Access drives a need for 10G compact aggregation boxes

Infinera has unveiled a platform to aggregate multiple 10-gigabit traffic streams originating in the access network.

The 1.6-terabit HDEA 1600G platform is designed to aggregate 80, 10-gigabit wavelengths. The use of ten-gigabit wavelengths in access continues to grow with the advent of 5G mobile backhaul and developments in cable and passive optical networking (PON).

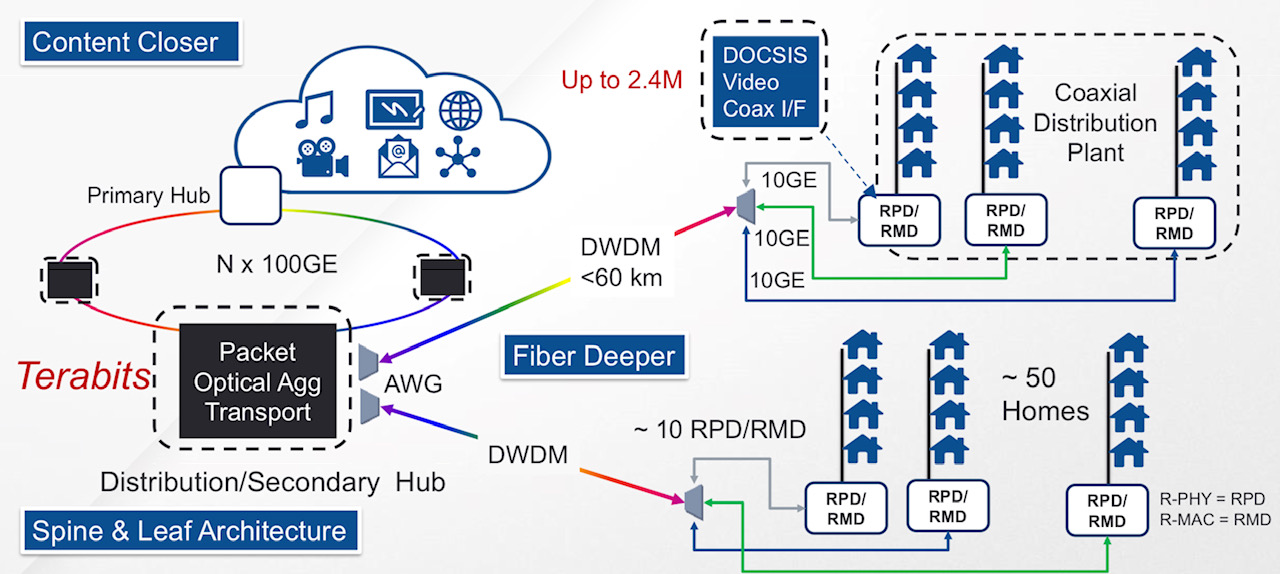

A distributed access architecture being embraced by cable operators. Shown are the remote PHY devices (RPD) or remote MAC-PHY devices (RMD), functionality moved out of the secondary hub and closer to the end user. Also shown is how DWDM technology is moved closer to the edge of the network. Source: Infinera.

A distributed access architecture being embraced by cable operators. Shown are the remote PHY devices (RPD) or remote MAC-PHY devices (RMD), functionality moved out of the secondary hub and closer to the end user. Also shown is how DWDM technology is moved closer to the edge of the network. Source: Infinera.

Infinera has adopted a novel mechanical design for its 1 rack unit (1RU) HDEA 1600G that uses the sides of the platform to fit 80 SFP+ optical modules.

The platform also features a 1.6-terabit Ethernet switch chip that aggregates the traffic from the 10-gigabit streams to fill 100-gigabit wavelengths that are passed to other switching or transport platforms for transmission into the network.

Distributed access architecture

Jon Baldry, metro marketing director at Infinera, cites the adoption of a distributed access architecture (DAA) by cable operators as an example of 10-gigabit links that are set to proliferate in the access network.

DAA is being adopted by cable operators to compete with the telecom operators’ rollout of fibre-to-the-home (FTTH) broadband access technology.

A recent report by market research firm, Ovum, addressing DAA in the North American market, discusses how the architectural approach will free up space in cable headends, reduce the operators’ operational costs, and allow the delivery of greater bandwidth to subscribers.

Implementing DAA involves bringing fibre as well as cable network functionality closer to the user. Such functionality includes remote PHY devices and remote MAC-PHY devices. It is these devices that will use a 10-gigabit interface, says Baldry: “The traffic they will be running at first will be two or three gigabits over that 10-gigabit link.”

Julie Kunstler, principal analyst at Ovum’s Network Infrastructure and Software group, says the choice whether to deploy a remote PHY or a remote MAC-PHY architecture is a issue of an operator's ‘religion’. What is important, she says, is that both options exploit the existing hybrid fibre coax (HFC) architecture to boost the speed tiers delivered to users.

The current, pre-DAA, cable network architecture. Source: Infinera.

In the current pre-DAA architecture, the cable network comprises cable headends and secondary distribution hubs (see diagram above). It is at the secondary hub that the dense wavelength-division multiplexing (DWDM) network terminates. From there, RF over fibre is carried over the hybrid fibre-coax (HFC) plant. The HFC plant also requires amplifier chains to overcome cable attenuation and the losses resulting from the cable splits that deliver the RF signals to the homes.

Typically, an HFC node in the cable network serves up to 500 homes. With the adoption of DAA and the use of remote PHYs, the amplifier chains can be removed with each PHY serving 50 homes (see diagram top).

“Basically DWDM is being pushed out to the remote PHY devices,” says Baldry. The remote PHYs can be as far as 60km from the secondary hub.

“DAA is a classic example where you will have dense 10-gigabit links all coming together at one location,” says Baldry. “Worst case, you can have 600-700 remote PHY devices terminating at a secondary hub.”

The same applies to cellular.

At present 4G networks use 1-gigabit links for mobile backhaul but 5G will use 10-gigabit and 25-gigabit links in a year or two. “So the edge of the WDM network has really jumped from 1 gigabit to 10 gigabit,” says Baldry.

It is the aggregation of large numbers of 10-gigabit links that the HDEA 1600G platform is designed to address.

HDEA 1600G

Only a certain number of pluggable interfaces can fit on the front panel of a 1RH box. To accommodate 80, 10-gigabit streams, the two sides of the platform are used for the interfaces. Using the HDEA’s sides creates much more space for the 1RU’s input-output (I/O) compared to traditional transport kit, says Baldry.

The 40 SFP+ modules on each side of the platform are accessed by pulling the shelf out and this can be done while it is operational (see photo below). Such an approach is used for supercomputing but Baldry believes Infinera is the first to adopt it for a transport product.

Infinera has also adopted MPO connectors to simplify the fibre management involved in connected 80 SFP+, each module requiring a fibre pair.

The HDEA 1600 has two groups of four MPO connectors on the front panel. Each MPO cluster connects 40 modules on each side, with each MPO cable having 20 fibres to connect 10 SFP+ modules.

A site terminating 400 remote PHYs, for example, requires the connection of 40 MPO cables instead of 800 individual fibres, says Baldry, simplifying installation greatly.

>

“DAA is a classic example where you will have dense 10-gigabit links all coming together at one location. Worst case, you can have 600-700 remote PHY devices terminating at a secondary hub.”

The other end of the MPO cable connects to a dense multiplexer-demultiplexer (mux-demux) unit that separates the individual 10-gigabit access wavelengths received over the DWDM link.

Each mux-demux unit uses an arrayed waveguide grating (AWG) that is tailored to the cable operators’ wavelengths needs. The 24-channel mux-demux design supports 20, 100GHz-wide channels for the 10-gigabit wavelengths and four wavelengths reserved for business services. Business services have become an important part of the cable operators’ revenues.

Infinera says the HDEA platform supports the extended C-band for a total of 96 wavelengths.

The company says it will develop different AWG configurations tailored for the wavelengths and channel count required for the different access applications.

In the rack, the HDEA aggregation platform takes up one shelf, while eight mux-demux units take up another 1RU. Space is left in between to house the cabling between the two.

The HDEA 1600G pulled out of the rack, showing the MPO connectors and the space to house the cabling between the HDEA and the rack of compact AWGs. Source: Infinera.

Baldry points out that the four business service wavelengths are not touched by the HDEA platform, Rather, these are routed to separate Ethernet switches dedicated to business customers. "We break those wavelengths out and hand them over to whatever system the operator is using," he says.

The HDEA 1600G also features eight 100-gigabit line-side interfaces that carry the aggregated cable access streams. Infinera is not revealing the supplier of the 1.6 terabit switch silicon - 800-gigabit for client-side capacity and 800-gigabit for line-side capacity - it is using for the HDEA platform.

The platform supports all the software Infinera uses for its EMXP, a packet-optical switch tailored for access and aggregation that is part of Infinera’s XTM family of products. Features include multi-chassis link aggregation group (MC-LAG), ring protection, all the Metro Ethernet Forum services, and synchronisation for mobile networks, says Baldry

Auto-Lambda

Infinera has developed what it calls its Auto-Lambda technology to simplify the wavelength management of the remote PHY devices.

Here, the optics set up the connection instead of a field engineer using a spreadsheet to determine which wavelength to use for a particular remote PHY. Tunable SFP+ modules can be used at the remote PHY devices only with fixed-wavelength (grey) SFP+ modules used by the HDEA platform to save on costs, or both ends can use tunable optics. Using tunable SFP+ modules at each end may be more expensive but the operator gains flexibility and sparing benefits.

Jon Baldry

Establishing a link when using fixed optics within the HDEA platform, the SFP+ is operated in a listening mode only. When a tunable SFP+ transceiver is plugged in at a remote PHY, which could be days later, it cycles through each wavelength. The blocking nature of the AWG means that such cycling does not disturb other wavelengths already in use.

Once the tunable SFP+ reaches the required wavelength, the transmitted signal is passed through the AWG to reach the listening transceiver at the switch. On receipt of the signal, the switch SFP+ turns on its transmitter and talks to the remote transceiver to establish the link.

For the four business wavelengths, both ends of the link use auto-tunable SFP+ modules, what is referred to a duel-ended solution. That is because both end-point systems may not be Infinera platforms and may have no knowledge as to how to manage WDM wavelengths, says Baldry.

In this more complex scenario, the time taken to establish a link is theoretically much longer. The remote end module has to cycle through all the wavelengths and if no connection is made, the near end transceiver changes its transmit wavelength and the remote end’s wavelength cycling is repeated.

Given that a sweep can take two minutes or more, an 80-wavelength system could take close to three hours in the worst case to establish the link; an unacceptable delay.

Infinera is not detailing how its duel-ended scheme works but a combination of scanning and communications is used between the two ends. Infinera had shown such a duel-ended scheme set up a link in 4 minutes and believes it can halve that time.

Finisar detailed its own Flextune fast-tuning technology at ECOC 2018. However, Infinera stresses its technology is different.

Infinera says it is talking to several pluggable optical module makers. “They are working on 25-gigabit optics which we are going to need for 5G,” says Baldry. “As soon as they come along, with the same firmware, we then have auto-tunable for 5G.”

System benefits

Infinera says its HDEA design delivers several benefits. Using the sides of the box means that the platform supports 80 SFP+ interfaces, twice the capacity of competing designs. In turn, using MPO connectors simplifies the fibre management, benefiting operational costs.

Infinera also believes that the platform’s overall power consumption has a competitive edge. Baldry says Infinera incorporates only the features and hardware needed. “We have deliberately not done a lot of stuff in Layer 2 to get better transport performance,” he says. The result is a more power-efficient and lower latency design. The lower latency is achieved using ‘thin buffers’ as part of the switch’s output-buffered queueing architecture, he says.

The platform supports open application programming interfaces (APIs) such that cable operators can make use of such open framework developments as the Cloud-Optimised Remote Datacentre (CORD) initiative being developed by the Open Networking Foundation. CORD uses open-source software-defined networking (SDN) technology such as ONOS and the OpenFlow protocol to control the box.

An operator can also choose to use Infinera’s Digital Network Administrator (DNA) management software, SDN controller, and orchestration software that it has gained following the Coriant acquisition.

The HDEA 1600G is generally available and in the hands of several customers.

Daryl Inniss reflects on a career in market research

Daryl Inniss

Daryl Inniss

Rocky beginnings

I jumped ship in 2001 joining RHK, a market research firm, knowing nothing about the craft. I had been a technical manager and loved research and development, but work was 500 miles from my family and the weekly commute was gruelling.

Back then, the telecom market was crashing and I believed my job was at risk. Moving to a small market research firm could hardly be described as good planning, but it turned out to be a godsend.

I had no idea what I was getting into and my first months did not help. My mother passed away within a month of joining and I was absent for half of my first 40 days. But my boss was very supportive. Meanwhile, work consisted of unintelligible, endless conference calls. And while in this daze, September 11th occurred.

The first report - getting the job done

Completing my first market research report helped ground me in the art. I wrote about optical dispersion compensators. After interviewing many companies, I wrote a long and complicated piece, an exercise that I found difficult. I also struggled with who would read the report and what would be done with the data.

The report aimed to explain technical issues simply and included a market forecast. Completing it proved hard because there was always more information to include, a better explanation, and better forecast data to be gathered.

I felt unsatisfied but the report received kudos. Internally I was told that I was the second or third analyst to tackle that topic and the first to complete the work. And an optical company complimented me on the report. But I felt dissatisfied and wished I had done better. I wanted to understand the subject more, wished I could provide clearer, simpler explanations and also provide a better forecast.

Nonetheless, I learned the importance of completing assignments as they can go on forever.

A market researcher's role

An analyst tries to identify market opportunities and winning strategies. Looking at new products, for example, the goal is to explain what they are, why they are being introduced, who will use them, their value, and the competitive landscape. The issues must be explained to novices and experts alike. The technical novice may get a glimpse of what the technology means and how it works, while a technical expert may understand the ecosystem more deeply.

An analyst must strive to prepare simple messages that are steeped in facts. You need to have a story—say why something is happening and explain it in the context of the bigger picture.

Forecasts, market share, rankings, prices and volumes are all important. Everyone loves numbers. But the story underpinning the numbers is far more important and most people do not take the time to determine the causes behind the numbers.

Where is the industry going?

I have spent the last 15 years analysing the optical components market. Sustainable profitability is the biggest topic, and consolidation is viewed as providing the best approach. Notwithstanding the mergers and acquisitions, the market is fragmented, margins remain low, and there is still no evidence of true consolidation.

Independent of all the change, optical component suppliers post gross margins below 40 percent and most are below 30 percent while semiconductor companies are routinely above 50 percent. There is a force keeping the industry stuck at this level, in part because there is little product differentiation.

Forecasts, market share, rankings, prices and volumes are all important. Everyone loves numbers. But the story underpinning the numbers is far more important

Avago Technologies’ divestiture of its optical module business to Foxxconn Interconnect Technology Group points to one high-margin path. Discrete components—particularly lasers and modulators, and to a lesser extent photodiodes and receivers - command higher margins. Vendors can offer differentiated products at this level. Total revenues are lower so the challenge is to win enough business to fill the factory because these are fixed-cost, intensive businesses.

Subsystems offer another high-margin path, particularly for vertically-integrated companies. Here vendors are challenged with a long time-to-market, requiring a strong design team to support customer requests. Also business can be lumpy because solutions are customer-specific.

Acacia Communications' coherent 100 gigabit transponders is an example solution that has the basis to win broad-based business and high margins. The products offer a one-stop-shop solution including optics, electronics, and software. Acacia is developing silicon photonics so it controls most of the bill of materials, keeping down product cost. And its solution is differentiated in that it helps customers get their products to market while achieving a high level of performance.

Market research: even more important now

The communications industry is going through extensive change making market research more important than ever. The Web 2.0 companies are the new optical communication mindshare leaders, driving technology and business practices.

Simultaneously China is the biggest consumer of optical gear, both for long-haul and access networks. Optical component suppliers need to understand how to compete in this new environment. What are the new rules? How are they evolving? How can companies best position themselves to win more business?

Just like when I started, I ask how can a market researcher help component companies navigate this new world. No doubt, this is a challenge, but market researchers provide the collective market voice. They are the market mirror that shows the beauty spots and the warts. They are given license to say what everyone is thinking. They can raise market consciousness so participants may act fearlessly.

But market researchers need to understand the story from top to bottom—end customer to suppliers. They must communicate well which includes not only delivering the story but also being humble, admitting mistakes, keeping sources and information confidential, and taking corrective actions.

This is indeed a challenge and I feel honoured to have had the opportunity to participate. I could not have done the job without the help of wonderful people from all over the world. Their generosity, warmth, and kindness made all the difference. At bottom, it is these relationships that mattered as we tried to help each other navigate.

Biography

Dr. Daryl Inniss is Director, New Business Development at OFS Fitel, the designer, manufacturer and provider of optical fibre, fibre optic cable, connectivity, fibre-to-the-subscriber and specialty photonics products.

He was formerly Components Practice Leader at market research firm Ovum and RHK. Daryl was Technical Manager at JDSU and Lucent Technologies, Bell Laboratories, and started his career as a Member of the Technical Staff, AT&T Bell Labs.

Global optical networking market set for solid growth

Source: Ovum

Source: Ovum

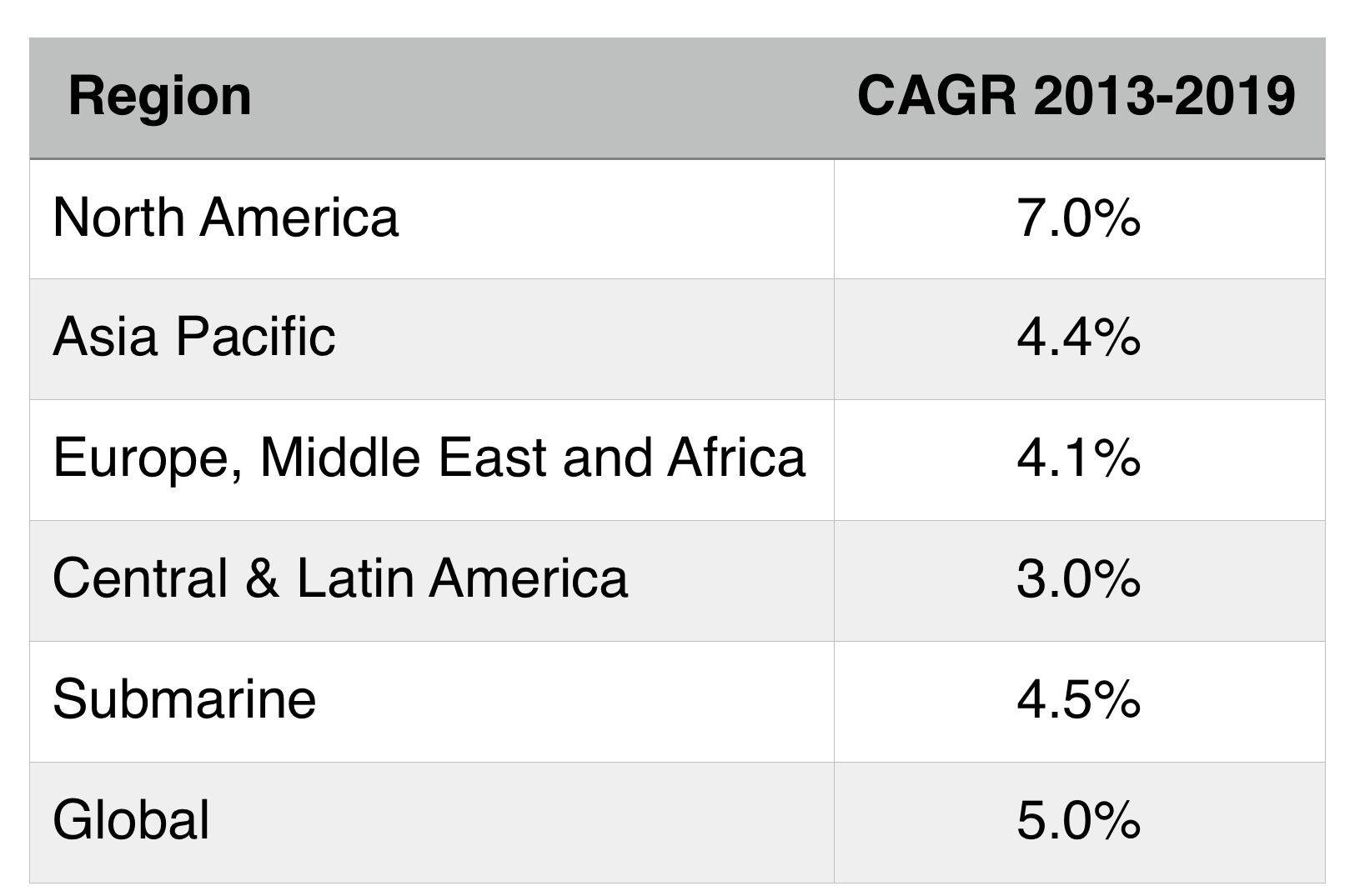

The global optical networking market will grow at a year-over-year rate of 5 percent through 2019. So claims market research firm, Ovum, in its optical networking forecast for 2013 to 2019. North America will lead the market growth, with data centre deployments and demand for 100 Gigabit being the main drivers.

The building of data centres drives demand for optical interconnect. "It [data centre operators] is almost a new category of buyer," says Ian Redpath, principal analyst, network infrastructure at Ovum. The segment is growing faster than telco spending on fixed and mobile networks.

"This whole phenomenon of the large data centre operators is more pronounced in North America, and we think that will continue throughout the forecast period," says Redpath.

Demand for 100 Gigabit is coming from several segments: large incumbent operators, cable operators and internet content service providers. "All these entities are buying a technology [100 Gig] that is prime time," says Redpath.

Asia Pacific will be the region with the second largest growth for the forecast period, at 4.4 percent compound annual growth rate (CAGR).

The deployment of optical equipment in China and Japan was down in 2013: China dipped 6 percent while Japan was down a huge 23 percent compared to 2012 market demand.

The underlying trend in China is one of growth, with the optical market valued at US $3 billion. "They just had to have a pause," says Redpath, who points out that the Chinese market has tripled in a relatively short period. "They are now retooling for the next big thing: LTE; it it just a matter of time," he says. The deployment of 100 Gig, by the large three domestic operators, may start by the year end or spill into 2015.

Optics is the foundation of an industry that is growing

Japan's sharp decline in 2013 follows massive growth in 2012, the result of replacing networks lost following the 2011 earthquake and tsunami. "That was a one-time bump followed by a one-time reset, with the market now back to normal," says Redpath.

Meanwhile, the EMEA optical networking market will growth at 4.1 percent. "This is a pretty modest growth rate, with more upside coming in the latter period," says Redpath. "The operators have been neglecting their core for so long, they are going to have to come back and reinvest."

Ovum says the weakness of the European market will run its course during the forecast period and expects Europe's northern countries - the UK and Germany - to lead the recovery, followed by the likes of Spain, Italy and Greece.

The market research firm singles out the UK market as being particularly dynamic, and an economy that will lead Europe out of recession. "It is probably closer to the North America market than any other country in terms of competitors and non-carrier spending," says Redpath. "The UK is also one of the leading data centre markets in the world."

Ovum remains upbeat about the long-term prospects of the global optical networking market. "Optics is the foundation of an industry that is growing," says Redpath.

He also points to recent developments in the net neutrality debate, and cites how over-the-top TV and film player, Netflix, has signed agreements with telecom and cable operators. "If over-the-top players realise that they can't keep free-riding on these networks, and to get performance they give a little money to the telcos, then that is a good thing for the ultimate food chain," says Redpath.

Further reading:

Global market soft in 1Q14; North America bucks trend, click here

OFC 2014 industry reflections - Part 2

The high cost of 100 Gigabit Ethernet client modules has been a major disappointment to me as it has slowed adoption

Joe Berthold, Ciena

Joe Berthold, vice president of network architecture at Ciena.

OFC 2014 was another great event, with interesting programmes, demonstrations and papers presented. A few topics that really grabbed my interest were discussions around silicon photonics, software-defined networking (SDN) and 400 Gigabit Ethernet (GbE).

The intense interest we saw at last year’s OFC around silicon photonics grew this year with lots of good papers and standing-room-only sessions. I look forward to future product announcements that deliver on the potential of this technology to significantly reduce cost of interconnecting systems over modest distances. The high cost of 100GbE client modules has been a major disappointment to me as it has slowed adoption.

Another area of interest at this year’s show was the great deal of experimental work around SDN, some more practical than others.

I particularly liked the reviews of the latest work under the DARPA-sponsored CORONET programme, whose Phase 3 focused on SDN control of multi-layer, multi-vendor, multi-data centre cloud networking across wide area networks.

In particular, there were talks from three companies I noted: Anne Von Lehman of Applied Communication Sciences, the prime contractor, provided a good program overview; Bob Doverspike of AT&T described a very extensive testbed using equipment of the type currently deployed in AT&T’s network, as well as two different processing and storage virtualisation platforms; and Doug Freimuth of IBM described its contributions to CORONET including an OpenStack virtualisation environment, as well as other IBM distributed cloud networking research.

All the action on rates above 100 Gig lies with the selection of client signals. 400 Gig seems to have the major mindshare but there are still calls for flexible rate clients and Terabit clients.

One thing I enjoyed about these talks was that they described an approach to SDN for distributed data centre networking that is pragmatic and could be realised soon.

I also really liked a workshop held on the Sunday on the question whether SDN will kill GMPLS. While there was broad consensus that GMPLS has failed in delivering on its original turn-of-the-century vision of IP routers control of multi-layer, multi-domain networks, most speakers recognised the value distributed control planes have in simplifying and speeding the control of single layer, single domain networks.

What I took away was that single layer distributed control planes are here to stay as important network control functions, but instead will work under the direction of an SDN network controller.

As we all know, 400 Gigabit dense wavelength division multiplexing (DWDM) is here from the technology perspective, but awaiting standardisation of the 400 Gig Ethernet signal from the IEEE, and follow-on work by the ITU-T on signal mapping to OTN. In fact, from the perspective of DWDM transmission systems, 1 Terabit-per-second systems can be had for the asking.

All the action on rates above 100 Gig lies with the selection of client signals. 400 Gig seems to have the major mindshare but there are still calls for flexible rate clients and Terabit clients.

One area that received a lot of attention, with many differing points of view, was the question of the 400GbE client. As the 400GbE project begins soon in the IEEE, it is time to take a lesson from the history of the 100 Gig client modules and do better.

Let us all agree that we don’t need 400 Gig clients until they can do better in cost, face plate density, and power dissipation than the best 100 Gig modules that will exist then.

The first 100 Gig DWDM transceivers were introduced in 2009. It is now 2014 and 100 Gig is the transmission rate of choice for virtually all high capacity DWDM network applications, with a strong economic value proposition versus 10 Gig. Yet the industry has not yet managed to achieve cost/bit parity between 100 Gig and 10 Gig clients - far from it!

Last year's OFC, we saw many show floor demonstrations of CFP2 modules. They promise lower costs, but evidence of their presence in shipping products is still lacking. At the exhibit this year we saw 100 Gig QSFP28 modules. While progress is slow, the cost of the 100 Gig client module continues to result in many operators favouring 10 Gig handoffs to their 100 Gig optical networking systems.

Let us all agree that we don’t need 400 Gig clients until they can do better in cost, face plate density, and power dissipation than the best 100 Gig modules that will exist then. At this juncture the 100 Gig benchmark we should be comparing 400 Gig to is a QSFP28 package.

Lastly, last year we heard about the launch of an OIF project to create a pluggable analogue coherent optical module. There were several talks that referenced this project, and discussed its implications for shrinking size and supporting higher transceiver card density.

Broad adoption of this component will help drive down costs of coherent transceivers, so I look forward to its hearing about its progress at OFC 2015.

Daryl Inniss, vice president and practice leader, Ovum.

There was no shortage of client-side announcements at OFC and I’ve spent time since the conference trying to organise them and understand what it all means.

I’m tempted to say that the market is once again developing too many options and not quickly agreeing on a common solution. But I’m reminded that this market works collaboratively and the client-side uncertainty we’re seeing today is a reflection of a lack of market clarity.

Let me describe three forces affecting suppliers:

The IEEE 100GBASE-xxx standards represent the best collective information that suppliers have. Not surprisingly, most vendors brought solutions to OFC supporting these standards. Vendors sharpened their products and focused on delivering solutions with smaller form factors and lower power consumption. Advances in optical components (lasers, TOSAs and ROSAs), integrated circuits (CDRs, TIAs, drivers), transceivers, active optical cables, and optical engines were all presented. A promising and robust supply base is emerging that should serve the market well.

A second driver is that hyperscale service providers want a cost-effective solution today that supports 500m to 2km. This is non-standard and suppliers have not agreed on the best approach. This is where the market becomes fragmented. The same vendors supporting the IEEE standard are also pushing non-standard solutions. There are at least four different approaches to support the hyperscale request:

- Parallel single mode (PSM4) where an MSA was established in January 2014

- Coarse wavelength division multiplexing—using uncooled directly modulated lasers and single mode fibre

- Dense wavelength division multiplexing—this one just emerged on the scene at OFC with Ranovus and Mellanox introducing the OpenOptics MSA

- Complex modulation—PAM-8 for example and carrier multi-tone.

Admittedly, the presence of this demand disrupts the traditional process. But I believe the suppliers’ behavior reflects their unhappiness with the standardisation solution.

The good news is these approaches are using established form factors like the QSFP. And silicon photonic products are starting to emerge. Suppliers will continue to innovate.

Ambiguity will persist but we believe that clarity will ultimately prevail.

The third issue lurking in the background is knowledge that 400 Gig and one Terabit will soon be needed. The best-case scenario is to use 100 Gig as a platform to support the next generation. Some argue for complex modulation as you reduce the number of optical components thereby lowering cost. That’s good but part of the price is higher power consumption, an issue that is to be determined.

Part of today’s uncertainty is whether the standard solution is suitable to support the market to the next generation. Sixteen channels at 25 Gig is doable but feels more like a stopgap measure than a long-term solution.

These forces leave suppliers innovating in search of the best path forward. The approaches and solutions differ for each vendor. Timing is an issue too with hyperscale looking for solutions today while the mass market may be years away.

We believe that servers with 25 Gig and/ or 40 Gig ports will be one of the catalysts to drive the mass market and this will not start until about 2016. Meanwhile, each vendor and the market will battle for the apparent best solution to meet the varying demands. Ambiguity will persist but we believe that clarity will ultimately prevail.

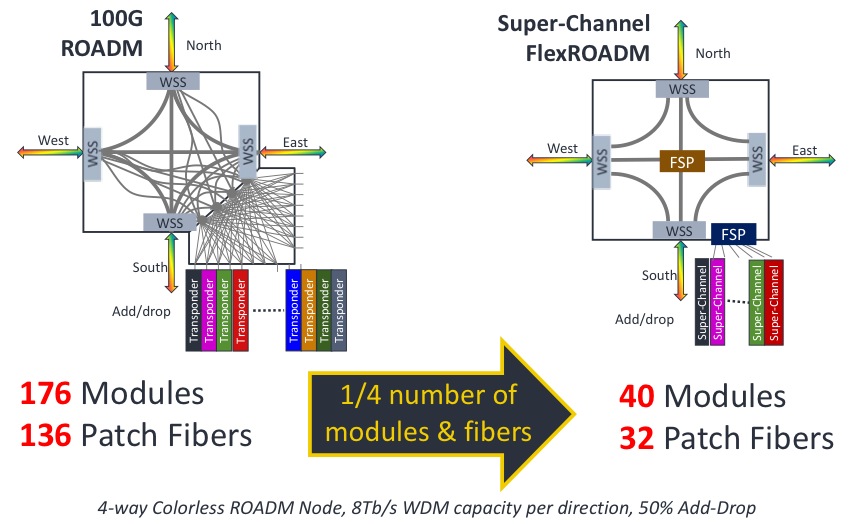

Infinera introduces flexible grid 500G super-channel ROADM

An example showing the impact of a 500G super-channel ROADM node. Source: Infinera

An example showing the impact of a 500G super-channel ROADM node. Source: Infinera

"The FlexROADM will open up the Tier-1 operators in a way Infinera has not been able to do before," says Dana Cooperson, vice president, network infrastructure at market research firm, Ovum. "The DTN-X was necessary but not sufficient; the ROADM is the last piece."

The FlexROADM is claimed to deliver two industry firsts: it can add and drop flexible-grid-based 500 Gig super-channels, and uses the Internet Engineering Task Force’s (IETF) spectrum switched optical networks (SSON).

"SSON is the next generation of WSON [Wavelength Switched Optical Network control plane], except it manages spectrum," says Ron Kline, principal analyst, network infrastructure also at Ovum.

The DTN-X platform combines Infinera's 500 Gig photonic integrated circuits and OTN (Optical Transport Network) switching. With the FlexROADM, Infinera has added switching at the optical layer in 500 Gig increments. Infinera can now offer enhanced multi-layer network optimisation with the combination of electrical and optical switching.

"Optical bypass before was manual using patch cords, now operators can reconfigure with the FlexROADM," says Kline. "It also provides new optical restoration capabilities that Infinera did not have."

The FlexROADM supports up to nine degrees, and is available in colourless, colourless and directionless, and full colourless, directionless and contentionless (CDC) versions.

"The debate about contentionless continues," says Kline. "It is safe to assume that for the majority of applications flexible grid, colourless and directionless will be the high runner." Contentionless will be used by the big carriers, he says, but in certain locations only.

Infinera says the line system announced will support up to 24 Terabit-per-second (Tbps) when it ships in September. The maximum long-haul capacity using its current PM-QPSK super-channels is 9.5Tbps per fibre pair.

"In the future when we enable metro-reach super-channels using PM-16-QAM, they will support 24 Terabit-per-second per fibre pair using the line system we are announcing," says Geoff Bennett, director, solutions and technology at Infinera.

Bennett says the data rate and the spectral efficiency for a given sub-carrier can be varied depending on the reach required. The spacing between sub-carriers that make up a super-channel also can be varied depending on reach. Many different transmission possibilities exist, says Bennett, but to explain the concept, he cites two examples.

The 24Tbps capacity with PM-16-QAM modulation uses pulse shaping at the transmitter to achieve 'Nyquist DWDM' channel spacing, the spacing between channels that approximates the baud rate, says Bennett.

"At this time we are not disclosing the details of the channel spacing, or the number of sub-carriers used by our future line modules," says Bennett. "But the total super-channel spectral width is the equivalent of 200GHz if you are transmitting a one Terabit super-channel, for example." This equates to a spectral efficiency of 5b/s/Hz, and using 16-QAM, the reach achieved will be 600-700km.

"The system we have just launched is designed to operate in long-haul networks and uses PM-QPSK," says Bennett. "For an ultra long-haul reach requirement of 4,500km, the super-channel comprises ten sub-carriers; a total of 500 Gbps over a spectral width of 250 GHz." These line cards are available now, he says.

Infinera continues to make steady market progress, according to Ovum. The company is in the top 10 system vendors globally, while in backbone and 100 Gigabit, Infinera is fourth.

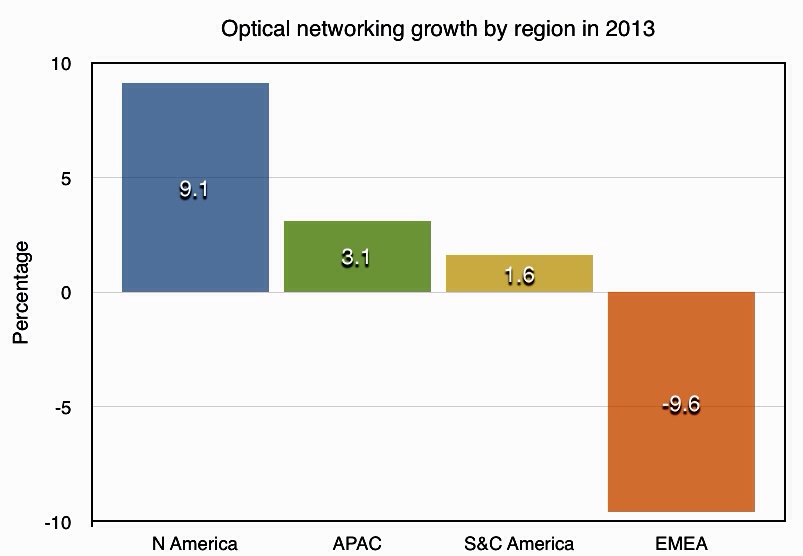

Optical networking spending up in all regions except Europe

Source data: Ovum

Source data: Ovum

Ovum forecasts that the global optical networking market will grow to US $17.5 billion by 2018, a compound annual growth rate of 3.1 percent.

Optical networking spending in North America will be up 9.1 percent in 2013 after two flat years. North American tier-1 service providers and cable operators are investing in the core network to support all traffic types, and 100 Gigabit is being deployed in volume.

In contrast, optical networking sales in EMEA will contract by nearly 10 percent in 2013. “Non-spending in Europe is the major factor in the overall EMEA decline,” says Ian Redpath, principal analyst, network infrastructure at Ovum.

The major technology trend for this forecast is the ascendancy of 100 Gig, whose sales exceeded 40 Gig revenues in 2Q13

EMEA optical networking spending has been down in four out of the past five years, and the lack of investment is becoming acute, says Ovum. Given that service providers are stretching their existing networks, spending will have to take place eventually to make up for the prolonged period of inactivity.

This year has seen 100 Gigabit become the wavelength of choice for large WDM systems, with sales surging. Spending on 100 Gigabit has now overtaken spending on 40 Gigabit which declined in the first half of the year.

"The major technology trend for this forecast is the ascendancy of 100 Gig, whose sales exceeded 40 Gig revenues in 2Q13," says Redpath.

Further reading:

Ovum: Optical networks forecast: top line steady, 100G surging, click here

Ovum on Infinera's Intelligent Transport Network strategy

Infinera announced that TeliaSonera International Carrier (TSIC) is extending the use of its DTN-X to its European network, having already adopted the platform in the US. Infinera has also outlined the next evolution in its networking strategy, dubbed the Intelligent Transport Network.

Dana Cooperson

Dana Cooperson

Gazettabyte asked Dana Cooperson, vice president and practice leader, and Ron Kline, principal analyst, both in the network infrastructure group at market research firm, Ovum, about the announcement and Infinera's outlined strategy.

What has been announced

TSIC is adding Infinera's DTN-X to boost network capacity in Europe and accommodate its own growing IP traffic. TSIC already has deployed 100 Gig technology in its European network, using a Coriant product. The wholesale operator will sell 100 Gig services, activating capacity using the DTN-X's 'instant bandwidth' feature based on already-lit 100 Gig light paths that make up its 500 Gigabit super-channels.

Meanwhile, Infinera has detailed its Intelligent Transport Network strategy that extends its digital optical network that performs optical-electrical-optical (OEO) conversion using its 500 Gig photonic integrated circuits (PICs) coupled with OTN (Optical Transport Network) switching to include additional features. These include multi-layer switching – reconfigurable optical add/drop multiplexers (ROADMs) and MPLS (Multi-Protocol Label Switching) – and PICs with terabit capacity

Q&A with Dana Cooperson and Ron Kline

Q. What is significant about Infinera's Intelligent Transport Network strategy?

Dana C: Infinera is being more public about its longer-term strategy - to 2020 - which includes evolving from its digital optical network messaging to a network that includes multiple layers and types of switching, and more automation. Infinera is not announcing more functionality availability now.

Infinera makes much play about its 500 Gig super-channels. More recently it has detailed such platform features as instant bandwidth and Fast Shared Mesh Protection supported in hardware. Are these features giving operators something new and is Infinera gaining market share as a result?

Dana C: Instant Bandwidth provides a way for Infinera’s operator customers to have their cake and eat it. They can install 500 Gig super-channels ahead of demand, and not pay for each 100 Gig sub-channel until they have a need for that bandwidth. It is a simple process at that point to 'turn on' the next 100 Gig worth of bandwidth within the super-channel.

By installing all five 100 Gig channels at once, the operator can simplify operations - lower opex - and allow quicker time-to-revenue without having to take the capex hit until the bandwidth needs materialise. This is an improvement over the DTN platform, which gave customers the 10x10 Gig architecture to let them pre-position bandwidth before the need for it materialised and save on opex, but at the cost of higher up-front capex than was ideal.

Talking to TSIC confirm that this added flexibility the DTN-X provides has allowed them to win wholesale business from competitors while tying capex more directly to revenue.

Ron K: Although pay-as-you go capability is available, analysis of 100 Gig shipments to date indicate most customers are paying for all five up front.

Dana C: I have not directly talked with an Infinera customer that has confirmed the benefit of Fast Shared Mesh Protection, but the feature certainly seems to be of value to customers and prospects. Our research indicates the continued search for better, more efficient mesh protection. Hardware-enabled protection should provide better latency (higher speed).

Ron K: Resiliency and mesh protection are critical requirements if you want to participate in the market. Shared mesh assumes that you have idle protection capacity available in case there is a failure. That is expensive. However, with Infinera’s technology - the PIC and Instant Bandwidth - it is not as difficult.

Restoration is all about speed – how fast can you get the network back up. It is not always milliseconds, sometimes it is half a minute. But during catastrophic failure events such as an earthquake, where a user can loose entire nodes, 30 seconds may not be so bad. Infinera has implemented the switch in hardware, based on a pre-planned map, so it is quicker.

Dana C: As for what impact these capabilities are having on market share, Infinera has climbed to the No.3 player in 100 Gig DWDM in three quarters since the DTN-X has become available.

They’ve jumped back up to No.4 globally in backbone WDM/CPO-T (converged packet optical transport) after sinking to sixth when they were losing share because they were without a viable 40 Gig solution. They made the right call at that time to focus on 100 Gig systems based on the 500 Gig PIC rather than chase 40 Gig. They are both keeping and expanding with existing DTN customers, TSIC being one, and picking up new customers.

Ron Kline

Ron Kline

Ron K:They are definitely picking up share. However, I’m not sure if they can sustain it. The reason for the share jump is they are selling 100 Gig, five at a time. Remember, most customers elect to pay for all five. That means future sales will lag because customers have pre-positioned the bandwidth.

Looking at the customers is probably a better indicator: Infinera has some 27 customers, maybe 30 by now, which provide a good embedded base. Still, 27 customers is low compared to Ciena, Alcatel-Lucent, Huawei and even Cisco.

When Infinera first announced the DTN-X in 2011 it talked about how it would add MPLS support. Now outlining its Intelligent Transport Network strategy it has still to announce MPLS support. Do operators not need this network feature yet in such platforms and if not, why?

Dana C: The market is still sorting out exactly what is needed for sub-wavelength switching and where it is needed. Cisco’s and Juniper’s approaches are very different in the routing world —essentially, a lower-cost MPLS blade for the CRS versus a whole new box in the PTX; there is no right way there.

Within packet-aware optical products, the same is true: What is the right level of integration of OTN versus MPLS? It depends on where you are in the network, what that carrier’s service mix is, and how fast the mix is changing.

Many carriers are still struggling with their rigid organisational structures, and how best to manage products that are optical and packet in equal measure. So I don’t think Infinera is late, they are just reacting to their customers’ priorities and doing other things first.

Ron K: This is the $64,000 question: MPLS versus OTN. I’m not sure how it will eventually play out. I am asking service providers now.

OTN is a carrier protocol developed for carriers by carriers (the replacement for SONET/SDH). They will be the ones to use it because they have multi-service networks and need the transparency OTN provides. Google types and cable operators will not use OTN switching - they will lean towards the label-switched path (LSP) route. Even Tier-1 operators who have both types of networks will most likely maintain separation.

"The trick is to optimise around the requirements that net you the biggest total available market and which maximise your strengths and minimise your weaknesses. You can’t be all things to all carriers."

If Infinera has its digital optical network, why is it now also talking about ROADMs? And does having both benefit operators?

Dana C: Yes, having both benefits operators. From discussions with Infinera's customers, it is true that the digital nodes give them flexibility, but they do introduce added cost. For those nodes where customers have little need to add/ drop traffic, a ROADM would provide a more cost-efficient option to a node that performs OEO for all the traffic. So, with a ROADM option customers would have more control over node design.

Infinera talks about its next-gen PICs that will support a Terabit and more. After nearly a decade of making PICs, how does Ovum view the significance of the technology?

Dana C: While more vendors are doing photonic integration R&D, and some - Huawei comes to mind - have released some PIC-based products, no one has come close to Infinera in what it can do with photonic integration. Speaking with quite a few of Infinera’s customers, they are very happy with the technology, the system, and the support.

Each generation of PIC requires a significant R&D effort, but it does provide differentiation. Infinera has managed to stay focused and implement on time and on spec. I see them as the epitome of a “specialist” vendor. They are of similar size to Coriant and Tellabs, which have seen their fortunes wane, and ADVA Optical Networking. So I would say they are a very good example of what focus and differentiation can do.

Now, is the PIC the only way to approach system architecture? No. As noted before, some Infinera clients have told me that the lack of a ROADM has hurt them in competitive situations, as did the need to pay for all the pre-positioned bandwidth up front (true for the DTN, not the DTN-X).

From my days in product development, I know you have to optimise around a set of requirements, and the trick is to optimise around the requirements that net you the biggest total available market and which maximise your strengths and minimise your weaknesses. You can’t be all things to all carriers.

What is significant about the latest TeliaSonera network win and what does it mean for Coriant?

Dana C: Infinera is announcing an extension of its deployments at TSIC from North America to now include Europe as well. When you ask what this means to Coriant, their incumbent supplier in Europe, the answer is not clear cut. This gives Infinera an expanded hunting licence and it gives Coriant some cause for worry.

TSIC values both vendors and both will have their place in the European network. TSIC plans to use the vendors in different regions.

I am sure TSIC will try and play each off against the other to get the best price. It is looking for more flexibility and some healthy competition.

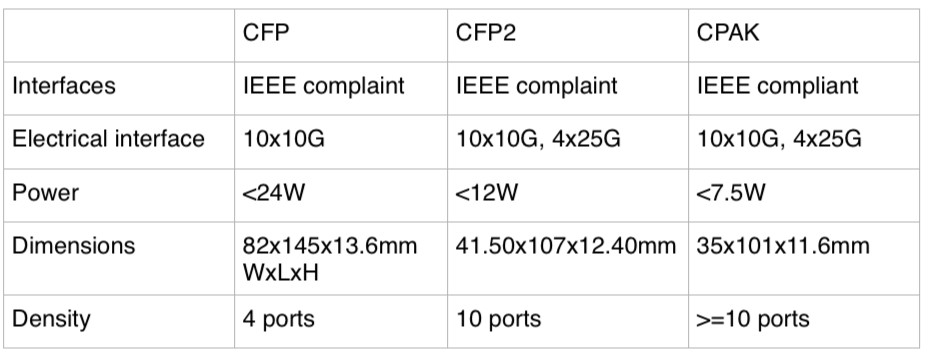

Does Cisco Systems' CPAK module threaten the CFP2?

Cisco Systems has been detailing over recent months its upcoming proprietary optical module dubbed CPAK. The development promises to reduce the market opportunity for the CFP2 multi-source agreement (MSA) and has caused some disquiet in the industry.

Source: Cisco Systems, Gazettabyte, see comments

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people," says Paul Brooks, director for JDSU's high speed transport test portfolio.

Brooks speculates that the advent of CPAK may even cause some module makers to skip the CFP2 and go straight to the smaller CFP4 given the time lag between the two MSAs is relatively short.

The CPAK module, smaller than the CFP2 MSA and three quarters its volume, has not been officially released and Cisco will not comment on the design but in certain company presentations the CPAK is compared with the CFP. The details are shown in the table above, with the CFP2’s details added.

The CPAK is the first example of Cisco's module design capability following its acquisition of silicon photonics player, Lightwire.

The development of the module highlights how the acquisition of core technology can give an equipment maker the ability to develop proprietary interfaces that promise costs savings and differentiation. But it also raises a question mark regarding the CFP2 and the merit of MSAs when a potential leading customer of the CFP2 chooses to use its own design.

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

Paul Brooks, JDSU

Industry analysts do not believe it undermines the CFP2 MSA. “I believe there is business for the CFP2,” says Daryl Inniss, practice leader, Ovum Components. “Cisco is shooting for a solution that has some staying power. The CFP2 is too large and the power consumption too high while the CFP4 is too small and will take too long to get to market; CPAK is a great compromise.”

That said, Inniss, in a recent opinion piece entitled: Optical integration challenges component/OEM ecosystem, writes:

“Cisco’s Lightwire acquisition provides another potential attack on the traditional ecosystem. Lightwire provides unique silicon photonics based technology that can support low power consumption and high-density modules. Cisco may adopt a proprietary transceiver strategy to lower cost, decrease time to market, and build competitive barriers. It need not go through the standards process, which would enable its competitors and provide them with its technology. Cisco only needs to convince its customers that it has a robust supply chain and that it can support its product.”

Vladimir Kozlov, CEO of market research firm, LightCounting, is not surprised by the development. “Cisco could use more proprietary parts and technologies to compete with Huawei over the next decade,” he says. “From a transceiver vendor perspective, custom-made products are often more profitable than standard ones; unless Cisco will make everything in house, which is unlikely, it is not bad news.”

JDSU has just announced that its ONT-100G test set supports the CFP2 and CFP4. The equipment will also support CPAK. "We have designed a range of adaptors that allows us to interface to other optics including one very large equipment vendor's - Cisco's - own CFP2-like form factor," says Brooks.

However, Brooks still expects the industry to align on a small number of MSAs despite the advent of CPAK. "The majority view is that the CFP2 and CFP4 will address most people's needs," says Brooks. "Although there is some debate whether a QSFP2 may be more cost effective than the CFP4." The QSFP2 is the next-generation compact follow-on to the QSFP that supports the 4x25Gbps electrical interface.

Optical industry restructuring: The analysts' view

The view that the optical industry is due a shake-up has been aired periodically over the last decade. Yet the industry's structure has remained intact. Now, with the depressed state of the telecom industry, the spectre of impending restructuring is again being raised.

In Part 2, Gazettabyte asked several market research analysts - Heavy Reading's Sterling Perrin, Ovum's Daryl Inniss and Dell'Oro's Jimmy Yu - for their views.

Part II: The analysts' view

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen"

Sterling Perrin, Heavy Reading

Larry Schwerin, CEO of ROADM subsystem player Capella Intelligent Subsystems, believes optical industry restructuring is inevitable. Optical networking analysts largely agree with Schwerin's analysis. Where they differ is that the analysts say change is already evident and that restructuring will be gradual.

"The industry has not been in good shape for many years," says Sterling Perrin, senior analyst at Heavy Reading. "The operators are the ones with the power [in the supply chain] and they seem to be doing decently but it is not a good situation for the systems players and especially for the component vendors."

Daryl Inniss, practice leader for components at Ovum, highlights the changes taking place at the optical component layer. "There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader," says Inniss.

A typical rule of thumb for an industry in that you need the top three [firms] to own between two thirds and 80 percent of the market, says Inniss: "These are real market leaders that drive the industry; everyone else is a specialist with a niche focus."

But the absence of such dominant players should not be equated with a lack of change or that component companies don't recognise the need to adapt.

"Finisar looks more like an industry leader than we have had before, and its behaviour is that of market leader," says Inniss. Finisar is building an integrated company to become a one-stop-shop supplier, he says, as is the newly merged Oclaro-Opnext which is taking similar steps to be a vertically integrated company. Finisar acquired Israeli optical amplifier specialist RED-C Optical Networks in July 2012.

Capella's Schwerin also wonders about the long term prospects of some of the smaller system vendors. Chinese vendors Huawei and ZTE now account for 30 percent of the market, while Alcatel-Lucent is the only other major vendor with double-digit share.

The rest of the market is split among numerous optical vendors. "If you think about that, if you have 5 percent or less [optical networking] market share, that really is not a sustainable business given the [companies'] overhead expenses," says Schwerin.

However Jimmy Yu, vice president of optical transport research at Dell’Oro Group, believes there is a role for generalist and specialist systems suppliers, and that market share is not the only indicator of a company's economic health. “You have a few vendors that are healthy and have a good share of the market,” he says. “That said, when I look at some of these [smaller] vendors, I say they are better off.”

Yu cites the likes of ADVA Optical Networking and Transmode, both small players with less than 3 percent market share but they are some of the most profitable system companies with gross margins typically above 40 percent. “Do I think they are going to be around? Yes. They are both healthy and investing as needed.”

Innovation

Equipment makers are also acquiring specialist component players. Cisco Systems acquired coherent receiver specialist CoreOptics in 2010 and more recently silicon photonics player, Lightwire. Meanwhile Huawei acquired photonic integration specialist, CIP Technologies in January 2012. "This is to acquire strategic technologies, not for revenues but to differentiate and reduce the cost of their products," says Perrin.

"There is a problem with the rate of innovation coming from the component vendors," adds Inniss. This is not a failing of the component vendors as innovation has to come from the system vendors: a device will only be embraced by equipment vendors if it is needed and available in time.

Inniss also highlights the changing nature of the market where optical networking and the carriers are just one part. This includes enterprises, cloud computing and the growing importance of content service providers such as Google, Facebook and Amazon who buy components and gear. "It is a much bigger picture than just looking at optical networking," says Inniss.

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

Daryl Inniss, Ovum

Huawei is one system vendor targeting these broader markets, from components to switches, from consumer to the data centre core. Huawei has transformed itself from a follower to a leader in certain areas, while fellow Chinese vendor ZTE is also getting stronger and gaining market share.

Moreover, a consequence of these leading system vendors is that it will fuel the emergence of Chinese optical component players. At present the Chinese optical component players are followers but Inniss expects this to change over the next 3-5 years, as it has at the system level.

Perrin also notes Huawei's huge emphasis on the enterprise and IT markets but highlights several challenges.

The content service providers may be a market but it is not as big an opportunity as traditional telecom. "It is also tricky for the systems providers to navigate as you really can't build all your product line to fit Google's specs and still expect to sell to a BT or an AT&T," says Perrin. That said, systems companies have to go after every opportunity they can because telecom has slowed globally so significantly, he says.

Inniss expects the big optical component players to start to distance themselves, although this does not mean their figures will improve significantly.

"This market is what it is - they [component players] will continue to have 35 percent gross margins and that is the ceiling," says Inniss. But if players want to improve their margins, they will have to invest and grow their presence in markets outside of telecom.

"I like the idea of a Cisco or a Huawei acquiring technology to use internally as a way to differentiate and innovate, and we are going to see more of that," says Perrin.

Thus the supply chain is changing, say the analysts, albeit in a gradual way; not the radical change that Capella's Schwerin suggests is coming.

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen," says Perrin. "I just don't see why there is some catalyst that suggests it is going to be different to the past two years."

This is based on an article that appears in the Optical Connections magazine for ECOC 2012

Ciena: Changing bandwidth on the fly

Ciena has announced its latest coherent chipset that will be the foundation for its future optical transmission offerings. The chipset, dubbed WaveLogic 3, will extend the performance of its 100 Gigabit links while introducing transmission flexibility that will trade capacity with reach.

Feature: Beyond 100 Gigabit - Part 1

"We are going to be deployed, [with WaveLogic 3] running live traffic in many customers’ networks by the end of the year"

"We are going to be deployed, [with WaveLogic 3] running live traffic in many customers’ networks by the end of the year"

Michael Adams, Ciena

"This is changing bandwidth modulation on the fly," says Ron Kline, principal analyst, network infrastructure group at market research firm, Ovum. “The capability will allow users to dynamically optimise wavelengths to match application performance requirements.”

WaveLogic 3 is Ciena's third-generation coherent chipset that introduces several firsts for the company.

- The chipset supports single-carrier 100 Gigabit-per-second (Gbps) transmission in a 50GHz channel.

- The chipset includes a transmit digital signal processor (DSP) - which can adapt the modulation schemes as well as shape the pulses to increase spectral efficiency. The coherent transmitter DSP is the first announced in the industry.

- WaveLogic 3's second chip, the coherent receiver DSP, also includes soft-decision forward error correction (SD-FEC). SD-FEC is important for high-capacity metro and regional, not just long-haul and trans-Pacific routes, says Ciena.

The two-ASIC chipset is implemented using a 32nm CMOS process. According to Ciena, the receiver DSP chip, which compensates for channel impairments, measures 18 mm sq. and is capable of 75 Tera-operations a second.

Ciena says the chipset supports three modulation formats: dual-polarisation bipolar phase-shift keying (DP-BPSK), quadrature phase-shift keying (DP-QPSK) and 16-QAM (quadrature amplitude modulation). Using a single carrier, these equate to 50Gbps, 100Gbps and 200Gbps data rates. Going to 16-QAM may increase the data rate to 200Gbps but it comes at a cost: a loss in spectral efficiency and in reach.

"This software programmability is critical for today's dynamic, cloud-centric networks," says Michael Adams, Ciena’s vice president of product & technology marketing.

WaveLogic 3 has also been designed to scale to 400Gbps. "This is the first programmable coherent technology scalable to 400 Gig," says Adams. "For 400 Gig, we would be using a dual-carrier, dual-polarisation 16-QAM that would use multiple [WaveLogic 3] chipsets."

Performance

Ciena stresses that this is a technology not a product announcement. But it is willing to detail that in a terrestrial network, a single carrier 100Gbps link using WaveLogic 3 can achieve a reach of 2,500+ km. "These refer to a full-fill [wavelengths in the C-Band] and average fibre," says Adams. "This is not a hero test with one wavelength and special [low-loss] fibre.”

Metro to trans-Pacific: The different reaches and distances over terrestrial and submarine using Ciena's WaveLogic 3. SC stands for single carrier. Source: Ciena/ Gazettabyte

Metro to trans-Pacific: The different reaches and distances over terrestrial and submarine using Ciena's WaveLogic 3. SC stands for single carrier. Source: Ciena/ Gazettabyte

When the modulation is changed to BPSK, the reach is effectively doubled. And Ciena expects a 9,000-10,000km reach on submarine links.

The same single-carrier 50GHz channel reverting to 16-QAM can transmit a 200Gbps signal over distances of 750-1,000km. "A modulation change [to 16-QAM] and adding a second 100 Gigabit Ethernet transceiver and immediately you get an economic improvement," says Adams.

For 400Gbps, two carriers, each 16-QAM, are needed and the distances achieved are 'metro regional', says Ciena.

The transmit DSP also can implement spectral shaping. According to Ciena, by shaping the signals sent, a 20-30% bandwidth improvement (capacity increase) can be achieved. However that feature will only be fully exploited once networks deploy flexible grid ROADMs.

At OFC/NFOEC. Ciena will be showing a prototype card that will demonstrate the modulation going from BPSK to QPSK to 16-QAM. "We are going to be deployed, running live traffic in many customers’ networks by the end of the year," says Adams.

Analysis

Sterling Perrin, senior analyst, Heavy Reading

Heavy Reading believes Ciena's WaveLogic 3 is an impressive development, compared to its current WaveLogic 2 and to other available coherent chipsets. But Perrin thinks the most significant WaveLogic 3 development is Ciena’s single-carrier 100Gbps debut.

Until now, Ciena has used two carriers within a 50GHz, each carrying 50Gbps of data.

"The dual carrier approach gave Ciena a first-to-market advantage at 100Gbps, but we have seen the vendor lose ground as Alcatel-Lucent rolled out its single carrier 100Gbps system," says Perrin in a Heavy Reading research note. "We believe that Alcatel-Lucent was the market leader in 100Gbps transport in 2011."

Other suppliers, including Cisco Systems and Huawei, have also announced single-carrier 100Gbps, and more single-wavelength 100Gbps announcements will come throughout 2012.

Heavy Reading believes the ability to scale to 400Gbps is important, as is the use of multiple carriers (or super-channels). But 400 Gigabit and 1 Terabit transport are still years away and 100Gbps transport will be the core networking technology for a long time yet.

"The vendors with the best 100G systems will be best-positioned to capture share over the next five years, we believe," says Perrin.

Ron Kline, principal analyst for Ovum’s network infrastructure group.

For Ron Kline, Ciena's announcement was less of a surprise. Ciena showcased WaveLogic 3's to analysts late last year. The challenge with such a technology announcement is understanding the capabilities and how it will be rolled out and used within a product, he says.

"Ciena's WaveLogic 3 is the basis for 400 Gig," says Kline. "They are not out there saying 'we have 400 Gig'." Instead, what the company is stressing is the degree of added capacity, intelligence and flexibility that WaveLogic 3 will deliver. That said, Ciena does have trials planned for 400 Gig this year, he says.

What is noteworthy, says Ovum, is that 400Gbps is within Ciena's grasp whereas there are still some vendors yet to record revenues for 100Gbps.

"Product differentiation has changed - it used to be about coherent," says Kline. "But now that nearly all vendors have coherent, differentiation is going to be determined by who has the best coherent technology."