Is ADVA Optical Networking looking to buy ECI Telecom?

Is ADVA Optical Networking preparing a bid for private company ECI Telecom? The latest consolidation rumour involving the two mid-tier metro players comes after Infinera’s announcement that it is acquiring Coriant, a deal that is expected to close this quarter.

According to a source in the financial sector, ADVA wanted to acquire Coriant but failed to raise the required funds. Infinera’s successful bid for Coriant has led ADVA to consider alternatives as it looks to secure its future in a consolidating marketplace, with ECI Telecom being viewed as an attractive target.

ECI Telecom is reportedly considering an initial public offering (IPO) on the London Stock Exchange to raise $170 million. A source close to ADVA confirmed that ‘ECI is looking for a home’ but declined to comment on whether ADVA is involved. Another source close to ADVA suggested that there may be some truth in such a bid.

ADVA declined to comment.

An ECI spokesperson said the company has issued no statement regarding an IPO and expressed surprise when asked if ECI was looking to merge. The spokesperson declined to comment when asked about ADVA acquiring ECI.

I wouldn't doubt that there are talks going on, I just don’t know how far they are. And, of course, things can always fall through.

If ADVA and ECI are in discussions, they are doing a good job keeping it quiet. This contrasts with Coriant where rumours started to circulate before the deal was announced.

Mike Genovese, managing director and senior equity research analyst at MKM Partners, who broke the news that Infinera was acquiring Coriant, has no knowledge of any ADVA deal. But he says such a deal fits the industry trend of vendors looking for scale and combining to focus their R&D resources on coherent optics.

Another financial analyst, George Notter, managing director, equity research, telecom and networking equipment analyst at Jefferies, is also unaware of any deal.

“It is a plausible concept,” says Sterling Perrin, principal analyst, optical networking and transport at Heavy Reading. He can see why ADVA is looking and why ECI might be a good fit. “I wouldn't doubt that there are talks going on, I just don’t know how far they are,” says Perrin. “And, of course, things can always fall through.”

Acquisition benefits

Perrin points to ADVA’s Euro 111 million ($131 million) revenues in 3Q 2017, a drop from its Euro 144 million ($165 million) revenues reported in the previous quarter.

ADVA attributed the drop in revenues to two major customers, one an internet content provider (ICP) and the other a large US carrier that was going through a merger. Amazon was the ICP, with ADVA losing some business to Ciena, says Heavy Reading. ADVA’s quarterly revenues have still not returned to their former levels.

“It made ADVA think of how they are going to replace that [business] going forward,” says Perrin. “The webscale business that they bet so heavily on is very competitive, and as they learned with Amazon, the customers are not very loyal.”

By acquiring ECI, ADVA would gain a packet-optical transport platform, a product it lacks, as well as a presence in new markets. ECI has benefitted in recent years from the growing telecom market in India. “Half of ECI’s revenues are coming from Asia, most of that being India,” says Perrin. In contrast, ADVA’s Asian business accounts for over 10 percent of in revenues.

The two firms overlap in wavelength-division multiplexing equipment but not in the data centre interconnect market.

“ADVA might be looking for a land grab and to essentially double down in traditional telecom to make up for losses on the webscale side,” says Perrin.

ADVA’s optical revenues in 2017 were $370 million while Heavy Reading estimates ECI’s optical revenues were $350 million last year

Mature market

Optical transport equipment has become a mature market with fewer than a dozen players remaining. Outside of Asia, the main players are Ciena, Nokia, Cisco, Infinera-Coriant, ADVA and ECI Telecom.

ADVA reported revenues of Euro 514 million in 2017 ($617 million). Heavy Reading says the two companies’ optical revenues are comparable: ADVA’s optical revenues in 2017 were $370 million while Heavy Reading estimates ECI’s optical revenues were $350 million last year. To put that in perspective, market leader Huawei’s optical revenues were $4 billion in 2017.

Both Coriant and ECI are privately held but Perrin says the fortunes of the two firms are very different.

Coriant was a company in decline which explains why its owners, Oaktree Capital Management, was keen for its sale. “ECI is doing really well right now,” says Perrin. ECI's revenues grew over 15 percent in 2017 compared to 2016 and the growth has continued this year. “Which is why you are hearing rumours of them floating publicly.”

ECI is thus in a strong position in any potential negotiations.

Infinera buying Coriant will bring welcome consolidation

Infinera is to purchase privately-held Coriant for $430 million. The deal will effectively double Infinera’s revenues, add 100 new customers and expand the systems vendor’s product portfolio.

Infinera's CEO, Tom FallonBut industry analysts, while welcoming the consolidation among optical systems suppliers, highlight the challenges Infinera faces making the Coriant acquisition a success.

Infinera's CEO, Tom FallonBut industry analysts, while welcoming the consolidation among optical systems suppliers, highlight the challenges Infinera faces making the Coriant acquisition a success.

“The low price reflects that this isn't the best asset on the market,” says Sterling Perrin, principal analyst, optical networking and transport at Heavy Reading. “They are buying $1 of revenue for 50 cents; the price reflects the challenges.”

Benefits

According to Perrin, there are still too many vendors facing "brutal price pressures" despite the optical industry being mature. Removing one vendor that has been cutting prices to win business is good news for the rest.

For Infinera, the acquisition of Coriant promises three main benefits, as outlined by its CEO, Tom Fallon, during a briefing addressing the acquisition.

The first is expanding its vertically-integrated business model across a wider portfolio of products. Infinera develops its own optical technology: its indium-phosphide photonic integrated circuits (PICs) and accompanying coherent DSPs that power its platforms. Having its own technology differentiates the optical performance of its platforms and helps it achieve leading gross margins of over 40 percent, said Fallon.

Exploiting the vertical integration model will be a central part of the Coriant acquisition. Indeed, the company mentioned vertical integration 21 times in as many minutes during its briefing outlining the deal. Infinera expects to deliver industry-leading growth and operating margins once it exploits the benefits of vertical integration across an expanded portfolio of platforms, said Fallon.

Having a seat at the table with the largest global service providers to strategise about where their business is going will be invaluable

Buying Coriant also gives Infinera much-needed scale. Not only will Infinera double its revenues - Coriant’s revenues were about $750 million in 2017 while Infinera’s were $741 million for the same period - but it will expand its customer base including key tier-one service providers and webscale players. According to Fallon, the newly combined company will include nine of the top 10 global tier-one service providers and the six leading global internet content providers.

Infinera admits it has struggled to break into the tier-one operators and points out that trying to enter is an expensive and time-consuming process, estimated at between $10 million to $20 million each time. “[Now, with Coriant,] having a seat at the table with the largest global service providers to strategise about where their business is going will be invaluable,” said Fallon.

Sterling Perrin of Heavy Reading The third benefit Infinera gains is an expanded product portfolio. Coriant has expertise in layer 3 networking, in the metro core with its mTera universal transport platform as well as SDN orchestration and white box technologies. Heavy Reading’s Perrin says Coriant has started development of a layer-3 router white box for edge applications.

Sterling Perrin of Heavy Reading The third benefit Infinera gains is an expanded product portfolio. Coriant has expertise in layer 3 networking, in the metro core with its mTera universal transport platform as well as SDN orchestration and white box technologies. Heavy Reading’s Perrin says Coriant has started development of a layer-3 router white box for edge applications.

Combining the two companies also results in a leading player in data centre interconnect.

“Coriant expands our portfolio, particularly in packet and automation where significant network investment is expected over the next decade,” said Fallon. The deal is happening at the right time, he said, as operators ramp spending as they undertake network transformation.

Infinera will pay $230 million in cash - $150 million up front and the rest in increments - and a further $200 million in shares for Coriant. The company expects to achieve cost savings of $250 million between 2019 and 2021 by combining the two firms, $100 million in 2019 alone. The deal is expected to close in the third quarter of 2018.

If a company is going to put that integrated product into their network, it’s a full-blown RFP process which Infinera may or may not win

Challenges

Industry analysts, while seeing positives for Infinera, have concerns regarding the deal.

A much-needed consolidation of weaker vendors is how George Notter, an analyst at the investment bank, Jefferies, describes the deal. For Infinera, however, continuing as before was not an option. Heavy Reading’s Perrin agrees: ”Infinera has been under a lot of pressure; their core business of long-haul has slowed.”

The deal brings benefits to Infinera: scale, complementary product sets, and the promise of being able to invest more in R&D to benefit its PIC technology, says Notter in a research note.

Gaining customers is also a key positive. “Infinera is really excited about getting the new set of customers and that is what they are paying for,” says Vladimir Kozlov, CEO of LightCounting Market Research. “However, these customers were gained by pricing products at steep discounts.”

What is vital for Infinera is that it delivers its upcoming 2.4-terabit Infinite Capacity Engine 5 (ICE5) optical engine on time. The ICE5 is expected to ship in early 2019. In parallel, Infinera is developing its ICE6 due two years later. Infinera is developing two generations of ICE designs in parallel after being late to market with its current 1.2-terabit optical engine.

Infinera is really excited about getting the new set of customers and that is what they are paying for

But even if the ICE5 is delivered on time, upgrading Coriant's platforms will be a major undertaking. “It sounds like they are going to fit their optical engines in all of Coriant’s gear; I don’t see how that is going to happen anytime quickly,” says Perrin.

Customers bought Coriant's equipment for a reason. Once upgraded with Infinera’s PICs, these will be new products that have to undergo extensive lab testing and full evaluations.

Perrin questions how moving customers off legacy platforms to the new will not result in the service providers triggering a new request-for-proposal (RFP). “If a company is going to put that integrated product into their network, it’s a full-blown RFP process which Infinera may or may not win,” says Perrin. “Infinera talked a lot about the benefits of vertical integration but they didn’t really address the challenges and the specific steps they would take to make that work.”

LightCounting's Vladimir KozlovLightCounting’s Kozlov also questions how this will work.

LightCounting's Vladimir KozlovLightCounting’s Kozlov also questions how this will work.

“The story about vertical integration and scaling up PIC production is compelling, but how will they support Coriant products with the PIC?” he says. “Will they start making pluggable modules internally? Will Coriant’s customers be willing to move away from the pluggables and get locked into Infinera’s PICs? Do they know something that we don’t?”

While Infinera is a top five optical platform supplier globally it hasn’t dominated the market with its PIC technologies, says Perrin. “Even if they technically pull off the vertical integration with the Coriant products, how much is that going to win business for them?” he says. “It is one architecture in a mix that has largely gone to pluggables.”

Transmode

Infinera already has experience acquiring a systems vendor when it bought in 2015 metro-access player, Transmode. Strategically, this was a very solid acquisition, says Perrin, but the jury is still out as to its success.

“The integration, making it work, how Transmode has performed within Infinera hasn’t gone as well as they wanted,” says Perrin. “That said, there are some good opportunities going forward for the Transmode group.”

Infinera also had planned to integrate its PIC technology within Transmode’s products but it didn't make economic sense for the metro market. There may also have been pushback from customers that liked the Transmode products, says Perrin: “With Coriant it looks like they really are going to force the vertical integration.”

Infinera acknowledges the challenges ahead and the importance of overcoming them if it is to secure its future.

“Given the comparable sizes of each company’s revenues and workforce, we recognise that integration will be challenging and is vital for our ultimate success,” said Fallon.

Ciena shops for photonic technology for line-side edge

Part 3: Acquisitions and silicon photonics

Ciena is to acquire the high-speed photonics components division of Teraxion for $32 million. The deal includes 35 employees and Teraxion’s indium phosphide and silicon photonics technologies. The systems vendor is making the acquisition to benefit its coherent-based packet-optical transmission systems in metro and long-haul networks.

Sterling Perrin

Sterling Perrin

“Historically Ciena has been a step ahead of others in introducing new coherent capabilities to the market,” says Ron Kline, principal analyst, intelligent networks at market research company, Ovum. “The technology is critical to own if they want to maintain their edge.”

“Bringing in-house not everything, just piece parts, are becoming differentiators,” says Sterling Perrin, senior analyst at Heavy Reading.

Ciena designs its own WaveLogic coherent DSP-ASICs but buys its optical components. Having its own photonics design team with expertise in indium-phosphide and silicon photonics will allow Ciena to develop complete line-side systems, optimising the photonics and electronics to benefit system performance.

Owning both the photonics and optics also promises to reduce power consumption and improve line-side port density.

“These assets will give us greater control of a critical roadmap component for the advancement of those coherent solutions,” a Ciena spokesperson told Gazettabyte. “These assets will give us greater control of a critical enabling technology to accelerate the pace of our innovation and speed our time-to-market for key packet-optical solutions.”

Ciena have always been do-it-yourself when it comes to optics, and it is an area where they has a huge heritage. So it is an interesting admission that they need somebody else to help them.

The OME 6500 packet optical platform remains a critical system for Ciena in terms of revenues, according to a recent report from the financial analyst firm, Jefferies.

Ciena have always been do-it-yourself when it comes to optics, and it is an area where they have a huge heritage, says Perrin: “So it is an interesting admission that they need somebody else to help them.” It is the silicon photonics technology not just photonic integration that is of importance to Ciena, he says.

Coherent competition

Infinera, which designs its own photonic integrated circuits (PICs) and coherent DSP-ASIC, recently detailed its next-generation coherent toolkit prior to the launch of its terabit PIC and coherent DSP-ASIC. The toolkit uses sub-carriers, parallel processing soft-decision forward-error correction (SD-FEC) and enhanced modulation techniques. These improvements reflect the tighter integration between photonics and electronics for optical transport.

Cisco Systems is another system vendor that develops its own coherent ASICs and has silicon photonics expertise with its Lightwire acquisition in 2012, as does Coriant which works with strategic partners while using merchant coherent processors. Huawei has photonic integration expertise with its acquisitions of indium phosphide UK specialist CIP Technologies in 2012 and Belgian silicon photonics start-up Caliopa in 2013.

Cisco may have started the ball rolling when they acquired silicon photonics start-up Lightwire, and at the time they were criticised for doing so, says Perrin: “This [Ciena move] seems to be partially a response, at least a validation, to what Cisco did, bringing that in-house.”

Optical module maker Acacia also has silicon photonics and DSP-ASIC expertise. Acacia has launched 100 gigabit and 200-400 gigabit CFP optical modules that use silicon photonics.

Companies like Coriant and lots of mid-tier players can use Acacia and rely on the expertise the start-up is driving in photonic integration on the line side, says Perrin. ”Now Ciena wants to own the whole thing which, to me, means they need to move more rapidly, probably driven by the Acacia development.”

Teraxion

Ciena has been working with Canadian firm Teraxion for a long time and the two have a co-development agreement, says Perrin.

Teraxion was founded in 2000 during the optical boom, specialising in dispersion compensation modules and fibre Bragg gratings. In recent years, it has added indium-phosphide and silicon photonics expertise and in 2013 acquired Cogo Optronics, adding indium-phosphide modulator technology.

Teraxion detailed an indium phosphide modulator suited to 400 gigabit at ECOC 2015. Teraxion said at the time that it had demonstrated a 400-gigabit single-wavelength transmission over 500km using polarisation-multiplexed, 16-QAM (PM-16QAM), operating at a symbol rate of 56 gigabaud.

It also has a coherent receiver technology implemented using silicon photonics.

The remaining business of Teraxion covers fibre-optic communication, fibre lasers and optical-sensing applications which employs 120 staff will continue in Québec City.

Mellanox to acquire silicon photonics player Kotura

Source: Gazettabyte

Source: Gazettabyte

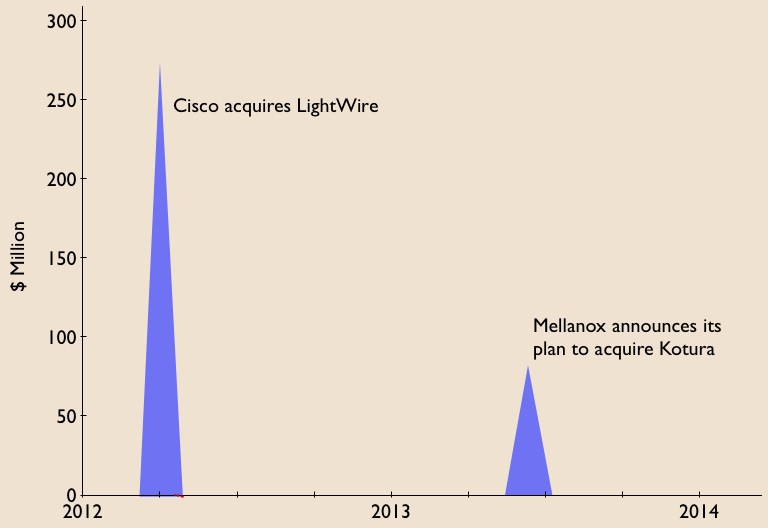

Mellanox Technologies has announced its intention to acquire silicon photonics player, Kotura, for $82 million.

The acquisition will enable Mellanox to deliver 100 Gigabit Infiniband and Ethernet interconnect in the coming two years. lt will also provide Kotura with the resources needed to bring its 100 Gigabit QSFP to market. Mellanox will also gain Kotura's optical engine for use in active optical cables and new mid-plane platform designs, as well as future higher speed interfaces.

The news is also significant for the optical component industry. Kotura is one of the three established merchant silicon photonics players - the others being LightWire and Luxtera - that have spent years developing their technologies.

LightWire was acquired by Cisco Systems in March 2012 for US $271 million and now Mellanox plans to acquire Kotura. The two equipment vendors recognise the value of the technology, bringing it in-house to reduce system interconnect costs and as a long term differentiator for their equipment and ASIC designs. Mellanox, as a silicon photonics player, will compete with Intel, with its own silicon photonics technology, and Cisco Systems.

Kotura has been using its technology to sell telecom products such as variable optical attenuators and multiplexers. The start-up recently announced its 100 Gig QSFP that uses wavelength division multiplexing (WDM) transmitter and receiver chips. The product is to become available in 2014.

In an interview last year, Kotura's CTO, Mehdi Asghari, discussed a roadmap showing how its 100 Gigabit silicon photonics technology could scale to 400 Gigabit and eventually 1.6 Terabit.

"Our devices are capable of running at 40 or 50 Gigabit-per-second (Gbps), depending on the electronics. The electronics is going to limit the speed of our devices. We can very easily see going from four channels at 25Gbps to 16 channels at 25Gbps to provide a 400 Gigabit solution," Asghari told Gazettabyte.

Kotura also discussed how the line rate could be increased to 50Gbps either using a non-return-to-zero (NRZ) line rate or using a multi-level modulation such as pulse amplitude modulation (PAM).

"To get to 1.6 Terabit transceivers, we envisage something running at 40Gbps times 40 channels or 50Gbps times 32 channels. We already have done a single receiver chip demonstrator that has 40 channels, each at 40Gbps," said Asghari.

"These things in silicon are not a big deal. The III-V guys really struggle with yield and cost. But you can envisage scaling to that level of complexity in a silicon platform."

Silicon photonics will not replace existing VCSEL or indium phosphide-based transceiver designs. But there is no doubting silicon photonics is emerging as a key optical technology and the segment is heating up.

If the early start-ups are being acquired, there have been more recent silicon photonics players entering the marketplace such as Aurrion, Skorpios Technologies and Teraxion. There are also internal developments among equipment players such as Alcatel-Lucent, HP Labs and IBM. Indeed Kotura has worked closely with Oracle (Sun Microsystems)

Further acquisitions of silicon photonic players should be expected as companies start designing next generation, denser systems and adopt 100 Gigabit and faster interfaces.

Equally, established optical component and module companies will likely enter quietly (and not so quietly) the marketplace adding silicon photonics to their technology toolkits when the timing is right.

Trends to watch

Two industry trends are underway regarding silicon photonics.

The first is system vendors wanting to own the technology to reduce their costs while recognising a need to control and understand the technology as they tackle more complex equipment designs.

The other, what at first glance is a contrarian trend, is the democratisation of silicon photonics.

The technology is slowly passing from the select few to become more generally available for industry use. For this to happen, the relevant design tools need to mature as do third-party fabrication plants that will manufacture the silicon photonics designs.

Appendix:

On June 4th, 2013, Mellanox announced a definitive agreement to acquire chip company IPtronics for $47.5 million as it builds out its in-house technologies for optical interconnect. Click here

Futher reading:

Avago to acquire CyOptics, click here

Avago to acquire CyOptics

- Avago to become the second largest optical component player

- Company gains laser and photonic integration technologies

- The goal is to grow data centre and enterprise market share

- CyOptics achieved revenues of $210M in 2012

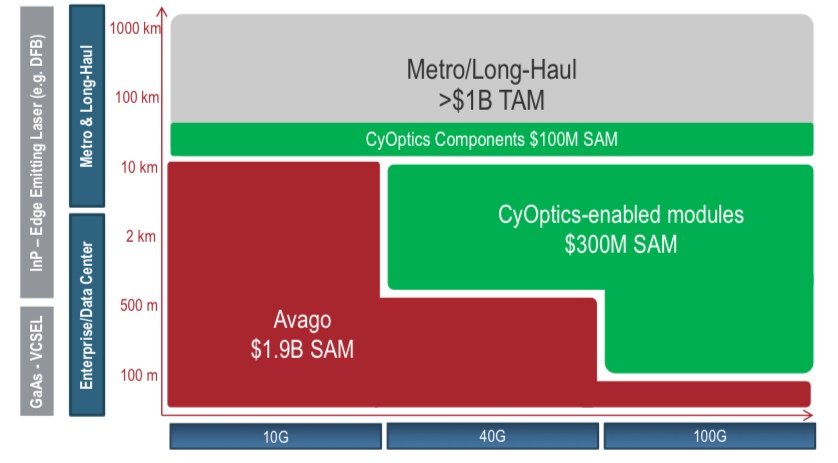

How the acquisition of CyOptics will expand Avago's market opportunities. SAM is the serviceable addressable market and TAM is the total addressable market. Source: Avago

How the acquisition of CyOptics will expand Avago's market opportunities. SAM is the serviceable addressable market and TAM is the total addressable market. Source: Avago

Avago Technologies has announced its plan to acquire optical component player, CyOptics. The value of the acquisition, at US $400M, is double CyOptics' revenues in 2012.

CyOptics' sales were $210M last year, up 21 percent from the previous year. Avago's acquisition will make it the optical component industry's second largest company, behind Finisar, according to market research firm, Ovum. The deal is expected to be completed in the third quarter of the year.

The deal will add indium phosphide and planar lightwave circuit (PLC) technologies to Avago's vertical-cavity surface-emitting laser (VCSEL) and optical transceiver products. In particular, Avago will gain edge laser technology and photonic integration expertise. It will also inherit an advanced automated manufacturing site as well as entry into new markets such as passive optical networking (PON).

Avago stresses its interest in acquiring CyOptics is to bolster its data centre offerings - in particular 40 and 100 Gigabit data centre and enterprise applications - as well as benefit from the growing PON market.

The company has no plans to enter the longer distance optical transmission market beyond supplying optical components.

Significance

Ovum views the acquisition as a shift in strategy. Avago is known as a short distance interconnect supplier based on its VCSEL technology.

"Avago has seen that there are challenges being solely a short-distance supplier, and there are opportunities expanding its portfolio and strategy," says Daryl Inniss, Ovum's vice president and practice leader components.

Such opportunities include larger data centres now being built and their greater use of single-mode fibre that is becoming an attractive alternative to multi-mode as data rates and reach requirements increase.

"Avago's revenues can be lumpy partly because they have a few really large customers," says Inniss.

Another factor motivating the acquisition is that short-distance interconnect is being challenged by silicon photonics. "In the long run silicon photonics is going to win," he says.

What Avago will gain, says Inniss, is one of the best laser suppliers around. And its acquisition will impact adversely other optical module players. "CyOptics is a supplier to several transceiver vendors," says Inniss. "The outlook, two or three years' hence, is decreased business as a merchant supplier."

Inniss points out that CyOptics will represent the second laser manufacturer acquisition this year, following NeoPhotonics's acquisition of Lapis Semiconductor which has 40 Gigabit-per-second (Gbps) electro-absorption modulator lasers (EMLs).

These acquisitions will remove two merchant EML suppliers, given that CyOptics is a strong 10Gbps EML player, and lasers are a key technological asset.

See also:

For a 2011 interview with CyOptics' CEO, click here