An insider's view on the merits of optical integration

Tolstikhin is president and CEO of Intengent, the Ottawa-based consultancy and custom design service provider, and an industry veteran of photonic integration. In 2005 he founded OneChip Photonics, a fabless maker of indium phosphide photonic integrated circuits for optical access.

One important lesson he learned at OneChip was how the cost benefit of a photonic integrated circuit (PIC) can be eroded with a cheap optical sub-assembly made from discrete off-the-shelf components. When OneChip started, the selling price for GPON optics was around $100 a unit but this quickly came down to $6. "We needed sales in volumes and they never came close to meeting $6," says Tolstikhin.

OneChip changed strategy, seeing early the emerging opportunity for 100-gigabit optics for the data centre but despite being among the first to demonstrate fully integrated 100-gigabit transmitter and receiver chips – at OFC 2013 – the company eventually folded.

When OneChip started, the selling price for GPON optics was around $100 a unit but this quickly came down to $6

Integent can be seen as the photonic equivalent of an electronic ASIC design house that was common in the chip industry, acting as the intermediary between an equipment vendor commissioning a chip design and the foundry making the chip.

Integent creates designs for system integrators which it takes to a commercial foundry for manufacturing. The company makes stand-alone devices, device arrays, and multi-function PICs. Integent uses the regrowth-free taper-assistant vertical integration (TAVI) indium phosphide process of the California-based foundry Global Communication Semiconductors (GCS). "We have also partnered with a prominent PIC design house, VLC Photonics, for PIC layout and verification testing,” says Tolstikhin. Together, Intengent, VLC and GCS offer a one-stop-shop for the development and production of PICs.

III-V and silicon photonics

Tolstikhin is a big fan of indium phosphide and related III-V semiconductor materials, pointing out that they can implement all the optical functions required for telecom and datacom applications. He is a firm believer that III-V will continue to be the material system of choice for various applications and argues that silicon photonics is not so much a competitor to III-V but a complement.

"Silicon photonics needs indium-phosphide-based sources but also benefits from III-V modulators and detectors, which have better performance than their silicon photonics counterparts," he says.

He admits that indium phosphide photonics cannot compete with the PIC scalability that silicon photonics offers. But that will benefit indium phosphide as silicon photonics matures. Intengent already benefits from this co-existence, offering specialised indium phosphide photonic chip development for silicon photonics as well.

"Silicon photonics cannot compete with indium phosphide photonics in relatively simple yet highest volume optical components for telecom and datacom transceivers," says Tolstikhin. Partly this is due to silicon photonics' performance inferiority but mainly for economical reasons.

Silicon photonics will have its chance, but only where it beats competing technologies on fundamentals, not just cost

There are also few applications that need monolithic photonic integration. Tolstikhin highlights coherent optics as one example but that is a market with limited volumes. Meanwhile, the most promising emerging market - transceivers for the data centre, whether 100-gigabit (4x25G NRZ) PSM or CWDM4 designs or in future 400-gigabit (4x100G PAM4) transceivers, will likely be implemented using optical sub-assembly and hybrid integration technologies.

Tolstikhin may be a proponent of indium phosphide but he does not dismiss silicon photonics' prospects: "It will have its chance, but only where it beats competing technologies on fundamentals, not just cost."

One such area is large-scale optoelectronic systems, such as data processors or switch fabrics for large-scale data centres. These are designs that cannot be assembled using discretes and go beyond the scalability of indium phosphide PICs. "This is not silicon photonics-based optical components instead of indium phosphide ones but a totally different system and possibly network solutions," he says. This is also where co-integration of CMOS electronics with silicon photonics makes a difference and can be justified economically.

He highlights Rockley Photonics and Ayar Labs as start-ups doing just this: using silicon photonics for large-scale electro-photonic integration targeting system and network applications. "There may also be more such companies in the making," says Tolstikhin. "And should they succeed, the entire setup of optics for the data centre and the role of silicon photonics could change quite dramatically."

Verizon prepares its next-gen PON request for proposal

Vincent O'Byrne

Vincent O'Byrne

The NG-PON2 request for proposal (RFP) is being issued after the US operator completed a field test that showed a 40 gigabit NG-PON2 system working alongside Verizon’s existing GPON customer traffic.

The field test involved installing a NG-PON2 optical line terminal (OLT) at a Verizon central office and linking it to a FiOS customer’s home 5 km away. A nearby business location was also included in the trial.

Cisco and PT Inovação, an IT and research company owned by Portugal Telecom, worked with Verizon on the trial and provided the NG-PON2 equipment.

NG-PON2 is the follow-on development to XG-PON1, the 10 gigabit GPON standard. NG-PON2 supports both point-to-point links and a combination of time- and wavelength-division multiplexing that in effect supports a traditional time-division multiplexed PON per wavelength, known as TWDM-PON. The rates TWDM-PON supports include 10 gigabit symmetrical, 10 gigabit downstream and 2.5 gigabit upstream, and 2.5 gigabit symmetrical.

Verizon field-tested the transmission of NG-PON2 signals over a fibre already carrying GPON traffic to show that the two technologies can co-exist without interference, including Verizon’s analogue RF video signal. Another test demonstrated how, in the event of a OLT card fault at the central office, the customer’s optical network terminal (ONT) equipment can detect the fault and retune to a new wavelength, restoring the service within seconds.

Now we know we can deploy this technology on the same fibre without interference and upgrade the customer when the market demands such speed

Verizon is not saying when it will deploy the next-generation access technology. “We have not said as the technology has to become mature and the costs to reduce sufficiently,” says Vincent O'Byrne, director of access technology for Verizon.

It will also be several years before such speeds are needed, he says. “But now we know we can deploy this technology on the same fibre without interference and upgrade the customer when the market demands such speed.”

Verizon expects first NG-PON2 services will be for businesses, while residential customers will be offered the service once the technology is mature and cost-effective, says O’Byrne.

Vodafone is another operator conducting a TWDM-PON field trial based on four 10 gigabit wavelengths, using equipment from Alcatel-Lucent. Overall, Alcatel-Lucent says it has been involved in 16 customer TWDM-PON trials, half in Asia Pacific and the rest split between North America and EMEA.

Further reading

For an update on the NG-PON2 standard, click here

NeoPhotonics' PIC transceiver tackles PON business case

Gazettabyte completes its summary of optical announcements at ECOC, held in Amsterdam. In the third and final part, NeoPhotonics’ GPON multiport transceiver is detailed.

Part 3: NeoPhotonics

“Anything that can be done to get high utilisation of your equipment, which represents your up-front investment, helps the business case"

“Anything that can be done to get high utilisation of your equipment, which represents your up-front investment, helps the business case"

Chris Pfistner, NeoPhotonics

NeoPhotonics has announced a Gigabit passive optical network (GPON) transceiver designed to tackle the high up-front costs operators face when deploying optical access.

The GPON optical line terminal (OLT) transceiver has a split ratio of 1:128 - a passive optical network (PON) supporting 128 end points - yet matches the optical link budget associated with smaller split ratios. The transceiver, housed in an extended SFP module, has four fibre outputs, each supporting a conventional GPON OLT. The transceiver also uses a mode-coupling receiver implemented using optical integration.

According to NeoPhotonics, carriers struggle with the business case for PON given the relatively low take-up rates by subscribers, at least initially. “Anything that can be done to get high utilisation of your equipment, which represents your up-front investment, helps the business case,” says Chris Pfistner, vice president of product marketing at NeoPhotonics. “With a device like this, you can now cover four times the area you would normally cover.”

The GPON OLT transceiver, the first of a family, has been tested by operator BT that has described the technology as promising.

Reach and split ratio

The GPON transceiver supports up to 128 end points yet meets the GPON Class B+ 28dB link budget optical transceiver specification.

The optical link budget can be traded to either maximise the PON’s distance, limited due to the loss per fibre-km, or to support higher split ratios. However, a larger split ratio increases the insertion loss due to the extra optical splitter stages the signal passes through. Each 1:2 splitter introduces a 3.5dB loss, eroding the overall optical link budget and hence the PON’s reach.

GPON was specified with a Class B 20dB and Class C 30dB link budget. However once PON deployments started a 28dB Class B+ was created to match the practical requirements of operators. For Verizon, for example, a reach of 10-11km covers 95% of its single family units, says NeoPhotonics.

Operators wanting to increase the split ratio to 1:64 need an extra 4dB. This has led to the 32dB link budget Class C+. For shorter runs, in such cases as China, the Class C+ is used for a 1:128 split ratio. “They [operators] are willing to give up distance to cover an extra 1-by-2 split,” says Pfistner.

NeoPhotonics supports the 1:128 split ratio without suffering such loss by introducing two techniques: the mode-coupling receiver (MCR) and boosting the OLT transceiver's transmitter power.

A key issue dictating a PON performance is the sensitivity of the OLT's burst mode receiver. The upstream fibres are fed straight onto the NeoPhotonics’ MCR, eliminating the need for a 4x1 combiner (inverse splitter) and a resulting 6dB signal loss.

The GPON OLT transceiver showing the transmit and the mode-coupling receiver. Source: NeoPhotonics

The GPON OLT transceiver showing the transmit and the mode-coupling receiver. Source: NeoPhotonics

The MCR is not a new concept, says Pfistner, and can be implemented straightforwardly using bulk optics. But such an implementation is relatively large. Instead, NeoPhotonics has implemented the MCR as a photonic integrated circuit (PIC) fitting the design within an extended SFP form factor.

“The PIC draws on our long experience of planar lightwave circuit technology, and [Santur’s] indium phosphide array technology, to do fairly sophisticated devices,” says Pfistner. NeoPhotonics acquired Santur in 2011.

The resulting GPON transceiver module fits within an SFP slot but it is some 1.5-2cm longer than a standard OLT SFP. Most PON line cards support four or eight OLT ports. Pfistner says a 1:4 ratio is the sweet spot for initial rollouts but higher ratios are possible.

On the transmit side, the distributed feedback (DFB) laser also goes through a 1:4 stage which introduces a 6dB loss. The laser transmit power is suitably boosted to counter the 6dB loss.

Operators

BT has trialled the optical performance of a transceiver prototype. “BT confirmed that the four outputs each represents a Class B+ GPON OLT output,” says Pfistner. Some half a dozen operators have expressed an interest in the transceiver, ranging from making a request to working with samples.

China is one market where such a design is less relevant at present. That is because China is encouraging through subsidies the rollout of PON OLTs even if the take-up rate is low. Pfistner, quoting an FTTH Council finding, says that there is a 5% penetration typically per year: “Verizon has been deploying PON for six years and has about a 30% penetration.”

Meanwhile, an operator only beginning PON deployments will first typically go after the neighbourhoods where a high take-up rate is likely and only then will it roll out PON in the remaining areas.

After five years, a 25% uptake is achieved, assuming this 5% uptake a year. At a 4x higher split ratio, that is the same bandwidth per user as a standard OLT in a quarter of the area, says NeoPhotonics.

“One big concern that we hear from operators is: Now I'm sharing the [PON OLT] bandwidth with 4x more users,” says Pfistner. “That is true if you believe you will get to the maximum number of users in a short period, but that is hardly ever the case.”

And although the 1:128 split ratio optical transceiver accounts for a small part of the carrier’s PON costs, the saving the MCR transceiver introduces is at the line card level. "That means at some point you are going to save shelves and racks [of equipment],” says Pfistner.

Roadmap

The next development is to introduce an MCR transceiver that meets the 32dB Class C+ specification. “A lot of carriers are about to make the switch from B+ to C+ in the GPON world,” says Pfistner. There will also be more work to reduce the size of the MCR PIC and hence the size of the overall pluggable form factor.

Beyond that, NeoPhotonics says a greater than 4-port split is possible to change the economics of 10 Gigabit PON, for GPON and Ethernet PON. “There are no deployments right now because the economics are not there,” he adds.

“The standards effort is focussed on the 'Olympic thought': higher bandwidth, faster, further reach, mode-coupling receiver (MCR) whereas the carriers focus is: How do I lower the up-front investment to enter the FTTH market?” says Pfistner.

Further reading:

GPON SFP Transceiver with PIC based Mode-Coupled Receiver, Derek Nesset, David Piehler, Kristan Farrow, Neil Parkin, ECOC Technical Digest 2012 paper.

Lightwave: Mode coupling receiver increases PON split ratios, click here

Ovum: Lowering optical transmission cost at ECOC 2012, click here

Summary Gazettabyte stories from ECOC 2012, click here

ZTE takes PON optical line terminal lead

ZTE shipped 1.8 million passive optical network (PON) optical line terminals (OLTs) in 2011 to become the leading supplier with 41 percent of the global market, according to Ovum.

"ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing"

"ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing"

Song Shi Jie, ZTE

The market research firm also ranks the Chinese equipment maker as the second largest supplier of PON optical network terminals (ONT), with 28 per cent global market share in 2011.

China now accounts for over half the total fibre-to-the-x (FTTx) deployments worldwide. ZTE says 1.05 million of its OLTs were deploy in China, with 70 percent for the EPON standard and the rest GPON. Overall EPON accounts for 85% of deployments in China. However GPON deployments are growing and ZTE expects the technology to gain market share in China.

There are some 300 million broadband users in China, made up of DSL, fibre-to-the-building (FTTB) and -curb (FTTC), says Song Shi Jie, director of fixed network product line at ZTE.

Of the three main operators, China Telecom is the largest. It is deploying FTTB and is moving to fibre-to-the-home (FTTH) deployments using GPON. China Unicom has a similar strategy. China Mobile is focussed on FTTB and LAN technology; because it is a mobile operator and has no copper line assets it uses LAN cabling for networking within the building.

The split ratio - the number of PON ONTs connected to each OLT - varies depending on the deployment. "In the fibre-to-the-building scenario, the typical ratio is 1:8 or 1:16; for fibre-to-the-home the typical ratio is 1:64," says Song.

ZTE has also deployed 200,000 10 Gigabit EPON (10GEPON) lines in China but none elsewhere, either 10GEPON or XGPON1 (10 Gigabit GPON). "ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing," says Song.

Song attributes ZTE's success to such factors as reduced power consumption of its PON systems and its strong R&D in access.

The vendor says its PON platforms consume a quarter less power than the industry average. Its systems use such techniques as shutting down those OLT ports that are not connected to ONTs. It also employs port idle and sleep modes to save power when there is no traffic. Meanwhile, ZTE has 3,000 engineers engaged in fixed access product R&D.

As for the next-generation NGPON2 being development by industry body FSAN, Song says there are a variety of technologies being proposed but that the picture is still unclear.

ZTE is focussing on three main next-generation PON technologies: wavelength division multiplexing PON (WDM-PON), hybrid time division multiplexing (TDM)/ WDM-PON (or TWDM-PON) and orthogonal frequency division multiplexing (OFDM) PON. "We think OFDM PON can provide high security, high bandwidth and easy network maintenance," says Song.

ZTE says that the NGPON2 standard will be mature in 2015 but that commercial deployments will only start in 2018.

Photonic integration specialist OneChip tackles PON

Briefing: PON

Part 1: Monolithic integrated transceivers

OneChip Photonics is moving to volume production of PON transceivers based on its photonic integrated circuit (PIC) design. The company believes that its transceivers can achieve a 20% price advantage.

"We will be able to sell [our integrated PON transceivers] at a 20% price differential when we reach high volumes"

Andy Weirich, OneChip Photonics

OneChip Photonics has already provided transceiver engineering samples to prospective customers and will start the qualification process with some customers this month. It expects to start delivering limited quantities of its optical transceivers in the next quarter.

The company's primary products are Ethernet PON (EPON) and Gigabit PON (GPON) transceivers. But it is also considering selling a bi-directional optical sub-assembly (BOSA), a component of its transceivers, to those system providers that want to attach the BOSA directly to the printed circuit board (PCB) in their optical network units (ONUs).

"The BOSA is the sub-assembly that contains all the optics, usually the TIA [trans-impedance amplifier] and sometimes the laser driver," says Andy Weirich, OneChip Photonics' vice president of product line management.

The company will roll out its Ethernet PON (EPON) ONU transceivers in the second quarter of 2012, followed by GPON ONU transceivers in the third quarter.

PON Technologies

EPON operates at 1.25 Gigabit-per-second (Gbps) upstream and downstream. OneChip had planned to develop a 2.5Gbps EPON variant which, says OneChip, has been standardised by the China Communications Standards Association (CCSA). But the company has abandoned the design since volumes have been extremely small and there have been no deployments in China.

GPON is a 2.5Gbps downstream/ 1.25Gbps upstream technology. The main differences between GPON and EPON transceiver optical components are the requirement of the ONU's receiver optics and circuitry, and the laser type, says Weirich. GPON's Class B+ specification, used for nearly all the GPON deployments, calls for a 28-29dB sensitivity. This is a more demanding specification requirement to meet than EPON's. GPON also calls for a Distributed Feedback (DFB) laser, whereas an EPON ONU may use either a Fabry-Perot laser or a DFB laser.

OneChip uses the same DFB for GPON and EPON ONUs. Where the PIC designs differ is the receiver assembly where GPON requires amplification. This, says Weirich, is achieved using either an avalanche photodiode (APD) or a semiconductor optical amplifier (SOA).

OneChip will start with an APD but will progress to an SOA. Once it integrates an SOA as part of the PIC, a simpler, cheaper photo-detector can be used.

Weirich admits that it has taken OneChip longer than it expected to develop its monolithically-integrated design.

Part of the challenge has been the issue of packaging the PIC. "Because of our integrated approach and non-alignment-requiring assembly, we have had to solve a few more technology problems," he says. "Our suppliers have had a challenge with some of those issues, and it has taken a couple of iterations to solve."

OneChip says that the good news is that the price erosion of EPON transceivers has slowed down in the last two years. So while Weirich admits the market is more competitive now, what is promising is that volumes have continued to grow.

"There is no sign of saturation happening either in the EPON or GPON markets," he says. And OneChip believes it can compete on price. "What we are saying is that we will be able to sell [our monolithically integrated PON transceivers) at a 20% price differential when we reach high volumes." That is because the monolithic design is simpler and the optical components that make up the design are cheaper, says the company.

10G EPON and XGPON

OneChip believes the end of 2012 will be when 10G EPON volumes start to ramp. "10G EPON is a significantly larger market than 10G GPON [XGPON]," says Weirich, pointing out that some of the largest operators such as China Telecom have backed 10G EPON.

With 10G EPON there are two flavours: the asymmetric (10Gbps downstream and 1.25Gbps upstream) and the symmetric (10Gbps bidirectional) versions.

For an asymmetric 10Gbps ONU transceiver, the laser does not need to change but the optics and electronics at the receiver do, because of the 10Gbps receive signal and because operators want 28-29dB optical link budgets so that 10G EPON can run on the same fibre plant as EPON. "This is an order of magnitude more difficult from a sensitivity perspective than for EPON," says Weirich.

There is demand for the 10G symmetric EPON but it is much lower than the asymmetric version primarily due to cost. "The ONU transceiver with its 10 Gbps laser and photo-detector is quite a bit more costly," says Weirich, complicating the PON's business case.

OneChip says it has a 10G EPON in its product roadmap, but it has not yet made any announcements or made any demonstrations to customers.

Challenges

OneChip is not aware of any other company developing a monolithic integrated design for PON transceivers, in part due to the challenge. It has to be made cheaply enough to compete with the traditional TO-can design. The key is to develop low-cost integration techniques and processes right at the start of the PIC design, he says.

The company says that it is also exploring using its PIC technology to address data centre connectivity.

OneChip Photonics at a glance

OneChip employs some 80 staff and is headquartered in Ottawa, Canada, where it has a 4,000 sq. ft. cleanroom. The start-up also has a regional office in Shenzhen, China which includes a test lab to serve regional customers.

The company is primarily a transceiver supplier and its main target customers are the tier-one system vendors that supply OLT and ONU equipment. "When you think of the big three players in China, Huawei, ZTE and Fiberhome would be among those we are targeting," says Steve Bauer, vice president of marketing and communications, as well as players such as Alcatel-Lucent and Motorola. As mentioned, the company is also considering selling its BOSA design to ONU makers.

In May 2011 the company received $18M in its latest round of funding. "We are transitioning from product development to becoming operationally ready to manufacture in volume," says Bauer.

Fabrinet and Sanmina-SCI are two contract manufacturers that the company is using for transceiver testing and assembly while it has partnerships with several other fabs for supply of wafers, wafer fabrication and silicon optical benches.

R&D: At home or abroad?

Omer Industrial Park in the Negev, Israel - the location of ECI Telecom's latest R&D centre.

Omer Industrial Park in the Negev, Israel - the location of ECI Telecom's latest R&D centre.

Chaim Urbach likes working at the Omer Industrial Park site. Normally located at ECI’s headquarters in Petah Tikva, he visits the Omer site - some 100km away - once or twice a week and finds he is more productive there. Urbach employs an open door policy and has fewer interruptions at the Omer site since engineers are focussed solely on R&D work.

ECI set up its latest R&D centre in May 2010 with a staff of ten. “In 2009 we realised we needed more engineers,” says Urbach. One year on the site employs 150, by the end of the year it will be 200, and by year-end 2012 the company expects to employ 300. ECI has already taken one unit at the Industrial Park and its operations have already spilt over into a second building.

Urbach says that the decision to locate the new site in the south of Israel was not straightforward.

The company has 1,300 R&D staff, with research centres in the US, India and China. Having a second site in Israel helps in terms of issues of language and time zones but employing an R&D engineer in Israel is several times more costly than an engineer in India or China.

The photos on the wall are part of the winning entries in an ECI company-wide photo competition.

The photos on the wall are part of the winning entries in an ECI company-wide photo competition.

But the Israeli Government’s Office of the Chief Scientist (OCS) is keen to encourage local high-tech ventures and has helped with the funding of the site. In return the backed-venture must undertake what is deemed innovative research with the OCS guaranteed royalties from sales of future telecom systems developed at the site.

One difficulty Urbach highlights is recruiting experienced hardware and software engineers given that there are few local high-tech companies in the south of the country. Instead ECI has relocated experienced engineering managers from Petah Tikva, tasked with building core knowledge by training graduates from nearby Ben-Gurion University and from local colleges.

Work on the majority of ECI’s new projects in being done at the Omer site, says Urbach. Projects include developing GPON access technology for a BT tender as well as extending its successful XDM hybrid+ SDH to all-IP transport platform, which has over 30% market share in India. ECI is undertaking the research on one terabit transmission using OFDM technology, part of the Tera Santa Consortium, at its HQ.

“We realised we needed more engineers”

“We realised we needed more engineers”

Chaim Urbach, ECI Telecom

Urbach admits it is a challenge to compete with leading Far Eastern system vendors on cost and given their R&D budgets. But he says the company is focussed on building innovative platforms delivered as part of a complete solution. “We do not just provide a box,” says Urbach. “And customers know if they have a problem, we go the extra mile to solve it.”

Omer Industrial Park

Omer Industrial Park

The company is highly business oriented, he says, delivering solutions that fit customers’ needs. “Over 95% of all systems ECI has developed have been sold,” he says.

Urbach also argues that Israeli engineers are suited to R&D. “Engineers don’t do everything by the book,” he says. “And they are dedicated and motivated to succeed.”

For more photos of the Omer Industrial Park, click here

BroadLight’s GPON ICs: from packets to apps

BroadLight has announced its Lilac family of customer premise equipment (CPE) chips that support the Gigabit Passive Optical Network (GPON) standard.

The company claims its GPON devices with be the first to be implemented using a 40nm CMOS process. The advanced CMOS process, coupled with architectural enhancements, will double the devices' processing performance while improving by five-fold the packet-processing capability. The devices also come with a hardware abstraction layer that will help system vendors tailor their equipment.

"Traffic models and service models are not stable, and there are a lot of differences from carrier to carrier"

Didi Ivancovsky, BroadLight

Lilac will also act as a testbed for technologies needed for XG-PON, the emerging next generation GPON standard. XG-PON will support a 10 Gigabit-per-second (Gbps) downstream and 2.5Gbps upstream rate, and is set for approval by the International Telecommunication Union (ITU) in September.

Why is this important?

GPON networks are finally being rolled out by carriers after a slow start. Yet the GPON chip market is already mature; Lilac is BroadLight’s third-generation CPE family.

Major chip vendors such as Broadcom and Marvell are also now competing with the established GPON chip suppliers such as BroadLight and PMC-Sierra. “The [big] gorillas are entering [the market],” says Didi Ivancovsky, vice president of marketing at BroadLight.

BroadLight claims it has 60% share of the GPON CPE chip market. For the central office, where the optical line terminal (OLT) GPON integrated circuits (ICs) reside, the market is split between 40% merchant ICs and 60% FPGA-based designs. BroadLight claims it has over 90% of the OLT merchant IC market.

The Lilac family is Broadlight’s response to increasing competition and its attempt to retain market share as deployments grow.

GPON market

US operator Verizon with its FiOS service remains the largest single market in terms of day-to-day GPON deployments. But now significant deployments are taking place in Asia.

“Verizon might still be the largest individual deployer, but China Telecom and China Mobile are catching up fast,” says Jeff Heynen, directing analyst, broadband and video at Infonetics Research. “In fact, the aggregate GPON market in China is now larger than what Verizon has been deploying, given that Verizon’s OLT numbers have really slowed while its optical network terminal (ONT) shipments remain high at some 200,000 per quarter.”

“Verizon might still be the largest individual deployer, but China Telecom and China Mobile are catching up fast”

Jeff Heynen, Infonetics Research

Chinese operators are deploying both GPON and Ethernet PON (EPON) technologies. According to BroadLight, Chinese carriers are moving from deploying multi-dwelling unit (MDU) systems to single family unit (SFU) ONTs.

An MDU deployment involves bringing PON to the basement of a building and using copper to distribute the service to individual apartments. However such deployments have proved less popular that expected such that operators are favouring an ONT-per-apartment.

“Through this transition, China Telecom and China Unicom are also making the transition to GPON,” says Ivancovsky. “End–to-end prices of EPON and GPON are practically the same,” GPON has a download speed of 2.5Gbps and an upload speed of 1.25Gbps (Gbps) while for EPON it is 1.25Gbps symmetrical.

China Telecom and China Unicom are deploying GPON is several provinces whereas in major population centres the PON technology is being left unspecified; vendors can propose either the use of EPON or GPON. “This is a big change, really a big change,” says Ivancovsky.

In India, BSNL and a handful of private developers have been the primary GPON deployers, though the Indian market is still in its infancy, says Heynen. Ericsson has also announced a GPON deployment with infrastructure provider Radius Infratel that will involve 600,000 homes and businesses.

“I expect there to be a follow-on tender for BSNL later this year or early next year that will be twice the size of the first tender of 700,000 total GPON lines,” says Heynen. He also expects MTNL to begin deploying GPON early next year.

In other markets, Taiwan’s Chunghwa Telecom has issued its first tender for GPON. Telekom Malaysia is deploying GPON as is Hong Kong Broadband Network (HKBN), while in Australia the National Broadband Network Company will roll-out a 100Mbps fibre-to-the-home network to 90% of Australian premises over eight years working with Alcatel-Lucent.

“Let’s not forget about Europe, which has been basically dormant from a GPON perspective,” adds Heynen. “We now have commitments from France Telecom, Deutsche Telekom, and British Telecom to roll out more FTTH using GPON, which should help increase the overall market, which really was being driven by Telefonica, Portugal Telecom, and Eitsalat.”

Infonetics expects 2010 to be the first year that GPON revenue will exceed EPON revenue: US $1.4 billion worldwide compared to $1.02 billion. By 2014, the market research firm expects GPON revenue to reach $2.5 billion with EPON revenue - 1.25Gbps and 10Gbps EPON - to be US $1.5 billion. “At this point, China, Japan, and South Korea will be the only major EPON markets with many MSOs also using EPON for FTTH and business services,” says Heynen.

What’s been done?

BroadLight offers a range of devices in the Lilac family. It has enhanced the control processing performance of the CPE devices using 40nm CMOS, and has also added more network processor unit (NPU) cores to enhance the ICs’ data plane processing performance.

“It’s been the same story for some time now,” says Heynen. “System-on-chip vendors differentiate themselves on four key aspects: footprint, power consumption, speed and, most importantly, cost”

A key driver for upping the Lilac family’s control processor’s performance is to support the Java programming language and the OSGi Framework, says Ivancovsky. The OSGi Framework used with embedded systems has yet to be deployed on gateways but is becoming mandatory. This will enable the CPE gateway to run downloaded applications much as applications stores now complement mobile handsets.

BroadLight has also doubled to four the on-chip RunnerGrid NPU cores. “Traffic models and service models are not stable, and there are a lot of differences from carrier to carrier” says Ivancovsky. “This [on-chip] flexibility helps us to have a single device that can support many different requirements.”

As an example, Broadlights cites South Korean operator, SK Broadband, which is deploying an ONT supporting two gigabit Ethernet (GbE) ports – one for laptops and the other for the home’s set-top box. Thus a single GPON 2.5Gbps stream is delivered down the fibre and shared between the PON’s 32 or 64 ONTs, with each ONT having two 1GbE links.“The carrier wants to limit the IPTV downstream rate according to the service level agreement,” says Ivancovsky. Having the network processor as part of the CPE, the carrier can avoid deploying more more expensive NPUs at the central office.

The overall result is a Lilac family rated at 2,000 Dhrystone MIPS (DMIPS) and a packet processing capability of 15 million packets per second (Mpps) compared to BroadLight’s current-generation CPE family of 650-900 DMIPs and 3Mpps.

“Broadlight understands that you have to have a range of chips that provide flexibility across a wide range of CPE and infrastructure types,” says Heynen. The CPE demands of a Verizon differ markedly from those of China Telecom, for example, primarily because average-revenue-per-user expectations are so different. Verizon wants to provide the most advanced integrated CPE, with the ability to do TR-069 remote provisioning and both broadcast and on-demand TV, while China Telecom is concerned with achieving sustained downstream bandwidth, with IPTV being a secondary concern, he says.

Heynen also highlights the devices’ software stack with its open application programming interfaces (APIs) that allow third-party developers to develop applications on top of features already provided in BroadLight’s software stack.

“Residential gateway software stacks used to be dominated by Jungo (NDS). But now chipset companies are developing their own, which helps to reduce licensing costs on a per CPE basis,” says Heynen. “If a silicon vendor can provide a hardware abstraction layer like this, it makes it very attractive to system vendors who need an easy way to customise feature sets for a wide range of customers.”

Is the Lilac GPON family fast enough to support XG-PON?

“We are deep in the design of XG-PON end-to-end: one team is working on the OLT and one on the ONT,” says Ivancovsky. “We expect an FPGA prototype very early in 2011.”

The first XG-PON product will be an OLT ASIC rated at 40Gbps: supporting four XG-PON or 16 GPON ports. One XG-PON challenge is developing a 10Gbps SERDES (serialiser/ deserialiser), says Ivancovsky: “The SERDES in Lilac is a 10Gbps one, a preparation for XG-PON devices.”

Meanwhile, the first XG-PON CPE design will be implemented using an FPGA but the control processor used will be the one used for Lilac. As for data plane processing, NPUs will be added to the OLT design while more NPUs cores will be needed within the CPE device. “The number of cores in the Lilac will not be enough; we are talking about 40Gbps,” says Ivancovsky.

Lilac device members

Ivancovsky highlights three particular devices in the Lilac family that will start appearing from the fourth quarter of this year:

- The BL23530 aimed at GPON single family units with VoIP support. To reduce its cost, a low-cost packaging will be used.

- The BL23570 which is aimed at the integrated GPON gateway market.

- The BL23510, a compact 10x10mm IC to be launched after the first two. The chip’s small size will enable it to fit within an SFP form-factor transceiver. The resulting SFP transceiver can be added to connect a DSLAM platform, or upgrade an enterprise platform, to GPON.

“This new system-on-chip is a technology improvement, especially with respect to the residential gateway software layer, which is a requirement among most operators,” concludes Heynen. “But it should be noted this is an addition to, not a replacement for, existing BroadLight chips that solve different infrastructure requirements.”

WDM-PON: Can it save operators over €10bn in total cost of ownership?

Source: ADVA Optical Networking

Source: ADVA Optical Networking

“The focus of operators to squeeze the last dollar out of the system and optical component vendors is really nonsense.”

Klaus Grobe, ADVA Optical Networking.

Key findings

The total cost of ownership (TCO) of a widely deployed WDM-PON network is at least 20 percent cheaper than the broadband alternatives of VDSL and GPON. Given that the cost of deploying a wide-scale access network in a large western European country is €60bn, a 20 percent cost saving is huge, even if spread over 25 years.

What was modelled?

ADVA Optical Networking wanted to quantify the TCO of three access schemes: wavelength-division-multiplexing passive optical networking (WDM-PON), gigabit PON (GPON) - the PON scheme favoured by European incumbents, and copper-based VDSL (very high bit-rate digital subscriber line).

The company modelled a deployment serving 1 million residences and 10,000 enterprises. “We took seriously the idea of broadband roll out especially when operators talk about it being a strategic goal,” says Klaus Grobe, principal engineer at ADVA Optical Networking. “We wanted a single number that says it all.”

Assumptions

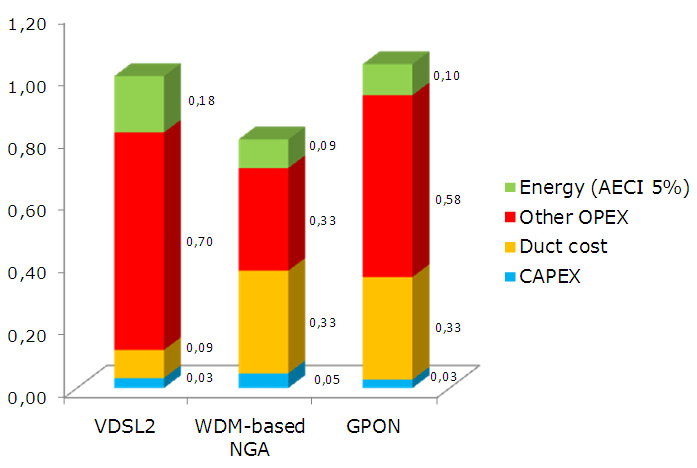

ADVA Optical Networking splits the TCO into four categories:

- Duct cost

- Other operational expense (OpEx)

- Energy consumption

- Capital expenditure (CapEx)

For ducting, it is assumed that VDSL already has fibre to the cabinet and the copper linking the user, whereas for optical access - WDM-PON and GPON - the feeder fibre is present but distribution fibre must be added to connect each home and enterprise. “There is also a certain upgrade of the feeder fibre required but it is 5 percent of the distribution fibre costs,” says Grobe. Hence the ducting costs of GPON and WDM-PON are similar and higher than VDSL.

A 25-year lifetime was also used for the TCO analysis during which three generations of upgrades are envisaged. For the end device like a PON optical network unit (ONU) the cost is the same for each generation, even if performance is significant improved each time.

The ‘other OpEx’ includes all the elements of OpEx except energy costs. The category includes planning and provisioning; operations, administration and maintenance (OA&M); and general overhead.

Planning and provisioning, as the name implies, covers the planning and provisioning of system links and bandwidth, says Grobe. Also the WDM-PON network serves both residential and enterprises whereas duplicate networks are required for GPON and VDSL, adding cost.

The ‘general overheads’ category includes an operator’s sales department. Grobe admits there is huge variation here depending on the operator and thus a common figure for all three cases was used.

Energy consumption is clearly important here. Three annual energy cost increase (AECI) rates were explored – 2, 5 and 10 percent (shown in the chart is the 5% case), with a cost of 80 €/MWh assumed for the first year.

The energy cost savings for WDM-PON come not from the individual equipment but from the reduced number of sites deploying the access technology allows. The power consumed of a WDM-PON ONU is 1W, greater than VDSL, says Grobe, but a lot more local exchanges and cabinets are used for VDSL than for WDM-PON.

And this is where the biggest savings arise: the difference in OA&M due to there being fewer sites for WDM-PON than for GPON and VDSL. That’s because WDM-PON has a larger, up to 100km, reach from the central office to the end user. And, as mentioned, a WDM-PON network caters for enterprise and residential users whereas GPON and VDSL require two distinct networks. This explains the large differences between VDSL, GPON and WDM-PON in the ‘other OpEX’ category.

Grobe says it is difficult to estimate the site reduction deploying WDM-PON will deliver. Operators are less forthcoming with such figures. However, the model and assumptions have been presented to operators and no objections were raised. Equally, the model is robust – varying wildly any one parameter does not change the main findings of the model.

Lastly, for CapEx, WDM-PON equipment is, as expected, the most expensive. CapEx for all three cases, however, is by far the smallest contributor to TCO.

Mass roll outs on the way?

So will operators now deploy WDM-PON on a huge scale? Sadly no, says Grobe. Up-front costs are paramount in operators’ thinking despite the vast cost saving if the lifetime of the network is considered.

But the analysis highlights something else for Grobe that will resonate with the optical community. “The focus of operators to squeeze the last dollar out of system and optical component vendors is really nonsense,” he says.

See ADVA Optical Networking's White Paper

See an associated presentation