Data centres to give silicon photonics its chance

The scale of modern data centres and the volumes of transceivers they will use are going to have a significant impact on the optical industry. So claims Facebook, the social networking company.

Katharine Schmidtke

Katharine Schmidtke

Facebook has been vocal in outlining the optical requirements it needs for its large data centres.

The company will use duplex single-mode fibre and has chosen the 2 km mid-reach 100 gigabit CWDM4 interface to connect its equipment.

But the company remains open regarding the photonics used inside transceivers. “Facebook is agnostic to technology,“ says Katharine Schmidtke, strategic sourcing manager, optical technology at Facebook. “There are multiple technologies that meet our requirements.”

That said, Facebook says silicon photonics has characteristics that are appealing.

Silicon photonics can produce integrated designs, with all the required functions placed in one or two chips. Such designs will also be needed in volume, given that a large data centre uses hundred of thousands of optical transceivers, and that requires a high-yielding process. This is a manufacturing model the chip industry excels at, and one that silicon photonics, which uses a CMOS-compatible process, can exploit.

When you bring up a data centre, you don’t just deploy, you deploy a data centre

New business model

What data centres brings to optics is scale. Optical transceiver volumes used by data centres are growing, and growing fast, and will account for half the industry’s demand for Ethernet transceivers by 2020, according to LightCounting Market Research.

Transceivers must be designed with high-volume, low-cost manufacturing in mind from the start. This is different to what the market has done traditionally. “With the telecom industry, you step into volume in more manageable, digestible chunks,” says Schmidtke. “When you bring up a data centre, you don’t just deploy, you deploy a data centre.”

Silicon photonics has already proven it can achieve the required optical performance, says Facebook, what remains open is whether the technology can meet the manufacturing demands of the data centre. What helps its cause is that the data centre provides the volumes needed to achieve such a manufacturing maturity.

Schmidtke is upbeat about silicon photonics’ prospects.

“Why silicon photonics is attractive is integration; you are reducing the number of components and the bill of materials significantly, and that reduces cost,” she says. “Then there is all the alignment and assembly cost reductions; that is what makes this technology appealing.”

Her expectation is that the industry will demonstrate the required level of manufacturing maturity in the coming year. Then the role silicon photonics will play for this market will become clearer.

“Within a year it will be very obvious,” she says.

Silicon photonics: "The excitement has gone"

The opinion of industry analysts regarding silicon photonics is mixed at best. More silicon photonics products are shipping but challenges remain.

Part 1: An analyst perspective

"The excitement has gone,” says Vladimir Kozlov, CEO of LightCounting Market Research. “Now it is the long hard work to deliver products.”

Dale Murray, LightCounting

Dale Murray, LightCounting

However, he is less concerned about recent setbacks and slippages for companies such as Intel that are developing silicon photonics products. This is to be expected, he says, as happens with all emerging technologies.

Mark Lutkowitz, principal at consultancy fibeReality, is more circumspect. “As a general rule, the more that reality sets in, the less impressive silicon photonics gets to be,” he says. “The physics is just hard; light is not naturally inclined to work on the silicon the way electronics does.”

LightCounting, which tracks optical component and modules, says silicon photonics product shipments in volume are happening. The market research firm cites Cisco’s CPAK transceivers, and 40 gigabit PSM4 modules shipping in excess of 100,000 units as examples. Six companies now offer 40 gigabit PSM4 products with Luxtera, a silicon photonics player, having a healthy start on the other five.

Indium phosphide and other technologies will not step back and give silicon photonics a free ride

LightCounting also cites Acacia with its silicon photonics-based low-power 100 and 400 gigabit coherent modules. “At OFC, Acacia made a fairly compelling case, but how much of its modules’ optical performance is down to silicon photonics and how much is down to its advanced coherent DSP chip is unclear,” says Dale Murray, principal analyst at LightCounting. Silicon photonics has not shown itself to be the overwhelming solution for metro/ regional and long-haul networks to date but that could change, he says.

Another trend LightCounting notes is how PAM-4 modulation is becoming adopted within standards. PAM-4 modulates two bits of data per symbol and has been adopted for the emerging 400 Gigabit Ethernet standard. Silicon photonics modulators work really well with PAM-4 and getting it into standards benefits the technology, says LightCounting. “All standards were developed around indium phosphide and gallium arsenide technologies until now,” says Kozlov.

You would be hard pressed to find a lot of OEMs or systems integrators that talk about silicon photonics and what impact it is going to have

Silicon photonics has been tainted due to the amount of hype it has received in recent years, says Murray. Especially the claim that optical products made in a CMOS fabrication plant will be significantly cheaper compared to traditional III-V-based optical components.

First, Murray highlights that no CMOS production line can make photonic devices without adaptation. “And how many wafers starts are there for the whole industry? How much does a [CMOS] wafer cost?” he says.

“You would be hard pressed to find a lot of OEMs or systems integrators that talk about silicon photonics and what impact it is going to have,” says Lutkowitz. “To me, that has always said everything.”

![]() Mark Lutkowitz, fibeReality LightCounting highlights heterogeneous integration as one promising avenue for silicon photonics. Heterogeneous integration involves bonding III-V and silicon wafers before processing the two.

Mark Lutkowitz, fibeReality LightCounting highlights heterogeneous integration as one promising avenue for silicon photonics. Heterogeneous integration involves bonding III-V and silicon wafers before processing the two.

This hybrid approach uses the III-V materials for the active components while benefitting from silicon’s larger (300 mm) wafer sizes and advanced manufacturing techniques.

Such an approach avoids the need to attach and align an external discrete laser. “If that can be integrated into a WDM design, then you have got the potential to realise the dream of silicon photonics,” says Murray. “But it’s not quite there yet.”

This poses a real challenge for silicon photonics: it will only achieve low cost if there are sufficient volumes, but without such volumes it will not achieve a cost differential

Murray says over 30 vendors now make modules at 40 gigabit and above: “There are numerous module types and more are being added all the time.” Then there is silicon photonics which has its own product pie split. This poses a real challenge for silicon photonics: it will only achieve low cost if there are sufficient volumes, but without such volumes it will not achieve a cost differential.

“Indium phosphide and other technologies will not step back and give silicon photonics a free ride, and are going to fight it,” says Kozlov. Nor is it just VCSELs that are made in high volumes.

LightCounting expects over 100 million indium phosphide transceivers to ship this year. Many of these transceivers use distributed feedback (DFB) lasers and many are at 10 gigabit and are inexpensive, says Kozlov.

For FTTx and GPON, bi-directional optical subassemblies (BOSAs) now cost $9, he says: “How much lower cost can you get?”

Is the tunable laser market set for an upturn?

Part 2: Tunable laser market

"The tunable laser market requires a lot of patience to research." So claims Vladimir Kozlov, CEO of LightCounting Market Research. Kozlov should know; he has spent the last 15 years tracking and forecasting lasers and optical modules for the telecom and datacom markets.

Source: LightCounting, Gazettabyte

Source: LightCounting, Gazettabyte

The tunable laser market is certainly sizeable; over half a million units will be shipped in 2014, says LightCounting. But the market requires care when forecasting. One subtlety is that certain optical component companies - Finisar, JDSU and Oclaro - are vertically integrated and use their own tunable lasers within the optical modules they sell. LightCounting counts these as module sales rather than tunable laser ones.

Another issue is that despite the development of advanced reconfigurable optical add/ drop multiplexers (ROADMs) and tunable lasers, the uptake of agile optical networking has been limited.

"Verizon is bullish on getting the next generation of colourless, directionless and contentionless ROADMS to reconfigure the network on-the-fly," says Kozlov. "But I'm not so sure Verizon is going to be successful in convincing the industry that this is going to be a good market for [ROADM] suppliers to sell into."

Reconfigurability helps engineers at installations when determining which channels to add or drop, but there is little evidence of operators besides Verizon talking about using ROADMS to change bandwidth dynamically, first in one direction and then the other, he says.

Another indicator of the reduced status of tunable lasers is NeoPhotonics's intention to purchase Emcore's tunable external cavity laser as well as its module assets for US $17.5 million. Emcore acquired the laser when it bought Intel's optical platform division for $85 million in 2007, while Intel acquired it from New Focus in 2002 for $50 million. NeoPhotonics has also spent more in the past: it bought Santur's tunable laser for $39 million in 2011.

"There was so much excitement with so many players [during the optical bubble of 1999-2000], the market was way too competitive and eventually it drove vendors to the point where they would prefer to sell the business for pennies rather than keep it running," says Kozlov. "Emcore has been losing money, it is not a highly profitable business." Yet for Kozlov, Emcore's tunable laser is probably the best in the business with its very narrow line-width compared to other devices.

Tunable laser market

Tunable lasers have failed to get into the mainstream of the industry. "If you look at DWDM, I'm guessing that 70 percent of lasers sold are still fixed wavelength or temperature-tunable over a few wavelengths," says Kozlov. System vendors such as Huawei and ZTE advertise their systems with tunable lasers. "But when we asked them how they are using tunable lasers, they admitted that the bulk of their shipments are fixed-wavelength devices because whatever little they can save on cost, they will."

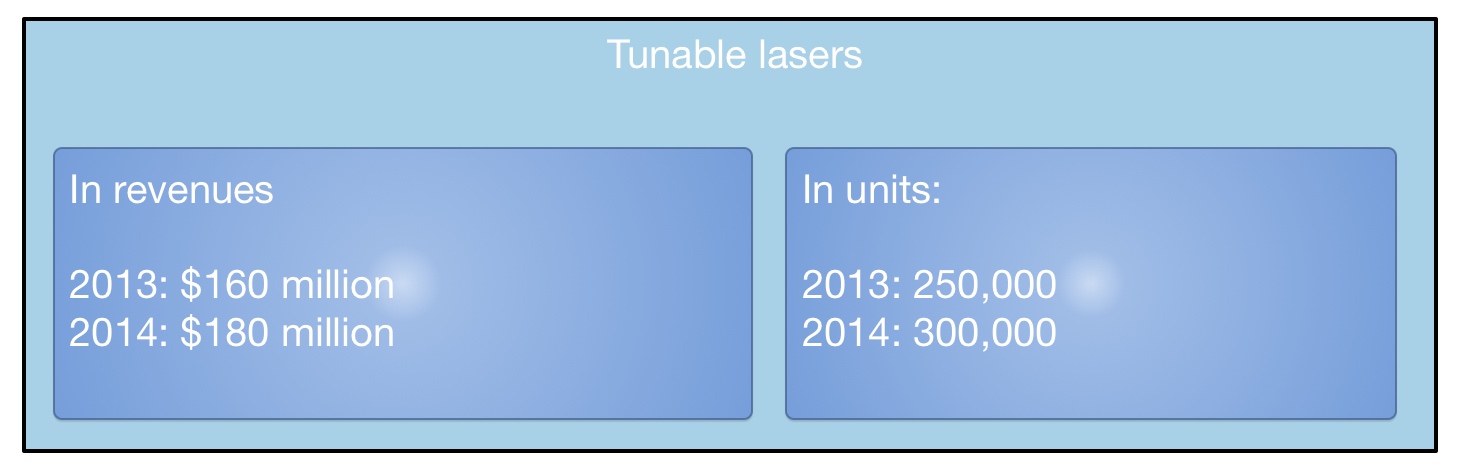

LightCounting valued the 2013 tunable laser market at $160 Million, growing to $180 Million in 2014. This equates to 250,000 units sold in 2013 and 300,000 units this year. "Most of these are for coherent systems," says Kozlov. The number of tunable lasers sold in modules - mainly XFPs but also SFPs and 300-pin modules - is 250,000 million units. "Half a million units a year; if you look at actual shipments, it is quite a lot," says Kozlov.

What next?

"I'm hoping we are reaching the low point in the tunable laser market as vendors are struggling and sales are at a very low valuation," says Kozlov.

The advent of more complex modulation schemes for 400 Gigabit and greater speed optical transmission, and the adoption of silicon photonics-based modulators for long haul will require higher powered lasers. But so much progress has been made by laser designers over the last 15 years, especially during the bubble, that it will last the industry for at least another decade or two, says Kozlov: "Incremental progress will continue and hopefully greater profitability."

For Part 1: NeoPhotonics to expand its tunable laser portfolio, click here

Reporting the optical component & module industry

LightCounting recently published its six-monthly optical market research covering telecom and datacom. Gazettabyte interviewed Vladimir Kozlov, CEO of LightCounting, about the findings.

When people forecast they always make a mistake on the timeline because they overestimate the impact of new technology in the short term and underestimate in the long term

Q: How would you summarise the state of the optical component and module industry?

VK: At a high level, the telecom market is flat, even hibernating, while datacom is exceeding our expectations. In datacom, it is not only 40 and 100 Gig but 10 Gig is growing faster than anticipated. Shipments of 10 Gigabit Ethernet (GbE) [modules] will exceed 1GbE this year.

The primary reason is data centre connectivity - the 'spine and leaf' switch architecture that requires a lot more connections between the racks and the aggregation switch - that is increasing demand. I suspect it is more than just data centres, however. I wouldn't be surprised if enterprises are adopting 10GbE because it is now inexpensive. Service providers offer Ethernet as an access line and use it for mobile backhaul.

Can you explain what is causing the flat telecom market?

Part of the telecom 'hibernation' story is the rapidly declining SONET/SDH market. The decline has been expected but in fact it had been growing up till as recently as two years ago. First, 40 Gigabit OC-768 declined and then the second nail in the coffin was the decline in 10 Gig sales: 10GbE is all SFP+ whereas 0C-192 SONET/SDH is still in the XFP form factor.

The steady dense WDM module market and the growth in wireless backhaul are compensating for the decline in SONET/SDH market as well as the sharp drop this year in FTTx transceiver and BOSA (bidirectional optical sub assembly) shipments, and there is a big shift from transceivers to BOSAs.

LightCounting highlights strong growth of 100G DWDM in 2013, with some 40,000 line card port shipments expected this year. Yet LightCounting is cautious about 100 Gig deployments. Why the caution?

We have to be cautious, given past history with 10 Gig and 40 Gig rollouts.

If you look at 10 Gig deployments, before the optical bubble (1999-2000) there was huge expected demand before the market returned to normality, supporting real traffic demand. Whatever 10 Gig was installed in 1999-2000 was more than enough till 2005. In 2006 and 2007 10 Gig picked up again, followed by 40 Gig which reached 20,000 ports in 2008. But then the financial crisis occurred and the 40 Gig story was interrupted in 2009, only picking up from 2010 to reach 70,000 ports this year.

So 40 Gig volumes are higher than 100 Gig but we haven't seen any 40 Gig in the metro. And now 100 Gig is messing up the 40G story.

The question in my mind is how much metro is a bottleneck today? There may be certain large cities which already require such deployments but equally there was so much fibre deployed in metropolitan areas back in the bubble. If fibre cost is not an issue, why go into 100 Gig? The operator will use fibre and 10 Gig to make more money.

CenturyLink recently announced its first customer purchasing 100 Gig connections - DigitalGlobe, a company specialising in high-definition mapping technology - which will use 100 Gig connectivity to transfer massive amounts of data between its data centers. This is still a special case, despite increasing number of data centers around the world.

There is no doubt that 100 Gig will be a must-have technology in the metro and even metro-access networks once 1GbE broadband access lines become ubiquitous and 10 Gig will be widely used in the access-aggregation layer. It is starting to happen.

So 100 Gigabit in the metro will happen; it is just a question of timing. Is it going to be two to three years or 10-15 years? When people forecast they always make a mistake on the timeline because they overestimate the impact of new technology in the short term and underestimate in the long term.

LightCounting highlights strong sales in 10 Gig and 40 Gig within the data centre but not at 100 Gig. Why?

If you look at the spine and leaf architecture, most of the connections are 10 Gig, broken out from 40 Gig optical modules. This will begin to change as native 40GbE ramps in the larger data centres.

If you go to super-spine that takes data from aggregation to the data centre's core switches, there 100GbE could be used and I'm sure some companies like Google are using 100GbE today. But the numbers are probably three orders of magnitude lower than in a spine and leaf layers. The demand for volume today for 100GbE is not that high, and it also relates to the high price of the modules.

Higher volumes reduce the price but then the complexity and size of the [100 Gig CFP] modules needs to be reduced as well. With 10 Gig, the major [cost reduction] milestone was the transition to a 10 Gig electrical interface. It has to happen with 100 Gig and there will be the transition to a 4x25Gbps electrical interface but it is a big transition. Again, forget about it happening in two-three years but rather a five- to 10-year time frame.

I suspect that one reason for Google offerings of 1Gbps FTTH services to a few communities in the U.S. is to find out what these new application are, by studying end-user demand

You also point out the failure of the IEEE working group to come up with a 100 GbE solution for the 500m-reach sweet spot. What will be the consequence of this?

The IEEE is talking about 400GbE standards now. Go back to 40GbE that was only approved some three years, the majority of the IEEE was against having 40GbE at all, the objective being to go to 100GbE and skip 40GbE altogether. At the last moment a couple of vendors pushed 40GbE. And look at 40GbE now, it is [deployed] all over the place: the industry is happy, suppliers are happy and customers are happy.

Again look at 40GbE which has a standard at 10km. If you look at what is being shipped today, only 10 percent of 40GBASE-LR4 modules are compliant with the standard. The rest of the volume is 2km parts - substandard devices that use Fabry-Perot instead of DFB (distributed feedback) lasers. The yields are higher and customers love them because they cost one tenth as much. The market has found its own solution.

The same thing could happen at 100 Gig. And then there is Cisco Systems with its own agenda. It has just announced a 40 Gig BiDi connection which is another example of what is possible.

What will LightCounting be watching in 2014?

One primary focus is what wireline revenues service providers will report, particularly additional revenues generated by FTTx services.

AT&T and Verizon reported very good results in Q3 [2013] and I'm wondering if this is the start of a longer trend as wireline revenues from FTTx pick up, it will give carriers more of an incentive to invest in supporting those services.

AT&T and Verizon customers are willing to pay a little more for faster connectivity today, but it really takes new applications to develop for end-user spending on bandwidth to jump to the next level. Some of these applications are probably emerging, but we do not know what these are yet. I suspect that one reason for Google offerings of 1Gbps FTTH services to a few communities in the U.S. is to find out what these new application are, by studying end-user demand.

A related issue is whether deployments of broadband services improve economic growth and by how much. The expectations are high but I would like to see more data on this in 2014.

Does Cisco Systems' CPAK module threaten the CFP2?

Cisco Systems has been detailing over recent months its upcoming proprietary optical module dubbed CPAK. The development promises to reduce the market opportunity for the CFP2 multi-source agreement (MSA) and has caused some disquiet in the industry.

Source: Cisco Systems, Gazettabyte, see comments

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people," says Paul Brooks, director for JDSU's high speed transport test portfolio.

Brooks speculates that the advent of CPAK may even cause some module makers to skip the CFP2 and go straight to the smaller CFP4 given the time lag between the two MSAs is relatively short.

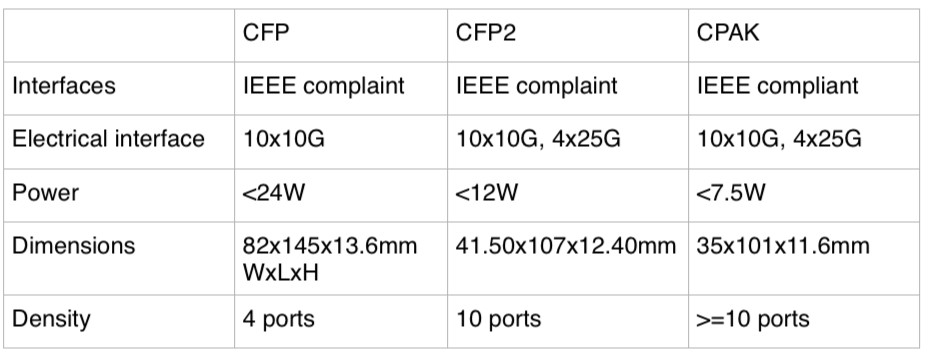

The CPAK module, smaller than the CFP2 MSA and three quarters its volume, has not been officially released and Cisco will not comment on the design but in certain company presentations the CPAK is compared with the CFP. The details are shown in the table above, with the CFP2’s details added.

The CPAK is the first example of Cisco's module design capability following its acquisition of silicon photonics player, Lightwire.

The development of the module highlights how the acquisition of core technology can give an equipment maker the ability to develop proprietary interfaces that promise costs savings and differentiation. But it also raises a question mark regarding the CFP2 and the merit of MSAs when a potential leading customer of the CFP2 chooses to use its own design.

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

"The CFP2 has been a bit slow - the MSA has taken longer than people expected - so Cisco announcing CPAK has frightened a few people"

Paul Brooks, JDSU

Industry analysts do not believe it undermines the CFP2 MSA. “I believe there is business for the CFP2,” says Daryl Inniss, practice leader, Ovum Components. “Cisco is shooting for a solution that has some staying power. The CFP2 is too large and the power consumption too high while the CFP4 is too small and will take too long to get to market; CPAK is a great compromise.”

That said, Inniss, in a recent opinion piece entitled: Optical integration challenges component/OEM ecosystem, writes:

“Cisco’s Lightwire acquisition provides another potential attack on the traditional ecosystem. Lightwire provides unique silicon photonics based technology that can support low power consumption and high-density modules. Cisco may adopt a proprietary transceiver strategy to lower cost, decrease time to market, and build competitive barriers. It need not go through the standards process, which would enable its competitors and provide them with its technology. Cisco only needs to convince its customers that it has a robust supply chain and that it can support its product.”

Vladimir Kozlov, CEO of market research firm, LightCounting, is not surprised by the development. “Cisco could use more proprietary parts and technologies to compete with Huawei over the next decade,” he says. “From a transceiver vendor perspective, custom-made products are often more profitable than standard ones; unless Cisco will make everything in house, which is unlikely, it is not bad news.”

JDSU has just announced that its ONT-100G test set supports the CFP2 and CFP4. The equipment will also support CPAK. "We have designed a range of adaptors that allows us to interface to other optics including one very large equipment vendor's - Cisco's - own CFP2-like form factor," says Brooks.

However, Brooks still expects the industry to align on a small number of MSAs despite the advent of CPAK. "The majority view is that the CFP2 and CFP4 will address most people's needs," says Brooks. "Although there is some debate whether a QSFP2 may be more cost effective than the CFP4." The QSFP2 is the next-generation compact follow-on to the QSFP that supports the 4x25Gbps electrical interface.

60-second interview with .... Vladimir Kozlov

A Q&A with Vladimir Kozlov, CEO of market research firm, LightCounting. The first of occasional, brief interviews with industry figures.

"You have to look over a longer time frame to understand the industry and appreciate the progress"

What exactly does your job entail?

As the founder and CEO my primary responsibility is to ensure that LightCounting's business grows smoothly. In practice this means managing a small team of industry experts to deliver quality market intelligence to our customers, co-ordinating sales and marketing and looking for new business opportunities.

What aspect of the job do you most enjoy?

I love talking with clients and industry experts. A good discussion is an essential element of market research, sales and business development. Not to mention that many of these people are my good friends by now.

How is the optical industry changing?

Slowly but steadily. If you look at it on a daily or quarterly time frame, it is full of problems and nothing is really changing. You have to look over a longer time frame to understand the industry and appreciate the progress.

What are you working on now?

I recently attended Optinet China held in Beijing. I am working on a report based on that exhibition and starting to work on a forecast report. China is a wild card, the economic systems of Europe are falling apart, and the U.S. is full of uncertainty. Someone needs to come up with a forecast for the next four years, despite this uncertainty. It is a big responsibility and a privilege at the same time.

You have been covering optical as an analyst for over a decade. What advice about market research would you give to someone starting now?

Doing a really good job in market research is much harder than it looks. You have to live on the edge to be able to do it right. Scanning the news and running forecast models is the easy part. Digging deep into the industry by finding the right questions and people who can answer them is much more challenging, but it is also a lot of fun.

Unless you can live on the edge and get excited by challenges, do not go into market research. Really good market research people are a bit crazy…I am not really good at it, but I am learning every day and I will certainly be crazy when it is time to retire.

LightCounting is a market research and consulting company focused on high speed interconnects for the datacom, telecom, and consumer communications.

Is optical components becoming a buyer's market?

"An organisation's gross margins ride on these new products"

Daryl Inniss, Ovum Components.

The global optical component market was down 2% in the second quarter of 2011 at US $1.55 billion, according to Ovum.

The good news is that the market research company is forecasting that modest growth will resume this quarter now that the build-up in component inventory that led to the market contraction has largely been worked through.

But Ovum is warning that there are signs that the continued weak market conditions and fierce competition could lead to sharp price declines even for newer, high-valued products. "An organisation's gross margins ride on these new products," says Daryl Inniss, practice leader, Ovum Components.

Oclaro's CEO on a recent earnings call said he was being asked for price concessions on 40Gbps products. Ovum also says the ROADM and tunable laser XFPs markets are becoming more crowded and competitive.

Inniss stresses that there is no evidence that companies are cutting prices to gain an edge but while he expects volumes will grow, intense pricing pressure should now be expected.

LightCounting points out that the slowdown in sales of optical component and modules in early 2011 has been limited to products that did very well in 2010 or which had long lead times, like wavelength-selective switches for ROADMs and 40Gbps modules. It says there is little, if any, excess inventory of components accumulated across the broader market.

"The telecom transceiver market remained steady in Q1 2011, but it declined further in Q2 mostly due to lower sales of 40Gig client-side modules," says Vladimir Kozlov, CEO of LightCounting. "We expect that by the end of this year, the telecom market segment will be strong again."

Best in a decade

The second quarter market dip follows a period where the optical components industry experienced its strongest yearly growth for a decade. The market reached US $6 billion for the year ending first quarter 2011 - a first since 2001.

So long as network expansion keeps up with traffic, we are looking at sustainable growth”

Vladimir Kozlov, LightCounting

The six quarters of consecutive market growth up to the second quarter was due partly to the overall health of the telecom industry. The service provider industry - wireless and wireline - grew 6% year-on-year between 2Q10 and 1Q11, to reach $1.82 trillion. In turn, the equipment market, mainly telecom vendors but including the likes of Brocade, grew 15% to $41.4 billion.

Ovum attributes the 28% growth in optical components between 2Q10 and 1Q 2011 to strong growth in the fibre-to-the-x (FTTx) market as well as new revenues entering the market from datacom players. A third factor was optical equipment vendors over-ordering long lead-time items – such as ROADMs – to secure supply.

“ROADMS did grow nicely but if you look at wavelength-selective switches, it is not such a big market," says Kozlov. The market research firm says the wavelength-selective switch market was $280 million in 2010.

LightCounting says 10 Gigabit SFP+ optical transceivers was a market highlight in 2010, with volume shipments tripling. Ethernet SFP+ sales alone reached $180 million in 2010, and will grow to $250 million this year.

“The optical component market grew 36% in 2010, and in 2011 we’re projecting it will grow 7%,”says Inniss

But competition is intense. Finisar may be the market leader but only 4% market share separates the players in second through to sixth place, says Ovum. “It’s a very competitive market and there is no breakaway here,” says Inniss.

Another challenge is the emergence of the Chinese optical component players. The large-scale deployment of FTTx being undertaken by the main three Chinese operators means that there is a huge market opportunity for local optical component and module players. The Chinese market also accounts for half the all 40 Gigabit-per-second shipments, according to Infonetics Research.

“Looking at the western suppliers, everyone is reporting slowdowns and drops in the second quarter [of 2011],” says Kozlov. “Yet from the data we are getting from the Chinese optical component players, they grew 35% in 2010 and are on track for 30% growth this year.”

Another challenge is for firms to fund sufficient R&D. Share prices took a severe hit after the companies issued warnings about second-quarter sales. “The entire optical component market is depressed because of the localised correction,” says Inniss. “It will still grow but because it is so much smaller than 2010, capital markets are bashing the companies.”

Since the stock market is an important source of investment, it may take several years for the market to recover the share price levels at the start of 2011. “It won’t stop investment in technology but there is going to be real hard eyes on each decision that is made,” says Inniss.

The main challenge facing optical component players is not so much technical issues but more the requirement to continually decrease costs. This is not new but neither is it going away, says Inniss.

Positive outlook

Yet the analysts expect market growth to continue.

Inniss points to the growing role of optics for short-distance interfaces: “The I/O (input-output) bandwidth requirements are sufficiently high, whether it is the backplane or chip-to-chip connections, that the market realisation is that optics will play a role.”

Ovum also highlights consumer market developments such as the USB 3.0 interface which will drive the market for active optical cables. “It [the consumer market] is not going to happen tomorrow - meaning 2012 - but it is something that is coming and has the potential to transform the industry,” says Inniss.

“Companies such as Finisar and Avago [Technologies] are becoming more assertive in enforcing their intellectual rights,” says Kozlov. This is as a positive development that has been missing in the past: “Protecting your intellectual property ultimately helps you become profitable,” he says.

LightCounting also highlights the need for network investment to keep track with traffic growth. "So long as network expansion keeps up with traffic, we are looking at sustainable growth,” says Kozlov. See Plotting transceiver shipments versus traffic growth.

This article is based on a piece that appeared in the ECOC 2011 exhibition guide.

Plotting transceiver shipments versus traffic growth

Summing transceiver shipments in the core of the network and plotting the data against traffic growth provides useful insights into the state of the network.

"We use transceiver shipment data [from vendors] to calculate how fast the network is growing and compare it to the traffic growth," says Vladimir Kozlov, CEO of market research firm, LightCounting.

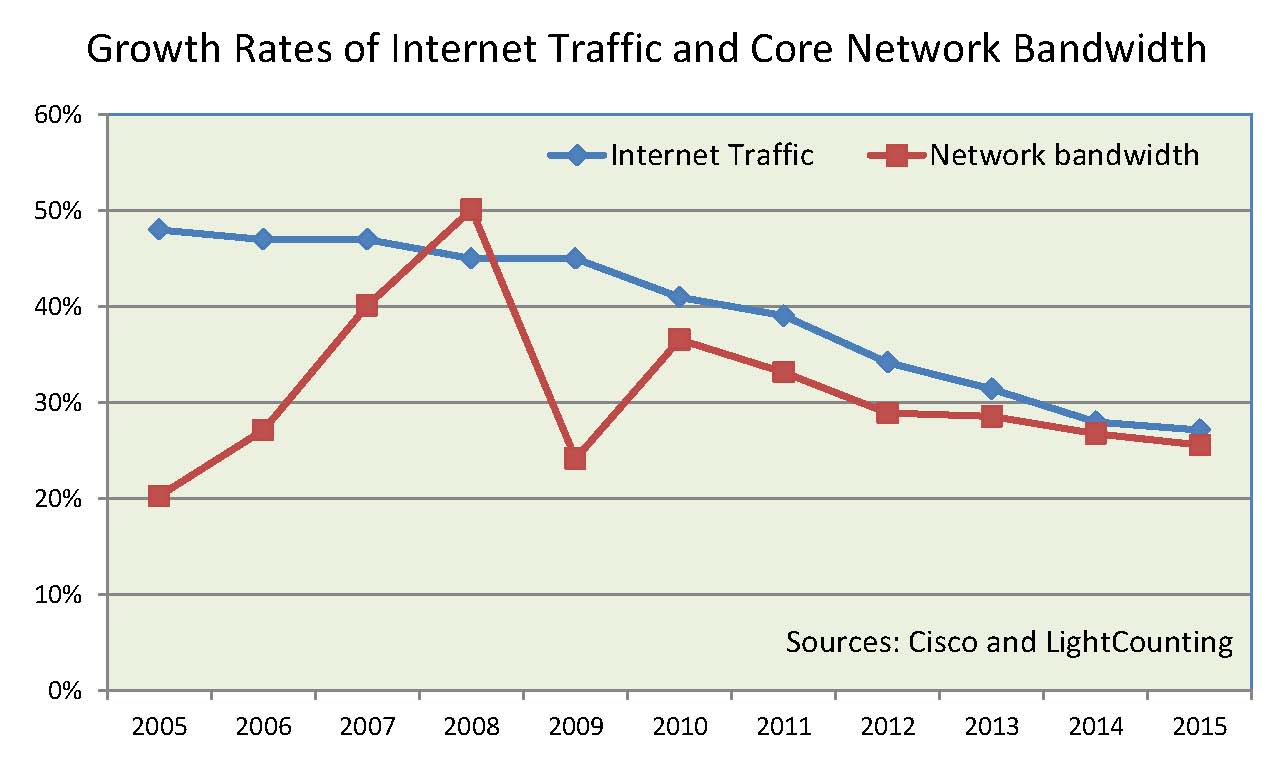

What it reveals is that in 2005-06 there was a significant discrepancy between traffic growth and installed capacity: there was 35-40% traffic growth while investment in dense wavelength division multiplex (DWDM) only grew 20-25%. This gap began to shrink in 2007-08.

LightCounting stresses that network investment must keep track with the traffic growth. "It is not going to be a one-to-one correlation as network efficiency improves over time," says Kozlov. But the gap in the past was too large and probably had to do with unused network capacity.

"As long as the network expansion is to continue just to keep up with traffic, we are looking at sustainable growth," says Kozlov.

Good long-term news for the optical component and module makers.

100 Gig: Is market expectation in need of a reality check?

“It could easily be ten to 15 years before we see 100Gbps in a big way on the public network side”

“It could easily be ten to 15 years before we see 100Gbps in a big way on the public network side”

Mark Lutkowitz, Telecom Pragmatics

Infonetics Research, in a published White Paper, says that 100Gbps technology will be adopted at a faster rate than 40Gbps was in its first years, and that the 100Gbps market will begin in earnest from 2013. Indeed this could even be sooner if China, which accounts for half of all 40Gbps ports being shipped, moves to 100Gbps faster than expected.

LightCounting, in its research, describes 100 Gbps optical transmission as a transformational networking technology for carriers, and forecasts that sales of 100Gbps dense wavelength division multiplexing (DWDM) line cards will grow to US $2.3 billion by 2015.

But one research firm, Telecom Pragmatics, is sounding a note of caution. It reports that the 40Gbps market is growing nicely and believes that it could be at least a decade before there is a substantial 100Gbps market.

“100G is not going to kill 40G and, if anything, we are bullish about 40G,” says Mark Lutkowitz, principal at Telecom Pragmatics. “I’m not talking about large volume ramp-up of 40G but there is arguably a ramp-up.”

100G Paradox

One reason, not often mentioned, why 40Gbps is being adopted is that it does not require as many networking changes as when 100Gbps technology is deployed. “There is additional compensation [needed] and it is not clear that all the fibres will work with 100G,” says Lutkowitz.

There is also what he calls the ‘100G Paradox’.

The 100Gbps technology will most likely be considered at pinch-points in the operators’ networks. Yet these are the same network pinch-points that were first upgraded to 10Gbps. As a result they are likely to have legacy DWDM systems such that upgrading to 100Gbps is a considerable undertaking. “It is questionable whether these systems can even work with 100G,” he says.

"We really think that 40G should be getting a lot more respect than it is getting”

”When you look at service providers they are willing to put up with a whole amount of pain before they buy something, and they will certainly not forklift electronics or fibre - they will only do that as a last resort.” Another attraction of 40Gbps for the operators is its growing maturity - it is a technology that has been available for several years.

Costs

Telecom Pragmatics also dismisses the argument made by component vendors that the market will move to 100Gbps especially if the cost-per-bit of 100G technology declines faster than expected.

“The first cost [point] is ten times 10G and really you need to get to something like six or seven times [the cost of] 10G before you consider 100G,” says Lutkowitz. But that is not the sole cost. Network protection is needed which means a second system and there are additional networking and operational costs associated with 100Gbps.

Moreover, to whatever extent 40G is deployed, it will put further pressure on 100Gbps as 40Gbps prices decline. “In the 10G market, prices continued to decline and that precluded 40G, now you have 40G - to whatever extent there is deployment - precluding 100G,” says Lutkowitz.

“It could easily be 10 to 15 years before we see 100G in a big way on the public network side,” says Lutkowitz. But he stresses that in the datacenter and for the enterprise, demand for 100Gbps technology will be a different story.

Meanwhile Telecom Pragmatics expects further operator trials at 100Gbps as well as new system announcements from vendors. “But we really think that 40G should be getting a lot more respect than it is getting,” says Lutkowitz.

Chinese optical component vendors set for change

“If [Chinese optical component] companies get $100m from an IPO, they have the resources to really do things”

Vladimir Kozlov, LightCounting

The local OC players have benefitted from the prolonged growth of China’s economy, the rise of global telecom system vendors Huawei and ZTE, and the significant expansion in Chinese operators’ networks. But such domestic growth will not continue and will likely lead to a shake-up of the local OC firms.

“They [Chinese OC players] all have the same industry pitch: they all have huge capacity, they have tons of people and they are growing fast but when you research that, you uncover different approaches to doing business,” says Vladimir Kozlov, CEO at LightCounting.

The market research firm has identified several classes of OC player. There are quite a few mid-size companies that focus on niche local opportunities. “Very few of them have an ambition of becoming a global player,” says Kozlov. “They have been set up with local government support, primarily with the aim of employing local people and being involved in local telecom projects.”

But there are other players with broader ambitions and resources. Companies such as HiSense Broadband and HG Genuine, acknowledged manufacturers of electronics and consumer products, have formed OC business units recognising the growth potential of optical communications.

Another category that Western firms will do well to note, says Kozlov, is the Chinese OC players with a long history such as WTD and Accelink. “WTD is 30-years-old and grew from the Wuhan Research Institute that is also a founding body for Chinese system vendor FiberHome,” says Kozlov. WTD has been growing steadily and the pace has accelerated in the last two years. “WTD is becoming more aggressive and is gaining market share while Accelink has a successful IPO that brought in $100m,” he says.

Other companies will likely follow Accelink’s example and raise money through IPOs. But what will be interesting is whether such companies continue to focus on the Chinese market or start addressing issues such as what technologies they are missing and even make acquisitions, he says.

“A lot more companies will have access to financial markets as the regulation that limits how many companies can become public is relaxed,” says Kozlov. “If [Chinese OC] companies get [US] $100m from an IPO, they have the resources to really do things.”

“It is unlikely that Huawei will keep on growing as fast as it did over recent years and continue to take market share from Alcatel-Lucent, Ericsson and others for much longer”

Yet another Chinese OC player segment is start-ups funded by venture capitalists (VCs). One example is Innolight which has received funding from local VCs and a Western company. “VCs will push firms to be as ambitious as possible as they are after returns,” says Kozlov. Interest among the financial investment community is also growing given the rise of the stock price of the OC industry’s leading firms in the last year. Such interest will likely lead to investment and restructuring of local Chinese firms, he says.

Chinese OC vendors have been helped by the rise of the system vendors Huawei and ZTE. The Chinese equipment makers have been disruptive in adopting technology quickly while reducing their costs. But having become global players, Huawei and ZTE now face their own challenges.

“Both [system vendors] companies have caught up on the technology and the next step for them is to see whether they can become leaders in technology and stay ahead of an Alcatel-Lucent or a Ciena,” says Kozlov. “They have the ambition but can they do it?” Kozlov notes that Chinese companies are now highly active with patent applications: “Chinese firms recognise that this is how they will achieve a longer-term advantage and protect their own technologies.”

Another challenge facing the system vendors, common to many technology industries, is that no one player dominates a market. “Usually three global companies share the dominance; the same if it is a local market,” says Kozlov. “It is therefore unlikely that Huawei will keep on growing as fast as it did over recent years and continue to take market share from Alcatel-Lucent, Ericsson and others for much longer.”

This will require Huawei and ZTE to adapt to more moderate growth in future. Meanwhile North American and European system vendors have long responded to the competitive threat, moving their manufacturing to Asia Pacific - and China in particular - to benefit from reduced operating costs. For the Chinese OC vendors, yet to become global players, the chance to be as disruptive as the Chinese system vendors has gone since leading OC vendors have established local manufacturing.

Can Western companies learn from the experience of Chinese system and OC vendors? Kozlov is not so sure.

The Chinese have proved adept at learning the business and mastering new technologies. The examples of Huawei and ZTE that have disrupted the market by being as efficient as possible have proved a wake-up call for Western companies. “I don’t see anything beyond that that Western companies can learn; it is still the Chinese that are learning from Western companies,” says Kozlov. “This does not mean that the Western companies have nothing to worry about; there is plenty of room for improvement in the industry supply chain.”

Looking at the decade ahead, Kozlov expects Huawei to have a much greater penetration in the North American telecom market. “And as it [Huawei] builds up its own intellectual property, it will be better able to compete with Cisco Systems and H-P in the datacom market,” says Kozlov. And as Chinese companies get access to greater finance he also expects they will start acquiring Western firms to gain expertise and greater access to markets.