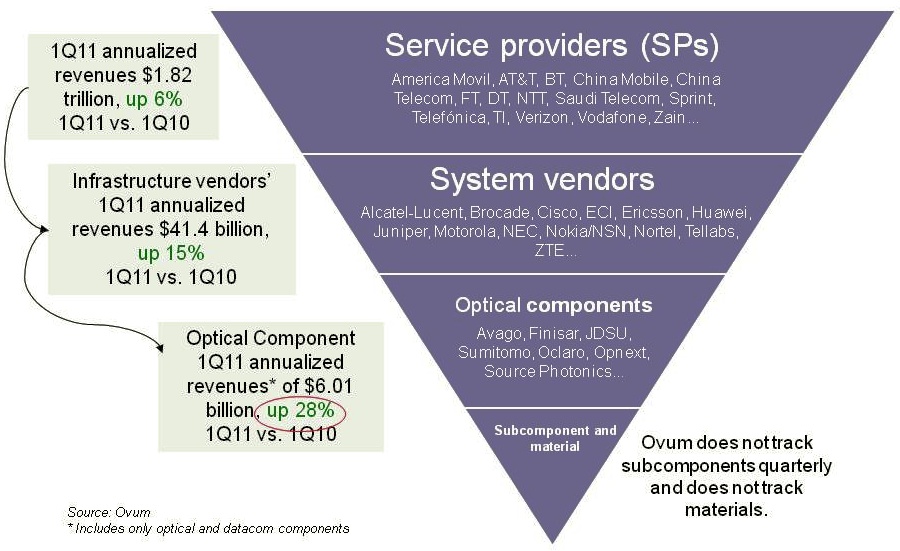

The six quarters of consecutive market growth up to the second quarter was due partly to the overall health of the telecom industry. The service provider industry - wireless and wireline - grew 6% year-on-year between 2Q10 and 1Q11, to reach $1.82 trillion. In turn, the equipment market, mainly telecom vendors but including the likes of Brocade, grew 15% to $41.4 billion.

Ovum attributes the 28% growth in optical components between 2Q10 and 1Q 2011 to strong growth in the fibre-to-the-x (FTTx) market as well as new revenues entering the market from datacom players. A third factor was optical equipment vendors over-ordering long lead-time items – such as ROADMs – to secure supply.

“ROADMS did grow nicely but if you look at wavelength-selective switches, it is not such a big market," says Kozlov. The market research firm says the wavelength-selective switch market was $280 million in 2010.

LightCounting says 10 Gigabit SFP+ optical transceivers was a market highlight in 2010, with volume shipments tripling. Ethernet SFP+ sales alone reached $180 million in 2010, and will grow to $250 million this year.

“The optical component market grew 36% in 2010, and in 2011 we’re projecting it will grow 7%,”says Inniss

But competition is intense. Finisar may be the market leader but only 4% market share separates the players in second through to sixth place, says Ovum. “It’s a very competitive market and there is no breakaway here,” says Inniss.

Another challenge is the emergence of the Chinese optical component players. The large-scale deployment of FTTx being undertaken by the main three Chinese operators means that there is a huge market opportunity for local optical component and module players. The Chinese market also accounts for half the all 40 Gigabit-per-second shipments, according to Infonetics Research.

“Looking at the western suppliers, everyone is reporting slowdowns and drops in the second quarter [of 2011],” says Kozlov. “Yet from the data we are getting from the Chinese optical component players, they grew 35% in 2010 and are on track for 30% growth this year.”

Another challenge is for firms to fund sufficient R&D. Share prices took a severe hit after the companies issued warnings about second-quarter sales. “The entire optical component market is depressed because of the localised correction,” says Inniss. “It will still grow but because it is so much smaller than 2010, capital markets are bashing the companies.”

Since the stock market is an important source of investment, it may take several years for the market to recover the share price levels at the start of 2011. “It won’t stop investment in technology but there is going to be real hard eyes on each decision that is made,” says Inniss.

The main challenge facing optical component players is not so much technical issues but more the requirement to continually decrease costs. This is not new but neither is it going away, says Inniss.

Positive outlook

Yet the analysts expect market growth to continue.

Inniss points to the growing role of optics for short-distance interfaces: “The I/O (input-output) bandwidth requirements are sufficiently high, whether it is the backplane or chip-to-chip connections, that the market realisation is that optics will play a role.”

Ovum also highlights consumer market developments such as the USB 3.0 interface which will drive the market for active optical cables. “It [the consumer market] is not going to happen tomorrow - meaning 2012 - but it is something that is coming and has the potential to transform the industry,” says Inniss.

“Companies such as Finisar and Avago [Technologies] are becoming more assertive in enforcing their intellectual rights,” says Kozlov. This is as a positive development that has been missing in the past: “Protecting your intellectual property ultimately helps you become profitable,” he says.

LightCounting also highlights the need for network investment to keep track with traffic growth. "So long as network expansion keeps up with traffic, we are looking at sustainable growth,” says Kozlov. See Plotting transceiver shipments versus traffic growth.

This article is based on a piece that appeared in the ECOC 2011 exhibition guide.

Optical components: The six billion dollar industry

The service provider industry, including wireless and wireline players, is up 6% year-on-year (2Q10 to 1Q11) to reach US $1.82 trillion, according to Ovum. The equipment market, mainly telecom vendors but also the likes of Brocade, has also shown strong growth - up 15% - to reach revenues of over $41.4 billion. But the most striking growth has occurred in the optical components market, up 28%, to achieve revenues of over $6 billion, says the market research firm.

Source: Ovum

Source: Ovum

“This is the first time optical components has exceeded six billion since 2001,” says Daryl Inniss, practice leader, Ovum Components. Moreover, the optical component industry growth has continued over six consecutive quarters with the growth being more than 25% for the past four quarters. “None of the other [two] segments have performed in this way,” says Inniss.

Ovum cites three factors accounting for the growth. Fibre-to-the-x (FTTx) is experiencing strong growth while revenues have entered the market from datacom players from the start of 2010. “The [optical] component recovery was led by datacom,” says Inniss. “We speculate that some of that money came from the Googles, Facebooks and Yahoos!.” A third factor accounting for growth has been optical equipment vendors ordering more long lead-time items than needed – such as ROADMs – to secure supply.

Source: Ovum

Source: Ovum

The second chart above shows the different market segments normalised since the start of 1999. Shown are the capex spending for optical networking, optical networking equipment revenues, optical components and FTTx equipment spending.

Optical networking spending is some 3.5x that of the components. FTTx equipment revenues are lower than the optical component industry’s and is therefore multiplied by 2.25, while capex is 9.2x that of optical equipment. The peak revenue in 2001 is the optical component revenues during the optical boom.

Several points can be drawn from the normalised chart:

- The strong recent growth in FTTx is the result of the booming Chinese market.

- From 2003 to 2008, the overall market showed steady growth, as illustrated by the best-fit line.

- From 2003 to 2008, capex and optical networking revenues were in line, while two thirds of the optical component revenues were due to this telecom spending.

- From 2010 onwards, components deviated from these two other segments due to the datacom spending from new players and the strong growth in FTTx.

- Once the market crashed in early 2009, optical components, networking and capex all fell. FTTx recovered after only one quarter and was followed by optical components. Optical networking and capex, meanwhile, have still not fully recovered when compared with the underlying growth line.

Google and the optical component industry

According to a report by Pauline Rigby, Google wants something in between two existing IEEE interface standards. The 100GBase-SR10, which has 10 parallel channels and a 125m span, has too short a reach for Google.

“What is good for an 800-pound gorilla is not necessarily good for the industry. It [Google] should have been at the table when the IEEE was working on the standard."

Daryl Inniss, practice leader, components, Ovum

The second interface, the 100GBase-LR4, uses four channels that are multiplexed onto a single fibre and has a 10km reach. The issue here is that Google doesn’t need a 10km reach and while a single fibre is better than the multi-mode fibre based SR10, the interface is costly with its “gearbox” IC that translates between 10 lanes of 10Gbps and four lanes each at 25Gbps. Both IEEE interfaces are also implemented using a CFP form factor which is bulky.

What Google wants

Google wants optical component vendors to develop a new 100 Gigabit Ethernet multi-source agreement (MSA) that is based on a single-mode interface with a 2km reach, reports Rigby. Such a design would use a ten-channel laser array whose output is multiplexed onto a fibre, a similar laser array-multiplexer arrangement that has already been developed by Santur. Using such a part, the new interface could be developed quickly and cheaply, says Google.

The proposed interface clearly has merits and Google, an important force with an appetite for optics, makes some valid points. But the industry is developing 4x25Gbps interfaces and while such interfaces may be challenging, no-one doubts they will come.

Google’s next moves

Google has a history of being contrarian if it believes it best serves its business. The way the internet giant designs data centres is one example, using massive numbers of cheap servers arranged in a fault-tolerant architecture.

But there is only so much it can do in-house and developing a new optical interface will require help from optical component players.

Google has the financial muscle to hire an optical component firm to engineer and manufacture a custom interface. A recent example of such a partnership is IBM's work with Avago Technologies to develop board-level optics – or an optical engine – for use within IBM’s POWER7 supercomputer systems.

According to Karen Liu, vice president, components and video technologies at market research firm Ovum, once such an interface is developed, Google could allow others to buy it to help reduce its price. “Remember the Lucent form factor which became a de facto standard but wasn’t originally intended to be?” says Liu. “This approach could work.”

Taking a longer term view, Google could also invest in optical component start-ups. The return may take years and as the experience of the last decade has shown, optical components is a risky business. But Google could encourage a supply of novel, leading-edge technologies over the next decade.

The optical component industry is right to push back with regard Google’s request for a new 100 Gigabit Ethernet MSA, as Finisar has done. While Google may be an important player that can drive interface requirements, many players have helped frame the IEEE 100Gbps Ethernet standards work. In the last decade the optical industry has also seen other giant firms try to drive the industry only to eventually exit.

“The industry needs to move on,” says Daryl Inniss, practice leader, components at Ovum. “What is good for an 800-pound gorilla is not necessarily good for the industry.” Inniss also suggests a simple and effective way Google could have influenced the 100 Gigabit Ethernet MSA work: “It [Google] should have been at the table when the IEEE was working on the standard."

Ciena post-MEN

“The 40G and 100G technology were key to the deal and we made sure that the core team was still there”

Tom Mock, Ciena

The company has announced the CN 5150 service aggregation switch, added Nortel’s 40 Gigabit-per-seconds (Gbps) coherent transmission technology to its flagship CN 4200 platform, and announced 140 job cuts, mostly in Europe. US operator AT&T has also selected the company as one of two suppliers of its optical and transport equipment.

Ciena provides optical transport, optical switching and Carrier Ethernet equipment. “We were finding it difficult to fund the required R&D in all three segments,” says Tom Mock, senior vice president of strategic planning at Ciena. “We saw this [the MEN acquisition] as an opportunity to bring good technology on board and give the company the scale needed to execute in these technology areas.”

According to Mock, Ciena was one of several firms interested in the Nortel unit but that Nokia Siemens Networks was the main counter-bidder in the auction process. Ciena won after agreeing to pay US $773.8 million, gaining MEN’s R&D group and associated sales and marketing.

In particular, it gained the R&D for optical transport – Nortel’s Optical Multiservice Edge (OME) 6500 product line for 40Gbps and 100Gbps, the Optical Metro 5200 metro and enterprise platform, Carrier Ethernet, and the R&D for software and network management. Most of these activities are based in Ottawa, Ontario.

“We had pretty good solutions in optical switching and carrier Ethernet but we were looking for a stronger transport offering, which is what Nortel brought to us,” says Mock. The acquisition, which effectively doubles the company’s size, means that Ciena now plays in a “$18 billion sandbox” comprising optical networking and Ethernet transport and services, according to market research firm Ovum.

Did Ciena secure Nortel’s MEN’s key staff, given the lengthy period – over a year – to complete the acquisition? “We agreed with Nortel that we would get 2000 staff out of a total of 2300 staff,” says Mock.

Yet Ciena had no visibility regarding staff since Nortel remained a competitor until the deal was completed. “We were very pleasantly surprised at the quality of the people who were in MEN,” says Mock. “When companies are in hard times the best people begin to leave, and because of the uncertainty I’m sure some people did leave.”

Ciena claims it secured MEN’s core 40 and 100Gbps team despite announcements such as Infinera's that it had recruited John McNicol, a senior engineer involved in the development of Nortel’s coherent technology. “The 40G and 100G technology were key to the deal and we made sure that the core team was still there,” says Mock.

He also dismisses the view that Nortel’s 100Gbps coherent technology market lead has been eroded due to the uncertainty. Mock claims it has a 12- to 18-month lead and points to Verizon Business’ deployment of Nortel’s 100Gbps system in late 2009 as proof that MEN continued to push the technology.

Strategy

Ciena’s primary focus is on what it calls carrier optical Ethernet, described by Mock as the marrying of the capacity scaling and reliability of optical transport with the ubiquity, flexibility and economics of Ethernet.

For Ciena this translates to three main product lines:

- Packet optical transport, primarily optical transport with some aggregation.

- Packet optical switching based on Ciena’s CoreDirector platform with its time-division multiplexing (TDM) and Ethernet switching, as well as control plane technology.

- Carrier Ethernet service delivery.

According to Ovum, Ciena is now the third “billion dollar club” optical networking vendor member with a 9% market share, behind Huawei and Alcatel-Lucent, with 24% and 19%, respectively. It also becomes the North American leader, with a 20% share while improving its standing in all other regional markets. In contrast, for Ethernet the combined company had only 3% share in 2009. “We are emerging as a leader in the Carrier Ethernet space,” claims Mock. “In 4Q 2009 we were leading in North America, according to Heavy Reading.”

Ciena sees optical transport and switching blurring but says that most of its customers still see these as separate products. “Both our packet optical switching and packet optical transport platforms can be used in these applications, for example the OME 6500 is looked at as a transport device but it has TDM and packet switching as well,” says Mock. But with time Ciena says optical switching and optical transport product families will increasingly consolidate.

What next?

Having completed the deal, one of the first things Ciena did was determine its product portfolio and tell its operator customers its plans.

Issues set to preoccupy Ciena for the next 12 to 18 months include the integration of Nortel’s 40Gbps and 100Gbps technology onto Ciena’s transport and switching platforms, getting the control plane of Ciena’s switching product integrated onto Nortel’s products, and bringing all the products under common network management.

At OFC/ NFOEC 2010 Ciena showcased Nortel’s OME 6500 transmitting over Ciena’s CN 4200 line system with both being overseen by Ciena’s OnCenter management software. “I wouldn’t point to the network management integration as a finished product but a step along the path,” says Mock.

According to Ovum, the demonstrations included 100Gbps over 1,500km of Corning ultra-low-loss fiber, 100Gbps over 800km in the presence of large and fast polarisation mode dispersion transients, and 40Gbps ultra-long haul transmission over 3,500km.

Ciena has said it expects its business to grow at least at the market rate: 10 to 12 percent yearly.

AT&T domain supplier

In April, AT&T announced that it had selected Ciena as a domain supplier. AT&T's domain supplier programme involves the operator splitting its networking requirements across several technologies, choosing two players for each domain. AT&T plans to work closely with each domain supplier ensuring that AT&T gains equipment tailored to its requirements while vendors such as Ciena can focus their R&D spending by seeing early the operator’s roadmap.

Did Ciena acquire Nortel to become a domain partner? “We would not make an acquisition to win the business of any one carrier,” says Mock. “But we realised that if we going to be a significant player in next-generation infrastructure we needed a certain critical mass, in portfolio and market coverage globally.

“Did we get selected because of Nortel, it’s hard to say – I’m sure it didn’t hurt - but we've been a supplier to AT&T for 10 years,” says Mock. He also highlights the operator’s own announcement to explain Ciena’s selection: “They talk about two technologies in particular – 100Gbps technology and Optical Transport Networking (OTN).”

Ovum argues in its “Telecoms in 2020: network infrastructure” report that the future prospects of specialist vendors will be as rosy as full-service ones. “We do view ourselves as specialists even though we’ve essentially doubled the size of the company, and there is absolutely a place for specialist companies as they are genuinely more agile,” says Mock.

Mock also expects further system vendor consolidation. “Optical transport remains fragmented so there are opportunities for further consolidation,” he says. Fragmented in what way? “If you look at the router space there are two dominant players, in optical transport there are 10 – no-one has a 40 to 50 percent market share.”

Is a datacom and telecom mini-boom taking place?

Daryl Inniss believes it is largely a reflection of cutbacks that have run their course. “The industry cut back swiftly and deeply when the market started to tank, cutting suppliers and capacity,” says Inniss, practice leader, components at market research firm Ovum.

“I think it's recovery dynamics - people ordering a tiny bit more and there are no parts available such that lead-times are stretching out simulating a boom.”

Brad Smith, LightCounting

Carriers supported the demand with inventory. “Now the industry needs to support both deployments and inventory and with the traffic continuing to grow suppliers cannot meet demand,” he says. Moreover this “bull-whip effect” impacts most severely suppliers furthest removed from the carriers i.e. component vendors.

Brad Smith, senior vice president at optical transceiver market research firm LightCounting, also explains the situation based on events last year.

“There is a shortage of certain parts in optical and semis as a result of cutbacks in manufacturing during 2009,” says Smith, “I think it's recovery dynamics - people ordering a tiny bit more and there are no parts available such that lead-times are stretching out simulating a boom.”

Late last year a research note highlighted industry reports that shortages were becoming more widespread, including components such as integrated circuits and fiber optic transceivers.

However one leading optical transceiver vendor commented that it is shipping everything it can make and that it can’t build stuff fast enough.

So is there a mini-boom after all?

Differentiation in a market that demands sameness

At first sight, optical transceiver vendors have little scope for product differentiation. Modules are defined through a multi-source agreement (MSA) and used to transport specified protocols over predefined distances.

“Their attitude is let the big guys kill themselves at 40 and 100 Gig while they beat down costs"

Vladimir Kozlov, LightCounting

“I don’t think differentiation matters so much in this industry,” says Daryl Inniss, practice leader components at Ovum. “Over time eventually someone always comes in; end customers constantly demand multiple suppliers.”

It is a view confirmed by Luc Ceuppens, senior director of marketing, high-end systems business unit at Juniper Networks. “We do look at the different vendors’ products - which one gives the lowest power consumption,” he says. “But overall there is very little difference.”

For vendors, developing transceivers is time-consuming and costly yet with no guarantee of a return. The very nature of pluggables means one vendor’s product can easily be swapped with a cheaper transceiver from a competitor.

Being a vendor defining the MSA is one way to steal a march as it results in a time-to-market advantage. There have even been cases where non-founder companies have been denied sight of an MSA’s specification, ensuring they can never compete, says Inniss: “If you are part of an MSA, you are very definitely at an advantage.”

Rafik Ward, vice president of marketing at Finisar, cites other examples where companies have an advantage.

One is Fibre Channel where new data rates require high-speed vertical-cavity surface-emitting lasers (VCSELs) which only a few companies have.

Another is 100 Gigabit-per-second (Gbps) for long-haul transmission which requires companies with deep pockets to meet the steep development costs. “One hundred Gigabit is a very expensive proposition whereas with the 40 Gigabit Ethernet LR4 (10km) standard, existing off-the-shelf 10Gbps technology can be used,” says Ward.

"One hundred Gigabit is a very expensive proposition"

"One hundred Gigabit is a very expensive proposition"

Rafik Ward, Finisar

Ovum’s Inniss highlights how optical access is set to impact wide area networking (WAN). The optical transceivers for passive optical networking (PON) are using such high-end components as distributed feedback (DFB) lasers and avalanche photo-detectors (APDs), traditionally components for the WAN. Yet with the higher volumes of PON, the cost of WAN optics will come down.

“With Gigabit Ethernet the price declines by 20% each time volumes double,” says Inniss. “For PON transceivers the decline is 40%.” As 10Gbps PON optics start to be deployed, the price benefit will migrate up to the SONET/ Ethernet/ WAN world, he says. Accordingly, those transceiver players that make and use their own components, and are active in PON and WAN, will most benefit.

“Differentiation is hard but possible,” says Vladimir Kozlov, CEO of optical transceiver market research firm, LightCounting. Active optical cables (AOCs) have been an area of innovation partly because vendors have freedom to design the optics that are enclosed within the cabling, he says.

AOCs, Fibre Channel and 100Gbps are all examples where technology is a differentiator, says Kozlov, but business strategy is another lever to be exploited.

On a recent visit to China, Kozlov spoke to ten local vendors. “They have jumped into the transceiver market and think a 20% margin is huge whereas in the US it is seen as nothing.”

The vendors differentiate themselves by supplying transceivers directly to the equipment vendors’ end customers. “They [the Chinese vendors] are finding ways in a business environment; nothing new here in technology, nothing new in manufacturing,” says Kozlov.

He cites one firm that fully populated with transceivers a US telecom system vendor’s installation in Malaysia. “Doing this in the US is harder but then the US is one market in a big world,” says Kozlov.

Offshore manufacturing is no longer a differentiator. One large Chinese transceiver maker bemoaned that everyone now has manufacturing in China. As a result its focus has turned to tackling overheads: trimming costs and reducing R&D.

“Their attitude is let the big guys kill themselves at 40 and 100 Gig while they beat down costs by slashing Ph.Ds, optimising equipment and improving yields,” says Kozlov. “Is it a winning approach long term? No, but short-term quite possibly.”

Do multi-source agreements benefit the optical industry?

System vendors may adore optical transceivers but there is a concern about how multi-source agreements originate.

Optical transceiver form factors, defined through multi-source agreements (MSAs), benefit equipment vendors by ensuring there are several suppliers to choose from. No longer must a system vendor develop its own or be locked in with a supplier.

“Personally, the MSA is the worst thing that has happened to the optical industry”

“Personally, the MSA is the worst thing that has happened to the optical industry”

Marek Tlaka, Luxtera

Pluggables also decouple optics from the line card. A line card can address several applications simply by replacing the module. In contrast, with fixed optics the investment is tied to the line card. A system can also be upgraded by swapping the module with an enhanced specification version once it is available.

But given the variety of modules that datacom and telecom system vendors must support, there are those that argue the MSA process should be streamlined to benefit the industry.

Traditionally, several transceiver vendors collaborate before announcing an MSA. The CFP MSA announced in March 2009, for example, was defined by Finisar, Opnext and Sumitomo Electric Device Innovations. Since then Avago Technologies has become a member.

“The industry has an interesting model,” says Niall Robinson, vice president of product marketing at Mintera. “A couple of companies can get together, work behind closed doors and announce suddenly an MSA and try to make it defacto in the market.”

Robinson contrasts the MSA process with the Optical Interconnecting Forum’s (OIF) 100Gbps line side work that defined guidelines for integrated transmitter and receiver modules. Here service providers and system vendors also contributed. “It was a much more effective and fair process, allowing for industry collaboration,” says Robinson

Matt Traverso, senior manager, technical marketing at Opnext, and involved in the CFP MSA, also favours an open process. “But the view that the way MSAs are run is not open is a bit of a fallacy,” he says.

“Any MSA that is well run requires iteration with suppliers,” says Traverso. The opposite is also true: poorly run MSAs have short lives, he says. Having too open a forum also runs the risk of creating a one-size-fits-all: “One vendor may want to use the MSA as a copper interface while a carrier will want it for long-haul dense WDM.”

Optical transceiver vendors benefit in another way if they are the ones developing MSAs. “Transceiver vendors will not make life tough for themselves,” says Padraig OMathuna, product marketing director at optical device maker, GigOptix. “If MSAs are defined by system vendors, [transceiver] designs would be a lot more challenging.”

Avago Technologies argues for standards bodies to play a role especially as industry resources become more thinly spread.

“MSAs are not standards; there are items left unwritten and not enough double checking is done,” says Sami Nassar, director of marketing, fiber optic products division at Avago Technologies. There are always holes in the specifications, requiring patches and fixes. “If they [transceivers] were driven by standards bodies that would be better,” says Nassar.

Organisations such as the IEEE don’t address packaging and connectors as part of their standards work. But this may have to change. “The real challenge, as the industry thins out, is ensuring the [MSA] work is thorough,” says Dan Rausch, Avago’s senior technical marketing manager, fiber optic products division. “The challenge for the industry going forward is ensuring good engineering and more robust solutions.”

Marek Tlalka, vice president of marketing at Luxtera, goes further, questioning the very merits of the MSA: “Personally, the MSA is the worst thing that has happened to the optical industry.”

Unlike the semiconductor industry where a framer chip once on a line card delivers revenue for years, a transceiver company may design the best product yet six months later be replaced by a cheaper competitor. “The return on investment is lost; all that work for nothing,” says Tlalka.

“Is it a good development or not? MSAs are out there,” says Vladimir Kozlov, CEO of optical transceiver market research firm, LightCounting. “It helps system vendors, giving them a freedom to buy.”

But MSAs have squeezed transceiver makers, says Kozlov, and he worries that it is hindering innovation as companies cut costs to maximize their return on investment.

“There is continual pressure to reduce the price of optics,” adds Daryl Inniss, Ovum’s practice leader components. If operators are to provide video and high definition TV services and grow revenues then bandwidth needs to become dirt cheap. “Even today optics is not cheap,” says Inniss. Certainly MSAs play an important role in reducing costs.

“The transceiver vendors’ challenge is our benefit,” admits Oren Marmur, vice president, optical networking line of business, network solutions division at system vendor, ECI Telecom. “But we have our own challenges at the system level.”