Cisco Systems' coherent power move

Cisco Systems announced its intent to acquire the optical transmission specialist CoreOptics back in May. CoreOptics has digital signal processing expertise used to enhance high-speed long-haul dense wavelength division multiplexing (DWDM) optical transmission. Cisco’s acquisition values the German company at US $99m.

"Let me be clear, we don’t believe 100Gbps serial will dominate the market for a long time, or 40Gbps for that matter"

Mark Lutkowitz, Telecom Pragmatics

“It has become clear that Cisco, with a few exceptions, has cornered the coherent market for 40 Gig and 100 Gig,” says Mark Lutkowitz, principal at market research firm, Telecom Pragmatics, which has published a report on Cisco's move.

Prior to Cisco’s move, several system vendors were working with CoreOptics for coherent transmission technology at 40 and 100 Gigabit-per-second (Gbps). Nokia Siemens Networks (NSN) was one and had invested in the company, another was Fujitsu Network Communications. Telecom Pragmatics believes other firms were also working with CoreOptics including Xtera and Ericsson (CoreOptics had worked with Marconi before it was acquired by Ericsson).

ACG Research in its May report Cisco/ CoreOptics Acquisition: What Does It Mean for the Packet Optical Transport Space? also claimed that the Cisco acquisition would set back NSN and Ericsson and listed other system vendors such as ADVA Optical Networking and Transmode that may have been considering using CoreOptics’ 100Gbps multi-source agreement (MSA) design.

“The mere fact that you have all these companies working with CoreOptics - and we don’t know all of them – says it all,” says Lutkowitz. “This was the company they were initially going to be depending on and Cisco made a power move that was brilliant.”

With Cisco bringing CoreOptics in-house, these system vendors will need to find a new coherent technology partner. “The next chance would be with a company like Opnext coming out with a sub-system,” says Lutkowitz. “There is no doubt about it – this was a major coup for Cisco.”

For Cisco, the deal is important for its router business more than its optical transmission business. “In terms of transceivers that go into routers and switches it was absolutely essential that Cisco comes up with coherent technology,” says Lutkowitz. Cisco views transport as a low-margin business unlike IP core routers. “This [acquisition] is about protecting Cisco’s bread and butter – the router business,” he says.

The acquisition also has consequences among the router vendors. Alcatel-Lucent has its own 100Gbps coherent technology which it could add to its router platforms. In contrast, the other main router player, Juniper Networks, must develop the technology internally or partner. Telecom Pragmatics claims Juniper has an internal coherent technology development programme.

40 and 100 Gig markets

Cisco kick-started the 40Gbps market when it added the high-speed interface on its IP core router and Lutkowitz expects Cisco to do the same at 100Gbps. “But let me be clear, we don’t believe 100Gbps serial will dominate the market for a long time, or 40Gbps for that matter.”

In Telecom Pragmatics’ view, multiple channels of 10Gbps will be the predominant approach. First, 10Gbps DWDM systems are widely deployed and their cost continues to come down. And while Alcatel-Lucent and Ciena already have 100Gbps systems, they remain expensive given the infancy of the technology.

But with business with large US operators to be won, systems vendors must have a 100Gbps optical transport offering. Verizon has an ultra-long haul request for proposal (RFP), AT&T has named Ciena as its first domain supplier for its optical and transport equipment but a second partner is still to be announced. And according to ACG Research, Google also has DWDM business.

What next?

Besides Alcatel-Lucent, Ciena, Infinera, Huawei, and now Cisco developing coherent technology, several optical module players are also developing 100Gbps line-side optics. These include Opnext, Oclaro and JDS Uniphase. There are also players such as Finisar that has yet to detail their plans. Lutkowitz believes that if Finisar is holding off developing 100Gbps coherent modules, it may prove a wise move given the continuing strength of the 10Gbps DWDM market.

Opnext acquired subsystem vendor StrataLight Communications in January 2009 and one benefit was gaining StrataLight’s systems expertise and its direct access to operators. Oclaro made its own subsystem move in July, acquiring Mintera. Oclaro has also partnered with Clariphy, which is developing coherent receiver ASICs.

But Telecom Pragmatics questions the long-term prospects of high-end line-side module/ subsystem vendors. “This [technology] is the guts of systems and where the money is made,” says Lutkowitz. “Ultimately all the system vendors will look to develop their own subsystems.”

Lutkowitz highlights other challenges facing module firms. Since they are foremost optical component makers it is challenging for them to make significant investment in subsystems. He also questions when the market 100Gbps will take off. “Some of our [market research] competitors talk about 2014 but they don’t know,” says Lutkowitz.

But is not the trend that over time, 40Gbps and 100Gbps modules will gain increasing share of the line side systems optics, as has happened at 10Gbps?

That is certainly LightCounting’s view that sees Cisco’s move as good news for component and transceiver vendors developing 40 and 100Gbps products. LightCounting argues that with Cisco’s commitment to the technology, other system vendors will have to follow suit, boosting demand for the higher-margin products.

“There will be all types of module vendors but it is possible that going higher in the food chain will not work out,” says Lutkowitz. “There will be more module and component vendors than we have now but all I question is: where are the examples of companies that have gone into subsystems that have done relatively well?”

Opnext is likely to be the next vendor with 100Gbps product, says Lutkowitz, and Oclaro could easily come out with its own offering. “All I’m saying is that there is a possibility that, in the final analysis, systems vendors take the technology and do it themselves.”

Ten years gone: Optical components after the boom

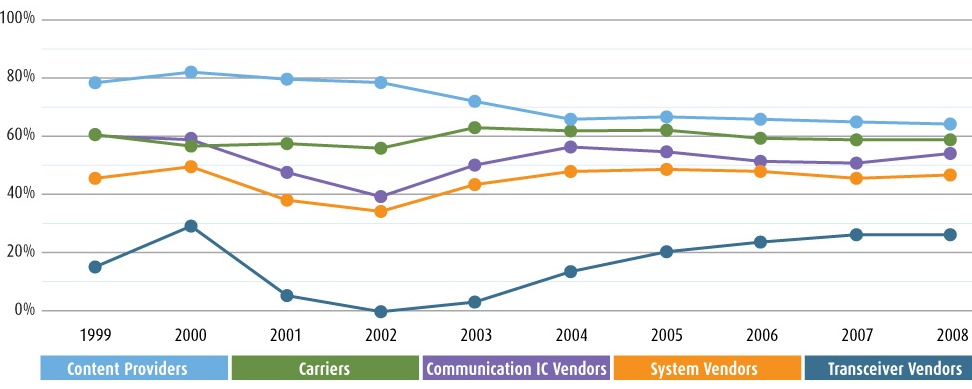

Average gross margin by industry. Source: LightCounting

Average gross margin by industry. Source: LightCounting

The biggest change in the last decade has been the way optics is perceived. That is the view of Vladimir Kozlov, boss of optical transceiver market research firm, LightCounting. “In 2000, optics was set to change the world,” he says. “The intelligent optical network would do all the work for the carrier; nothing would be done electrically.”

The boom of 1999-2000 saw hundreds of start-ups enter the market. Ten years on and a handful only remain; none changed the industry dramatically.

“The worse is definitely behind us”

“The worse is definitely behind us”

Vladimir Kozlov, LightCounting

Kozlov cites tunable lasers as an example. In 2000, the CEO of one start-up claimed the market for tunable lasers would grow to US$1 billion. Today the tunable laser market is worth several tens of millions. “It [the tunable laser] is a useful product that is selling but expectation didn’t match reality,” says Kozlov.

Another example is planar lightwave circuits used to make devices such as arrayed waveguide gratings used to multiplex and demultiplex wavelengths. “Intel was the biggest cheerleader,” says Kozlov. “Did planar lightwave circuits change the industry? No, but it is a useful technology.”

Where significant progress has been made is in the reliability, compactness and cost reduction of optical components. High-end lasers with complex control electronics have been replaced by small, single-chip devices that have minimal associated circuitry, says Kozlov.

Pragmatism not euphoria

The biggest surprise for Kozlov has been how many companies have survived the extremely tough market conditions. “There were almost no sales in 2001 and the market didn’t recover till 2004,” he says. Companies latched on to niche markets outside telecom to get by while many of the start-ups survived on their funding before folding, merging or being acquired by larger players.

“The leading companies such as Finisar, Excelight (now merged with Eudyna to form Sumitomo Electric Device Innovations), Avago Technologies and Opnext were also leading companies 10 years ago,” said Kozlov, who adds Oclaro, created with the merger of Bookham and Avanex.

The market has experienced hiccups since 2004 such as the dip of 2008-2009. “The worse is definitely behind us,” says Kozlov. Many vendors have a good vision as to what to do and plan accordingly. He notes companies are maintaining resources to be well placed to respond to rapid increases in demand. And profitability is rising sharply after the belt-tightening of 2008-09. “Whoever gets in first makes the profit,” says Kozlov. “That is what happened in 1999, although that was an extreme.”

Transceiver vendors and gross margins

Another notable development of the last decade has been the advent of optical transceivers. In the late 1990s system vendors such as Alcatel, Fujitsu, Marconi, NEC and Nortel designed their own optical systems before divesting their optical component arms. Optical component companies exploited the opportunity by developing optical transceivers to sell to the systems vendors.

LightCounting forecasts that the global optical transceiver market will total $2.2 billion in 2010, yet Kozlov still has doubts about the optical transceiver vendors’ business model. “Optical transceiver vendors still have to prove they are profitable and viable, that they are a real layer in the food chain.”

Comparing the gross margin performance of the industry layers that make up the telecom industry, optical transceiver vendors are last (see chart at the top of the page). Gross margin is an efficiency measure as to how well a vendor turns what they manufacture into income. Companies such as Cisco Systems have impressive gross margins of 75%. “You have to own a market, to have something unique to maintain such a margin,” says Kozlov.

Cisco has a unique position and to a degree so do semiconductors players which have gross margins twice those of the transceiver vendors. Contract manufacturers, however, have even lower margins than the 25% achieved by the transceiver vendors, adds Kozlov, but they benefit from large manufacturing volumes.

The main challenge for transceiver vendors is differentiating their products. There is also fierce competition across product segments. “A gross margin of 25% is not the end of the world as long as there are sufficient volumes,” says Kozlov. “And of course 25% in China is a lot – local [optical transceiver] vendors don’t think twice about entering the market.”

Kozlov says there are now between 20-30 Chinese optical transceiver vendors. “Some two thirds are benefiting from government funding but a third are building laser manufacturing and making transceivers, are real, and are here to stay.”

Bandwidth drives components

LightCounting collects quarterly shipment data from leading optical transceiver vendors worldwide. It also forecasts market demand based on a traffic model. Kozlov stresses the importance of the adoption of broadband schemes such as fibre-to-the-x (FTTx) as a traffic driver and ultimately transceiver sales.

A small change in the bandwidth utilisation of the access network has a huge impact on the network core. The advent of a killer application or the emergence of devices such as the iPhone and iPad that change user habits and drive access network utilisation from 2% to 5% would have a marked impact on operators’ networks. “This would require a significant upgrade and would result in a very nice bubble,” says Kozlov.

Utilised bandwidth (terabits-per-second). Scenario 2 with the higher utilisation in the access network quickly impacts core network capacity. Source: LightCounting

Utilised bandwidth (terabits-per-second). Scenario 2 with the higher utilisation in the access network quickly impacts core network capacity. Source: LightCounting

Another effect LightCounting has noted is that the total transceiver capacity is not keeping pace with growth in network traffic. This discrepancy is caused by operators running their networks more efficiently, explains Kozlov. Collapsing the number of platforms when operators adopt newer, more integrated systems is removing interfaces from the network.

LightCounting does not see operators’ traffic data such that Kozlov can’t know to what degrees operators are running their networks closer to capacity but given the rapid clip in traffic growth this is not a sustainable policy and hence does not explain this overall trend.

The next decade

Kozlov expects the next decade to continue like recent years with optical component companies being conservative and pragmatic. He is optimistic about optics’ adoption in the data centre as interface speeds move to 10Gbps and above, pushing copper to its limit. He also believes active optical cables are here to stay, while photonic integration will play an increasingly important role over time.

Kozlov also believes another bubble could occur especially if there is a need for more bandwidth at the network edge that will with a knock-on effect on the core.

But what gives him most optimism is that he simply doesn’t know. “We were all really wrong 10 years ago, maybe we will be again.”

- Lightwave July 2010: Interview with Vladimir Kozlov. "Can the optical transceiver industry sustain double-digit growth?

The InfiniBand roadmap gets redrawn

“We can already demonstrate in silicon a 30Gbps transmitter."

“We can already demonstrate in silicon a 30Gbps transmitter."

Marek Tlalka, Luxtera

“Our June 2008 roadmap originally projected 4x EDR at less than 80Gbps data rate for 2011,” says Skip Jones, director of technology at QLogic and co-chair of the IBTA’s marketing working group. “The IBTA has increased the data speeds for 2011 due to demand for higher throughput.” A 26Gbps channel rate - or 104Gbps for 4x EDR - is to accommodate the overhead associated with 64/66bit encoding.

The IBTA has also added an interim speed, dubbed Fourteen Data Rate (FDR), operating at 14Gbps per channel or 56Gbps for 4x FDR. This, says the IBTA, is to address midrange enterprise applications in the data centre. “Many server OEMs’ backplanes can support speeds up to 56Gbps,” says Jones. “For those OEMs doing a server refresh using existing backplanes, 56Gbps will be the solution they’ll be looking to implement.”

The IBTA dismisses claims by some industry voices that the re-jigged roadmap is to stop InfiniBand falling behind 100 Gigabit Ethernet (GbE) while FDR is to advance InfiniBand while laser vendors grapple with the challenge of developing 26Gbps vertical-cavity surface-emitting lasers (VCSELs) for EDR.

Jones points out that 4x Quad Data Rate (QDR) InfiniBand (4x10Gbps) now accounts for between 60 and 70 percent of newly deployed InfiniBand systems, and that 100Gbps EDR will appear in 2011/ 2012. “The IBTA has a good track record of releasing products on time; as such, 100Gbps InfiniBand will come out much faster than 100 Gigabit Ethernet.” FDR, meanwhile, will benefit from 14Gbps VCSELs for Fibre Channel that will be available next year. Jones admits that developing a 26Gbps VCSEL poses a challenge but that “InfiniBand markets are mostly electrical interconnects”.

“The 4x25G short reach is not going to rise and dominate for quite awhile."

“The 4x25G short reach is not going to rise and dominate for quite awhile."

Scott Schube, LightCounting

“VCSELs are going to have a tough time at 26Gbps per lane, though they'll get there,” says Scott Schube, senior analyst and strategist at optical transceiver market research firm, LightCounting. “There's definitely a push to go to 26Gbps per lane to reduce pin counts, and the chip guys look like they will be ready before the VCSELs.”

One company looking to benefit from the emerging market for EDR is Luxtera. The silicon photonics specialist says its modulator has already been demonstrated at 30Gbps. This is fast enough to accommodate EDR, 100 Gigabit Ethernet (a 4-channel design) and the emerging 28Gbps Fibre Channel standard.

“We can already demonstrate in silicon a 30Gbps transmitter using the same laser as in our existing products and modulated in our silicon waveguides,” says Marek Tlalka, vice president of marketing at Luxtera. “That allows us to cover 14Gbps, 26Gbps EDR, parallel Ethernet as well as 28Gbps for serial Fibre Channel.”

Luxtera will need to redesign the transistor circuitry to drive the modulator beyond the current 15Gbps before the design can be brought to market. It will also use an existing silicon modulator design though the company says some optimisation work will be required.

There are two main product offerings from Luxtera: QSFP-based active optical cables and OptoPHY, one and four-channel optical engines. Luxtera’s OptoPHY product is currently being qualified and is not yet in volume production.

For multi-channel designs, Luxtera uses a continuous-wave 1490nm distributed feedback (DFB) laser fed to the modulated channels. Addressing 28Gbps Fibre Channel, an SFP+ form factor will be used. Luxtera may offer a transceiver product or partner with a module maker with Luxtera providing the optical engine. “It’s an open question,” says Tlalka.

“The IBTA has a good track record of releasing products on time; as such, 100Gbps InfiniBand will come out much faster than 100 Gigabit Ethernet.”

“The IBTA has a good track record of releasing products on time; as such, 100Gbps InfiniBand will come out much faster than 100 Gigabit Ethernet.”

Skip Jones, IBTA

The company has said that the single-channel and four-channel 10Gbps OptoPHY engine consumes 450mW and 800mW respectively. Going to 26Gbps will increase the power consumption but only by several tens of percent, it says.

The first product from Luxtera will be a pluggable cable followed by a companion OptoPHY. The pluggable active optical cable from Luxtera will support 100GbE and EDR Infiniband. “I’d still place my bets on InfiniBand deploying first followed by 100GbE,” says Tlalka.

But Schube warns that Luxtera faces a fundamental challenge “Leading-edge designs based on proprietary technology to solve commodity problems - more bandwidth for out-of-the-box connections - are never going to get widely adopted, though Luxtera can fill a niche for awhile," he says.

There is also much work to be done before 100Gbps interfaces will be deployed. “The 4x25G short reach is not going to rise and dominate for quite awhile, no matter what the component availability is,” says Schube. That is because switch ASICs, backplanes, connectors and line cards will all first need to be redesigned.

Meanwhile the IBTA has also announced two future placeholder data rates on its InfiniBand roadmap: High Data Rate (HDR) due in 2014 and the Next Data Rate (NDR) sometime after. “We will refrain from identifying the exact lane speed until we are closer to that timeframe to avoid confusion and the possibility - and probability - of changing future lane speeds,” says Jones.

And Luxtera says its modulator can go faster still. “I think we can easily go 40 and 50Gbps,” says Tlalka. “After 50Gbps we’ll have to look at new magic.”

Is a datacom and telecom mini-boom taking place?

Daryl Inniss believes it is largely a reflection of cutbacks that have run their course. “The industry cut back swiftly and deeply when the market started to tank, cutting suppliers and capacity,” says Inniss, practice leader, components at market research firm Ovum.

“I think it's recovery dynamics - people ordering a tiny bit more and there are no parts available such that lead-times are stretching out simulating a boom.”

Brad Smith, LightCounting

Carriers supported the demand with inventory. “Now the industry needs to support both deployments and inventory and with the traffic continuing to grow suppliers cannot meet demand,” he says. Moreover this “bull-whip effect” impacts most severely suppliers furthest removed from the carriers i.e. component vendors.

Brad Smith, senior vice president at optical transceiver market research firm LightCounting, also explains the situation based on events last year.

“There is a shortage of certain parts in optical and semis as a result of cutbacks in manufacturing during 2009,” says Smith, “I think it's recovery dynamics - people ordering a tiny bit more and there are no parts available such that lead-times are stretching out simulating a boom.”

Late last year a research note highlighted industry reports that shortages were becoming more widespread, including components such as integrated circuits and fiber optic transceivers.

However one leading optical transceiver vendor commented that it is shipping everything it can make and that it can’t build stuff fast enough.

So is there a mini-boom after all?

Why optical transceiver vendors are like discus-throwers

Guest blog on Lightwave magazine, click here.

Differentiation in a market that demands sameness

At first sight, optical transceiver vendors have little scope for product differentiation. Modules are defined through a multi-source agreement (MSA) and used to transport specified protocols over predefined distances.

“Their attitude is let the big guys kill themselves at 40 and 100 Gig while they beat down costs"

Vladimir Kozlov, LightCounting

“I don’t think differentiation matters so much in this industry,” says Daryl Inniss, practice leader components at Ovum. “Over time eventually someone always comes in; end customers constantly demand multiple suppliers.”

It is a view confirmed by Luc Ceuppens, senior director of marketing, high-end systems business unit at Juniper Networks. “We do look at the different vendors’ products - which one gives the lowest power consumption,” he says. “But overall there is very little difference.”

For vendors, developing transceivers is time-consuming and costly yet with no guarantee of a return. The very nature of pluggables means one vendor’s product can easily be swapped with a cheaper transceiver from a competitor.

Being a vendor defining the MSA is one way to steal a march as it results in a time-to-market advantage. There have even been cases where non-founder companies have been denied sight of an MSA’s specification, ensuring they can never compete, says Inniss: “If you are part of an MSA, you are very definitely at an advantage.”

Rafik Ward, vice president of marketing at Finisar, cites other examples where companies have an advantage.

One is Fibre Channel where new data rates require high-speed vertical-cavity surface-emitting lasers (VCSELs) which only a few companies have.

Another is 100 Gigabit-per-second (Gbps) for long-haul transmission which requires companies with deep pockets to meet the steep development costs. “One hundred Gigabit is a very expensive proposition whereas with the 40 Gigabit Ethernet LR4 (10km) standard, existing off-the-shelf 10Gbps technology can be used,” says Ward.

"One hundred Gigabit is a very expensive proposition"

"One hundred Gigabit is a very expensive proposition"

Rafik Ward, Finisar

Ovum’s Inniss highlights how optical access is set to impact wide area networking (WAN). The optical transceivers for passive optical networking (PON) are using such high-end components as distributed feedback (DFB) lasers and avalanche photo-detectors (APDs), traditionally components for the WAN. Yet with the higher volumes of PON, the cost of WAN optics will come down.

“With Gigabit Ethernet the price declines by 20% each time volumes double,” says Inniss. “For PON transceivers the decline is 40%.” As 10Gbps PON optics start to be deployed, the price benefit will migrate up to the SONET/ Ethernet/ WAN world, he says. Accordingly, those transceiver players that make and use their own components, and are active in PON and WAN, will most benefit.

“Differentiation is hard but possible,” says Vladimir Kozlov, CEO of optical transceiver market research firm, LightCounting. Active optical cables (AOCs) have been an area of innovation partly because vendors have freedom to design the optics that are enclosed within the cabling, he says.

AOCs, Fibre Channel and 100Gbps are all examples where technology is a differentiator, says Kozlov, but business strategy is another lever to be exploited.

On a recent visit to China, Kozlov spoke to ten local vendors. “They have jumped into the transceiver market and think a 20% margin is huge whereas in the US it is seen as nothing.”

The vendors differentiate themselves by supplying transceivers directly to the equipment vendors’ end customers. “They [the Chinese vendors] are finding ways in a business environment; nothing new here in technology, nothing new in manufacturing,” says Kozlov.

He cites one firm that fully populated with transceivers a US telecom system vendor’s installation in Malaysia. “Doing this in the US is harder but then the US is one market in a big world,” says Kozlov.

Offshore manufacturing is no longer a differentiator. One large Chinese transceiver maker bemoaned that everyone now has manufacturing in China. As a result its focus has turned to tackling overheads: trimming costs and reducing R&D.

“Their attitude is let the big guys kill themselves at 40 and 100 Gig while they beat down costs by slashing Ph.Ds, optimising equipment and improving yields,” says Kozlov. “Is it a winning approach long term? No, but short-term quite possibly.”

Do multi-source agreements benefit the optical industry?

System vendors may adore optical transceivers but there is a concern about how multi-source agreements originate.

Optical transceiver form factors, defined through multi-source agreements (MSAs), benefit equipment vendors by ensuring there are several suppliers to choose from. No longer must a system vendor develop its own or be locked in with a supplier.

“Personally, the MSA is the worst thing that has happened to the optical industry”

“Personally, the MSA is the worst thing that has happened to the optical industry”

Marek Tlaka, Luxtera

Pluggables also decouple optics from the line card. A line card can address several applications simply by replacing the module. In contrast, with fixed optics the investment is tied to the line card. A system can also be upgraded by swapping the module with an enhanced specification version once it is available.

But given the variety of modules that datacom and telecom system vendors must support, there are those that argue the MSA process should be streamlined to benefit the industry.

Traditionally, several transceiver vendors collaborate before announcing an MSA. The CFP MSA announced in March 2009, for example, was defined by Finisar, Opnext and Sumitomo Electric Device Innovations. Since then Avago Technologies has become a member.

“The industry has an interesting model,” says Niall Robinson, vice president of product marketing at Mintera. “A couple of companies can get together, work behind closed doors and announce suddenly an MSA and try to make it defacto in the market.”

Robinson contrasts the MSA process with the Optical Interconnecting Forum’s (OIF) 100Gbps line side work that defined guidelines for integrated transmitter and receiver modules. Here service providers and system vendors also contributed. “It was a much more effective and fair process, allowing for industry collaboration,” says Robinson

Matt Traverso, senior manager, technical marketing at Opnext, and involved in the CFP MSA, also favours an open process. “But the view that the way MSAs are run is not open is a bit of a fallacy,” he says.

“Any MSA that is well run requires iteration with suppliers,” says Traverso. The opposite is also true: poorly run MSAs have short lives, he says. Having too open a forum also runs the risk of creating a one-size-fits-all: “One vendor may want to use the MSA as a copper interface while a carrier will want it for long-haul dense WDM.”

Optical transceiver vendors benefit in another way if they are the ones developing MSAs. “Transceiver vendors will not make life tough for themselves,” says Padraig OMathuna, product marketing director at optical device maker, GigOptix. “If MSAs are defined by system vendors, [transceiver] designs would be a lot more challenging.”

Avago Technologies argues for standards bodies to play a role especially as industry resources become more thinly spread.

“MSAs are not standards; there are items left unwritten and not enough double checking is done,” says Sami Nassar, director of marketing, fiber optic products division at Avago Technologies. There are always holes in the specifications, requiring patches and fixes. “If they [transceivers] were driven by standards bodies that would be better,” says Nassar.

Organisations such as the IEEE don’t address packaging and connectors as part of their standards work. But this may have to change. “The real challenge, as the industry thins out, is ensuring the [MSA] work is thorough,” says Dan Rausch, Avago’s senior technical marketing manager, fiber optic products division. “The challenge for the industry going forward is ensuring good engineering and more robust solutions.”

Marek Tlalka, vice president of marketing at Luxtera, goes further, questioning the very merits of the MSA: “Personally, the MSA is the worst thing that has happened to the optical industry.”

Unlike the semiconductor industry where a framer chip once on a line card delivers revenue for years, a transceiver company may design the best product yet six months later be replaced by a cheaper competitor. “The return on investment is lost; all that work for nothing,” says Tlalka.

“Is it a good development or not? MSAs are out there,” says Vladimir Kozlov, CEO of optical transceiver market research firm, LightCounting. “It helps system vendors, giving them a freedom to buy.”

But MSAs have squeezed transceiver makers, says Kozlov, and he worries that it is hindering innovation as companies cut costs to maximize their return on investment.

“There is continual pressure to reduce the price of optics,” adds Daryl Inniss, Ovum’s practice leader components. If operators are to provide video and high definition TV services and grow revenues then bandwidth needs to become dirt cheap. “Even today optics is not cheap,” says Inniss. Certainly MSAs play an important role in reducing costs.

“The transceiver vendors’ challenge is our benefit,” admits Oren Marmur, vice president, optical networking line of business, network solutions division at system vendor, ECI Telecom. “But we have our own challenges at the system level.”