JDSU's Brandon Collings on silicon photonics, optical transport & the tunable SFP+

JDSU's CTO for communications and commercial optical products, Brandon Collings, discusses reconfigurable optical add/drop multiplexers (ROADMs), 100 Gigabit, silicon photonics, and the status of JDSU's tunable SFP+.

"We have been continually monitoring to find ways to use the technology [silicon photonics] for telecom but we are not really seeing that happen”

Brandon Collings, JDSU

Brandon Collings highlights two developments that summarise the state of the optical transport industry.

The industry is now aligned on the next-generation ROADM architecture of choice, while experiencing a ’heavy component ramp’ in high-speed optical components to meet demand for 100 Gigabit optical transmission.

The industry has converged on the twin wavelength-selective switch (WSS) route-and-select ROADM architecture for optical transport. "This is in large networks and looking forward, even in smaller sized networks," says Collings.

In a route-and-select architecture, a pair of WSSes reside at each degree of the ROADM. The second WSS is used in place of splitters and improves the overall optical performance by better suppressing possible interference paths.

JDSU showcased its TrueFlex portfolio of components and subsystems for next-generation ROADMs at the recent European Conference on Optical Communications (ECOC) show. The company first discussed the TrueFlex products a year ago. "We are now in the final process of completing those developments," says Collings.

Meanwhile, the 100 Gigabit-per-second (Gbps) component market is progressing well, says Collings. The issues that interest him include next-generation designs such as a pluggable 100Gbps transmission form factor.

Direct detection and coherent

JDSU remains uncertain about the market opportunities for 100Gbps direct-detection solutions for point-to-point and metro applications. "That area remains murky," says Collings. "It is clearly an easy way into 100 Gig - you don't have to have a huge ASIC developed - but its long-term prospects are unclear."

The price point of 100Gbps direct-detection, while attractive, is competing against coherent transmission solutions which Collings describes as volatile. "As coherent becomes comparable [in cost], the situation will change for the 4x25 Gig [direct detection] quite quickly," he says. "Coherent seems to be the long-term, robust cost-effective way to go, capturing most of the market."

At present, coherent solutions are for long-haul that require a large, power-consuming ASIC. Equally the accompanying optical components - the lasers and modulators - are also relatively large. For the coherent metro market, the optics must become cheaper and smaller as must the coherent ASIC.

"If you are looking to put that [coherent ASIC and optics] into a CFP or CFP2, the problem is based on power; cost is important but power is the black-and-white issue," says Collings. Engineers are investigating what features can be removed from the long-haul solution to achieve the target 15-20W power consumption. "That is pretty challenging from an ASIC perspective and leaves little-to-no headroom in a pluggable," says Collings.

The same applies to the optics. "Is there a lesser set of photonics that can sit on a board that is much lower cost and perhaps has some weaker performance versus today's high-performance long-haul?" says Collings. These are the issues designers are grappling with.

Silicon photonics

Another area in flux is the silicon photonics marketplace. "It is a very fluid and active area," says Collings. "We are not highly active in the area but we are very active with outside organisations to keep track of its progress, its capabilities and its overall evolution in terms of what the technology is capable of."

The silicon photonics industry has shifted towards datacom and interconnect technology in the last year, says Collings. The performance levels silicon photonics achieves are better suited to datacom than telecom's more demanding requirements. "We have been continually monitoring to find ways to use the technology for telecom but we are not really seeing that happen,” says Collings.

Tunable SFP+

JDSU demonstrated its tunable laser in an SFP+ pluggable optical module at the ECOC exhibition.

The company was first to market with the tunable XFP, claiming it secured JDSU an almost two-year lead in the marketplace. "We are aiming to repeat that with the SFP+," says Collings.

The SFP+ doubles a line card's interface density compared to the XFP module. The SFP+ supports both 10Gbps client-side and wavelength-division multiplexing (WDM) interfaces. "Most of the cards have transitioned from supporting the XFP to the SFP+," says Collings. This [having a tunable SFP+] completes that portfolio of capability."

JDSU has provided samples of the tunable pluggable to customers. "We are working with a handful of leading customers and they typically have a preference on chirp or no-chirp [lasers], APD [avalanche photo-diode] or no APD, that sort of thing," says Collings.

JDSU has not said when it will start production of the tunable SFP+. "It won't be long," says Collings, who points out that JDSU has been demonstrating the pluggable for over six months.

The company plans a two-stage rollout. JDSU will launch a slightly higher power-dissipating tunable SFP+ "a handful of months" before the standard-complaint device. "The SFP+ standard calls for 1.5W but for some customers that want to hit the market earlier, we can discuss other options," says Collings.

Further reading

Teraxion embraces silicon photonics for its products

Teraxion has become a silicon photonics player with the launch of its compact 40 and 100 Gigabit coherent receivers.

The Canadian optical component company has long been known for its fibre Bragg gratings and tunable dispersion compensation products. But for the last three years it has been developing expertise in silicon photonics and at the recent European Conference on Optical Communications (ECOC) exhibition it announced its first products based on the technology.

"You don't have this [fabless] model for indium phosphide or silica, while an ecosystem is developing around silicon photonics"

Martin Guy, Teraxion

"We are playing mainly in the telecom business, which accounts for 80% of our revenues," says Martin Guy, vice president, product management & technology at Teraxion. "It is clear that our customers are going to more integration and smaller form-factors so we need to follow our customers' requirements."

Teraxion assessed several technologies but chose silicon photonics and the fabless model it supports. "We are using all our optical expertise that we can apply to this material but use a process already developed for the CMOS industry, with the [silicon] wafer made externally," says Guy. "You don't have this [fabless] model for indium phosphide or silica, while an ecosystem is developing around silicon photonics."

The company uses hybrid integration for its coherent receiver products, with silicon implementing the passive optical functions to which the active components are coupled. Teraxion is using externally-supplied photo-detectors which are flip-chipped onto the silicon for its coherent receiver.

"We need to use the best material for the function for this high-end product," says Guy. "Our initial goal is not to have everything integrated in silicon."

Coherent receiver

A coherent receiver comprises two inputs - the received optical signal and the local oscillator - and four balanced receiver outputs. Also included in the design are two polarisation beam splitters and two 90-degree hybrid mixers.

Several companies have launched coherent receiver products. These include CyOpyics, Enablence, NEL, NeoPhotonics, Oclaro and u2t Photonics. Silicon photonics player Kotura has also developed the optical functions for a coherent receiver but has not launched a product.

One benefit of using silicon photonics, says Teraxion, is the compact optical designs it enables.

The Optical Internetworking Forum (OIF) has specified a form factor for the 100 Gigabit-per-second (Gbps) coherent receiver. Teraxion has developed a silicon photonics-based product that matches the OIF's form factor sized 40mmx32mm. This is for technology evaluation purposes rather than a commercial product. "If customers want to evaluate our technology, they need to have a compatible footprint with their design," explains Guy. This is available in prototype form and Teraxion has customers ready to evaluate the product.

Teraxion will come to market with a second 100 Gigabit coherent receiver design that is a third of the size of the OIF's form factor, measuring 23mmx18mm (0.32x the area of the OIF specification). The compact coherent receivers for 40 and 100Gbps will be available in sample form in the first quarter of 2013.

Teraxion's OIF-specification 100 Gig coherent receiver (left) for test purposes and its compact coherent receiver product. Source: Teraxion

Teraxion's OIF-specification 100 Gig coherent receiver (left) for test purposes and its compact coherent receiver product. Source: Teraxion

"We match the OIF's performance with this design but there are also other key requirements from customers that are not necessarily in the OIF specification," says Guy.

The compact 100Gbps design is of interest to optical module and system vendors but there is no one view in terms of requirements or the desired line-side form-factor that follows the 5x7-inch MSA. Indeed there are some that are interested in developing a 100 Gigabit CFP module for metro applications, says Guy.

Roadmap

Teraxion's roadmap includes further integration of the coherent receiver's design. "We are using hybrid integration but eventually we will look at having the photo-detectors integrated within the material,” says Guy.

The small size of the coherent design means there is scope for additional functionality to be included. Teraxion says that customers are interested in integrating variable optical attenuators (VOAs). The local oscillator is another optical function that can be integrated within the coherent receiver.

In 2005 Teraxion acquired Dicos Technologies, a narrow line-width laser specialist. Teraxion's tunable narrow line-width laser product - a few kiloHertz wide - is available in the lab. "The purpose of this product is not to be deployed on the line card - right now," says Guy. "We believe this type of performance will be required for next-generation 100 Gig, 400 Gig, 1 Terabit coherent communication systems where you will need a very 'clean' local oscillator."

Teraxion is also working on developing a silicon-photonics-based modulator. The company has been exploring integrating Bragg gratings within silicon waveguides for which it has applied for patents. This is several years out, says Guy, but has the potential to enable high-speed modulators suited for short-reach datacom applications.

MultiPhy targets low-power coherent metro chip for 2013

MultiPhy has given first details of its planned 100 Gigabit coherent chip for metro networks. The Israeli fabless start-up expects to have samples of the device in 2013.

"We can tolerate greater [signal] impairments which means the requirements on the components we can use are more relaxed"

Avi Shabtai, CEO of MultiPhy

"Coherent metro is always something we have pushed," says Avi Shabtai, CEO of MultiPhy. Now, the company says it is starting to see a requirement for coherent technology's deployment in the metro. "Everyone expects to see it [coherent metro] in the next 2-3 years," he says. "Not tomorrow; it will take time to develop a solution to hit the target-specific [metro] market."

MultiPhy is at an advanced stage in the design of its coherent metro chip, dubbed the MP2100C. "It is going to be a very low power device," says Shabtai. MultiPhy is not quoting target figures but in an interview with the company's CTO, Dan Sadot, a figure of 15W was mentioned. The goal is to fit the design within a 24W CFP. This is a third of the power consumed by long-haul coherent solutions.

The design is being tackled from scratch. One way the start-up plans to reduce the power consumption is to use a one-sample-per-symbol data rate combined with the maximum-likelihood sequence estimation (MLSE) algorithm.

MultiPhy has developed patents that involve sub-Nyquist sampling. This allows the analogue-to-digital converters and the digital signal processor to operate at half the sampling rate, saving power. To use sub-Nyquist sampling, a low-pass anti-aliasing filter is applied but this harms the received signal. Using the filter, sampling at half the rate can occur and using the MLSE algorithm, the effects of the low-pass filtering can be countered. And because of the low-pass filtering, reduced bandwidth opto-electronics can be used which reduces cost.

This low-power approach is possible because the reach requirements in metro, up to 1,000km, is shorter than long haul/ ultra long haul optical transmission links. The shorter-reach requirements also impact the forward error correction codes, needed which can lessen the processing load, and the components, as mentioned. "We can tolerate greater [signal] impairments which means the requirements on the components we can use are more relaxed," says Shabtai.

The company also revealed that the MP2100C coherent device will integrate the transmitter and receiver on-chip.

MultiPhy says it is working with several system vendor and optical module partners on the IC development. Shabtai expects the first industry products using the chip to appear in 2014 or 2015. The timing will also be dependent on the cost and power consumption reductions of the accompanying optical components.

A 100Gbps direct-detection optical module showing MultiPhy's multiplexer and receiver ICs. The module shown is a WDM design. Source: MultiPhy

A 100Gbps direct-detection optical module showing MultiPhy's multiplexer and receiver ICs. The module shown is a WDM design. Source: MultiPhy

100Gbps direct detection multiplexer chip

MultiPhy has also announced a multiplexer IC for 100 Gigabit direct detection. The start-up can now offer customers the MP1101Q, a 40nm CMOS multiplexer complement to its MP1100Q receiver IC that includes a digital signal processor to implements the MLSE algorithm. The MP1100Q was unveiled a year ago.

Testing the direct-detection chipset, MultiPhy says it can compensate +/-1000ps/nm of dispersion to achieve a point-to-point reach of 55km. No other available solution can meet such a reach, claims MultiPhy.

MultiPhy's direct-detection solution also enables 10 Gigabit-per-second (Gbps) opto-electronics components to be used for the transmit and receive paths. At ECOC, MultiPhy announced that it has used Sumitomo Electric's 10Gbps 1550nm externally-modulated lasers (EMLs) to demonstrate a 40km reach.

Using such 10Gbps devices simplifies the design since no 25Gbps components are required. It will also enable more optical module makers to enter the 100 Gigabit marketplace, claims MultiPhy. "It is twice the distance and about half of the cost of any other solution on the market - much below $10,000," says Shabtai.

MultiPhy's HQ in Ness Ziona, Israel

MultiPhy's HQ in Ness Ziona, Israel

The multiplexer device can also be used for traditional 4x28Gbps WDM solutions to achieve a reach in existing networks of up to 800km.

MultiPhy says that it expects the overall 100 Gigabit direct detection market to number 4 optical module makers and 4-5 system vendors by the end of 2012. At present ADVA Optical Networking is offering a 100Gbps direct-detection CFP-based design. ECI Telecom has detailed a 5x7-inch MSA direct-detection 100 Gigabit module, while Finisar and Oclaro have both announced that they are coming to market with 100Gbps direct-detection modules.

Optical industry restructuring: The analysts' view

The view that the optical industry is due a shake-up has been aired periodically over the last decade. Yet the industry's structure has remained intact. Now, with the depressed state of the telecom industry, the spectre of impending restructuring is again being raised.

In Part 2, Gazettabyte asked several market research analysts - Heavy Reading's Sterling Perrin, Ovum's Daryl Inniss and Dell'Oro's Jimmy Yu - for their views.

Part II: The analysts' view

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen"

Sterling Perrin, Heavy Reading

Larry Schwerin, CEO of ROADM subsystem player Capella Intelligent Subsystems, believes optical industry restructuring is inevitable. Optical networking analysts largely agree with Schwerin's analysis. Where they differ is that the analysts say change is already evident and that restructuring will be gradual.

"The industry has not been in good shape for many years," says Sterling Perrin, senior analyst at Heavy Reading. "The operators are the ones with the power [in the supply chain] and they seem to be doing decently but it is not a good situation for the systems players and especially for the component vendors."

Daryl Inniss, practice leader for components at Ovum, highlights the changes taking place at the optical component layer. "There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader," says Inniss.

A typical rule of thumb for an industry in that you need the top three [firms] to own between two thirds and 80 percent of the market, says Inniss: "These are real market leaders that drive the industry; everyone else is a specialist with a niche focus."

But the absence of such dominant players should not be equated with a lack of change or that component companies don't recognise the need to adapt.

"Finisar looks more like an industry leader than we have had before, and its behaviour is that of market leader," says Inniss. Finisar is building an integrated company to become a one-stop-shop supplier, he says, as is the newly merged Oclaro-Opnext which is taking similar steps to be a vertically integrated company. Finisar acquired Israeli optical amplifier specialist RED-C Optical Networks in July 2012.

Capella's Schwerin also wonders about the long term prospects of some of the smaller system vendors. Chinese vendors Huawei and ZTE now account for 30 percent of the market, while Alcatel-Lucent is the only other major vendor with double-digit share.

The rest of the market is split among numerous optical vendors. "If you think about that, if you have 5 percent or less [optical networking] market share, that really is not a sustainable business given the [companies'] overhead expenses," says Schwerin.

However Jimmy Yu, vice president of optical transport research at Dell’Oro Group, believes there is a role for generalist and specialist systems suppliers, and that market share is not the only indicator of a company's economic health. “You have a few vendors that are healthy and have a good share of the market,” he says. “That said, when I look at some of these [smaller] vendors, I say they are better off.”

Yu cites the likes of ADVA Optical Networking and Transmode, both small players with less than 3 percent market share but they are some of the most profitable system companies with gross margins typically above 40 percent. “Do I think they are going to be around? Yes. They are both healthy and investing as needed.”

Innovation

Equipment makers are also acquiring specialist component players. Cisco Systems acquired coherent receiver specialist CoreOptics in 2010 and more recently silicon photonics player, Lightwire. Meanwhile Huawei acquired photonic integration specialist, CIP Technologies in January 2012. "This is to acquire strategic technologies, not for revenues but to differentiate and reduce the cost of their products," says Perrin.

"There is a problem with the rate of innovation coming from the component vendors," adds Inniss. This is not a failing of the component vendors as innovation has to come from the system vendors: a device will only be embraced by equipment vendors if it is needed and available in time.

Inniss also highlights the changing nature of the market where optical networking and the carriers are just one part. This includes enterprises, cloud computing and the growing importance of content service providers such as Google, Facebook and Amazon who buy components and gear. "It is a much bigger picture than just looking at optical networking," says Inniss.

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

Daryl Inniss, Ovum

Huawei is one system vendor targeting these broader markets, from components to switches, from consumer to the data centre core. Huawei has transformed itself from a follower to a leader in certain areas, while fellow Chinese vendor ZTE is also getting stronger and gaining market share.

Moreover, a consequence of these leading system vendors is that it will fuel the emergence of Chinese optical component players. At present the Chinese optical component players are followers but Inniss expects this to change over the next 3-5 years, as it has at the system level.

Perrin also notes Huawei's huge emphasis on the enterprise and IT markets but highlights several challenges.

The content service providers may be a market but it is not as big an opportunity as traditional telecom. "It is also tricky for the systems providers to navigate as you really can't build all your product line to fit Google's specs and still expect to sell to a BT or an AT&T," says Perrin. That said, systems companies have to go after every opportunity they can because telecom has slowed globally so significantly, he says.

Inniss expects the big optical component players to start to distance themselves, although this does not mean their figures will improve significantly.

"This market is what it is - they [component players] will continue to have 35 percent gross margins and that is the ceiling," says Inniss. But if players want to improve their margins, they will have to invest and grow their presence in markets outside of telecom.

"I like the idea of a Cisco or a Huawei acquiring technology to use internally as a way to differentiate and innovate, and we are going to see more of that," says Perrin.

Thus the supply chain is changing, say the analysts, albeit in a gradual way; not the radical change that Capella's Schwerin suggests is coming.

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen," says Perrin. "I just don't see why there is some catalyst that suggests it is going to be different to the past two years."

This is based on an article that appears in the Optical Connections magazine for ECOC 2012

60-second interview with .... Dell'Oro's Jimmy Yu

"For the year, it is going to be a fivefold growth rate [for 100 Gig transport]."

Jimmy Yu, Dell'Oro

Q: That fact that the market is down 5 percent on a year ago. Why is this?

A: There are a few factors. First, the macro-economy in Europe continues to get worse; that causes a slowdown.

A second factor is that in North America there was a decline in the second quarter, which is pretty unusual. Part of it, we think, might be that operators have caught up with a lot of the spending to increase broadband, after adding [to the network] for a couple of good years.

The third issue is that the China market has had a really slow start. And while there has been talk about the Chinese market softening, it seems that the CapEx [capital expenditure] is there for a strong second half.

What categories does Dell'Oro include when it talks about optical transport?

There are two main pieces: WDM [wavelength division multiplexing], both metro and long haul, and the multi-service multiplexer used for aggregation. The third piece, which is really small, is optical switching - optical cross-connect used in the core and lately more so in the metro.

According to Dell'Oro, wavelength division multiplexing was up 5 percent in the first half of 2012 compared to the same period a year ago, due to demand for 40 Gig and 100 Gig. What is happening in these two markets?

At 100 Gig we are at an inflection point where demand growth rates are really high. We've got a doubling in demand and shipments quarter-on-quarter [in the second quarter]. For the year, it is going to be a fivefold growth rate.

Also the 40 Gig is still growing. It has been around for a few years so its growth rate is not as strong [as 100 Gig transport] but it is still a significant part of the market.

Has the market settled on particular modulation scheme, especially at 40 Gig?

For 100 Gig the majority [deployed] is coherent. There is one company at least, ADVA Optical Networking, which is coming out with its direct-detection scheme for 100 Gig. This has now been shipping for one quarter. There is a market for the price point and the lower-span link of direct-detection.

For 40 Gig there is still a mix of modulations. Vendors coming out with 100 Gig coherent are also coming out with 40 Gig coherent options. So coherent at 40 Gig is now approaching half of the total market and is happening pretty quickly.

As for [40 Gig] DQPSK [differential quadrature phase-shift keying] modulation, it is probably a little bit more than DPSK [differential phase-shift keying].

You also report a rise in the adoption of optical packet products and that it contributed close to one-third of the optical market revenues in the first half 2012. Why is that?

The optical packet platform is a wider definition than just packet optical transport systems (P-OTS).

One reason why optical packet is growing is that with traditional P-OTS, you have cross-connect and switching capabilities in a WDM system so as you go to higher 40 and 100 Gig wavelengths you want some bandwidth management in that system.

Another thing is that people are trying to make the aggregation layer - the traditional SONET/SDH - more Ethernet friendly and MPLS-TP [multiprotocol label switching, transport profile] is gaining traction.

Combined, we are seeing this optical packet market has grown 12 percent year-on-year in the second quarter whereas the overall market has declined.

Dell'Oro said Huawei has 20 percent market share, which other vendors have double-digit market share?

Besides Huawei, the other vendors with double-digit percentage for the quarter - in order - are ZTE, Alcatel-Lucent and Ciena.

Did you see anything in this latest study that was surprising?

There was nothing in this quarter but I saw it last quarter. The legacy equipment – traditional SONET/SDH – is declining. Most of the market decline for optical is in legacy.

SONET/SDH sales in the second quarter of 2012 declined by 20 percent year-on-year. It is finally happening: the market is shifting away from SONET/SDH.

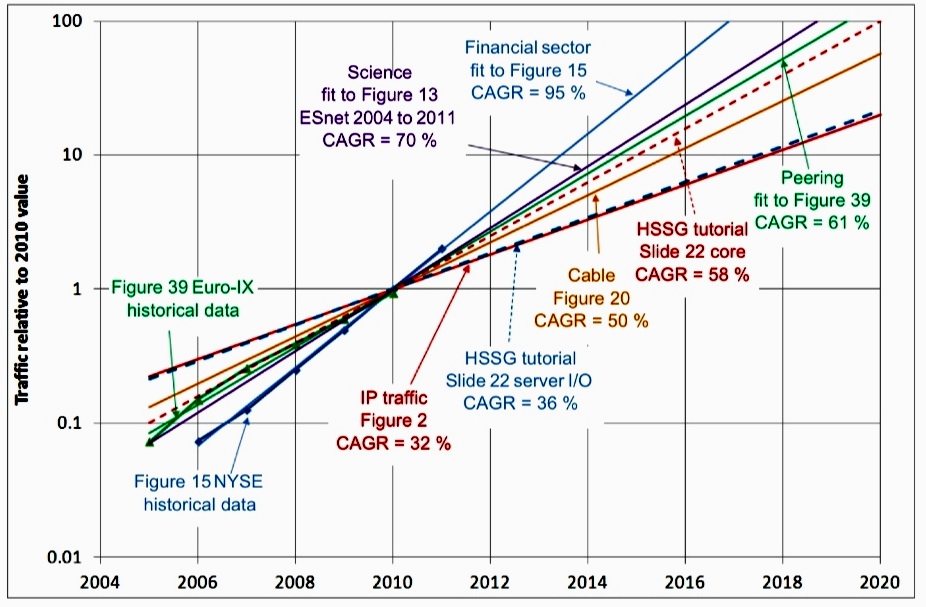

The uphill battle to keep pace with bandwidth demand

Relative traffic increase normalised to 2010 Source: IEEE

Relative traffic increase normalised to 2010 Source: IEEE

Optical component and system vendors will be increasingly challenged to meet the expected growth in bandwidth demand.

According to a recent comprehensive study by the IEEE (The IEEE 802.3 Industry Connections Ethernet Bandwidth Assessment report), bandwidth requirements are set to grow 10x by 2015 compared to demand in 2010, and a further 10x between 2015 and 2020. Meanwhile, the technical challenges are growing for the vendors developing optical transmission equipment and short-reach high-speed optical interfaces.

Fibre bandwidth is becoming a scarce commodity and various techniques will be required to scale capacity in metro and long-haul networks. The IEEE is expected to develop the next-higher speed Ethernet standard to follow 100 Gigabit Ethernet (GbE) in 2017 only. The IEEE is only talking about capacities and not interface speeds. Yet, at this early stage, 400 Gigabit Ethernet looks the most likely interface.

"The various end-user markets need technology that scales with their bandwidth demands and does so economically. The fact that vendors must work harder to keep scaling bandwidth is not what they want to hear"

A 400GbE interface will comprise multiple parallel lanes, requiring the use of optical integration. A 400GbE interface may also embrace modulation techniques, further adding to the size, complexity and cost of such an interface. And to achieve a Terabit, three such interfaces will be needed.

All these factors are conspiring against what the various end-user bandwidth sectors require: line-side and client-side interfaces that scale economically with bandwidth demand. Instead, optical components, optical module and systems suppliers will have to invest heavily to develop more complex solutions in the hope of matching the relentless bandwidth demand.

The IEEE 802.3 Bandwidth Assessment Ad Hoc group, which produced the report that highlights the hundredfold growth in bandwidth demand between 2010 and 2020, studied several sectors besides core networking and data centre equipment such as servers. These include Internet exchanges, high-performance computing, cable operators (MSOs) and the scientific community.

The difference growth rates in bandwidth demand it found for the various sectors are shown in the chart above.

Optical transport

A key challenge for optical transport is that fibre spectrum is becoming a precious commodity. Scaling capacity will require much more efficient use of spectrum.

To this aim, vendors are embracing advanced modulation schemes, signal processing and complex ASIC designs. The use of such technologies also raises new challenges such as moving away from a rigid spectrum grid, requiring the introduction of flexible-grid switching elements within the network.

And it does not stop there.

Already considerable development work is underway to use multi-carriers - super-channels - whose carrier count can be adapted on-the-fly depending on demand, and which can be crammed together to save spectrum. This requires advanced waveform shaping based on either coherent orthogonal frequency division multiplexing (OFDM) or Nyquist WDM, adding further complexity to the ASIC design.

At present, a single light path can be increased from 100 Gigabit-per-second (Gbps) to 200Gbps using the 16-QAM amplitude modulation scheme. Two such light paths give a 400Gbps data rate. But 400Gbps requires more spectrum than the standard 50GHz band used for 100Gbps transmission. And using QAM reduces the overall optical transmission reach achieved.

The shorter resulting reach using 16-QAM or 64-QAM may be sufficient for metro networks (~1000km) but to achieve long-haul and ultra-long-haul spans will require super-channels based on multiple dual-polarisation, quadrature phase-shift keying (DP-QPSK) modulated carriers, each occupying 50GHz. Building up a 400Gbps or 1 Terabit signal this way uses 4 or 10 such carriers, respectively - a lot of spectrum. Some 8Tbps to 8.8Tbps long-haul capacity result using this approach.

The main 100Gbps system vendors have demonstrated 400Gbps using 16-QAM and two carriers. This doubles system capacity to 16-17.6Tbps. A further 30% saving in bandwidth using spectral shaping at the transmitter crams the carriers closer together, raising the capacity to some 23Tbps. The eventual adoption of coherent OFDM or Nyquist WDM will further boost overall fibre capacity across the C-band. But the overall tradeoff of capacity versus reach still remains.

Optical transport thus has a set of techniques to improve the amount of traffic it can carry. But it is not at a pace that matches the relentless exponential growth in bandwidth demand.

After spectral shaping, even more complex solutions will be needed. These include extending transmission beyond the C-band, and developing exotic fibres. But these are developments for the next decade or two and will require considerable investment.

The various end-user markets need technology that scales with their bandwidth demands and does so economically. The fact that vendors must work harder to keep scaling bandwidth is not what they want to hear.

"No-one is talking about a potential bandwidth crunch but if it is to be avoided, greater investment in the key technologies will be needed. This will raise its own industry challenges. But nothing like those to be expected if the gap between bandwidth demand and available solutions grows"

Higher-speed Ethernet

The IEEE's Bandwidth Assessment study lays the groundwork for the development of the next higher-speed Ethernet standard.

Since the standard work has not yet started, the IEEE stresses that it is premature to discuss interface speeds. But based on the state of the industry, 400GbE already looks the most likely solution as the next speed hike after 100GbE. Adopting 400GbE, several approaches could be pursued:

- 16 lanes at 25Gbps: 100GbE is moving to a 4x25Gbps electrical interface and 400GbE could exploit such technology for a 16-lane solution, made up of four, 4x25Gbps interfaces. "If I was a betting man, I'd probably put better odds on that [25Gbps lanes] because it is in the realm of what everyone is developing," John D'Ambrosia, chair of the IEEE 802.3 Industry Connections Higher Speed Ethernet Consensus group and chair of the the IEEE 802.3 Bandwidth Assessment Ad Hoc group, told Gazettabyte.

- 10 lanes at 40Gbps: The Optical Internetworking Forum (OIF) has started work on an electrical interface operating between 39 and 56Gbps (Common Electrical Interface - 56G-Close Proximity Reach). This could lead to 40Gbps lanes and a 10x40Gbps implementation for a 400Gbps Ethernet design.

- Modulation: For the 100Gbps backplane initiative, the IEEE is working on pulse-amplitude modulation (PAM), says D'Ambrosia. Such modulation could be used for 400GbE. Modulation is also being considered by the IEEE to create a single-lane 100Gbps interface. Such a solution could lead to a 4-lane 400GbE solution. But adopting modulation comes at a cost: more sophisticated electronics, greater size and power consumption.

As with any emerging standard, first designs will be large, power-hungry and expensive. The industry will have to work hard to produce more integrated 16-lane or 10-lane designs. Size and cost will also be important given that three 400GbE modules will be needed to implement a Terabit interface.

The challenge for component and module vendors is to develop such multi-lane designs yet do so economically. This will require design ingenuity and optical integration expertise.

Timescales

Super-channels exist now - Infinera is shipping its 5x100Gbps photonic integrated circuit. Ciena and Alcatel-Lucent are introducing their latest generation DSP-ASICs that promise 400Gbps signals and spectral shaping while other vendors have demonstrated such capabilities in the lab.

The next Ethernet standard is set for completion in 2017. If it is indeed based on a 400GbE Ethernet interface, it will likely use 4x25Gbps components for the first design, benefiting from emerging 100GbE CFP2 and CFP4 modules and their more integrated designs. But given the standard will only be completed in five years' time, new developments should also be expected.

No-one is talking about a potential bandwidth crunch but if it is to be avoided, greater investment in the key technologies will be needed. This will raise its own industry challenges. But nothing like those to be expected if the gap between bandwidth demand and available solutions grows.

The next high-speed Ethernet standard starts to take shape

Source: Gazettabyte

Source: Gazettabyte

The IEEE has begun work to develop the next-speed Ethernet standard beyond 100 Gigabit to address significant predicted growth in bandwidth demand.

The standards body has set up the IEEE 802.3 Industry Connections Higher Speed Ethernet Consensus group, chaired by John D’Ambrosia, who previously chaired the 40 and 100 Gigabit IEEE P802.3ba Ethernet standards ratified in June 2010. "I guess I’m a glutton for punishment,” quips D'Ambrosia.

The Higher Speed Ethernet standard could be completed by early 2017.

The group has been set up after an extensive one-year study by the IEEE 802.3 Bandwidth Assessment Ad Hoc group investigating networking capacity growth trends in various markets. The study looked beyond core networking and data centres - the focus of the 40 and 100 Gigabit Ethernet (GbE) study work - to include high-performance computing, financial markets, Internet exchanges and the scientific community.

One of the resulting report's conclusions (IEEE 802.3 Industry Connections Ethernet Bandwidth Assessment report) is that Terabit capacity will likely be required by 2015, growing a further tenfold by 2020.

“By 2015 core networks on average will need ten times the bandwidth of 2010, and one hundred times [the bandwidth] by 2020,” says D’Ambrosia, who is also the chair of the IEEE 802.3 Ethernet Bandwidth Assessment Ad Hoc group, as well as chief Ethernet evangelist, CTO office at Dell. “If you look at Ethernet in 2010, it was at 100 Gigabit, so ten times 100 Gigabit in 2015 is a Terabit and a hundred times 2010 is 10 Terabit by 2020.”

"We have got to the point where the pesky laws of physics are challenging us"

John D'Ambrosia, chair of the IEEE 802.3 Industry Connections Higher Speed Ethernet Consensus group

D'Ambrosia stresses that the Ad Hoc group's role is to talk about capacity requirements, not interface speeds. The technical details of any interface implementation will only become clear once the standardisation effort is well under way.

A second Ethernet Bandwidth Assessment study finding is that network aggregation nodes are growing faster, and hence require greater capacity earlier, than the network's end points.

"There is also a growing deviation between the big guys and the rest of the market," says D'Ambrosia. He has heard individuals from the largest internet content providers say they need Terabit connections by 2013, while others claim it will be 2020 before a mass market develops for such an interconnect.

D'Ambrosia says the main findings are not necessarily surprising but there were two 'aha' moments during the study.

One was that the core networking growth rates predicted in 2007 by the 40 and 100 Gig High-speed Study Group are still valid five years on.

The other concerned the New York Stock Exchange that had forecast that it would need to install four 100Gbps links in its data centre yet ended up using 13. "If there is any company that has a lot of money on the line and would have the best chance of nailing down their needs, I would put the New York Stock Exchange up there," says D'Ambrosia. "That tells you something about bandwidth growth and that you can still underestimate what is going to happen."

"The reality is that I can't give you any solutions right now that are attractive to do a Terabit"

What next

The IEEE standardisation work for the next speed Ethernet has not started but the completed Ethernet Bandwidth Assessment study will likely form an important input for the Industry Connections Higher Speed Ethernet Consensus group.

The start of the standardisation work is expected in either March or July 2013 with the Study Group phase then taking a further eight months. This compares to 18 months for the IEEE 40GbE and 100GbE Study Group work (see chart above). The Task Force's work - writing the specification - is then expected to take a further two and a half years, completing the standard in early 2017 if all goes to plan.

Technology options

While stressing that the IEEE is talking about capacities and not yet interface speeds, Terabit capacity could be solved using multiple 400 Gigabit Ethernet interfaces, says D'Ambrosia.

At present there is no 400GbE project underway. However, the industry does believe that 400GbE is "doable" economically and technically. "Much of the supply base, when we are talking about Ethernet, is looking at 400 Gigabit," says D'Ambrosia.

Achieving a 1TbE interface looks much more distant. "People pushing for 1 Terabit tend to be the people looking at it from the bandwidth perspective and then looking at upgrading their networks and making multiple investments," he says. "But the reality is that I can't give you any solutions right now that are attractive to do a Terabit."

All agree that the technical challenges facing the industry to meet growing bandwidth demands are starting to mount. "We have got to the point where the pesky laws of physics are challenging us," says D'Ambrosia.

Further reading:

IEEE 802.3 Industry Connections Higher Speed Ethernet Ad Hoc

Briefing: Flexible elastic-bandwidth networks

Vendors and service providers are implementing the first examples of flexible, elastic-bandwidth networks. Infinera and Microsoft detailed one such network at the Layer123 Terabit Optical and Data Networking conference held earlier this year.

Optical networking expert Ioannis Tomkos of the Athens Information Technology Center explains what is flexible, elastic bandwidth.

Part 1: Flexible elastic bandwidth

"We cannot design anymore optical networks assuming that the available fibre capacity is abundant"

Prof. Tomkos

Several developments are driving the evolution of optical networking. One is the incessant demand for bandwidth to cope with the 30+% annual growth in IP traffic. Another is the changing nature of the traffic due to new services such as video, mobile broadband and cloud computing.

"The characteristics of traffic are changing: A higher peak-to-average ratio during the day, more symmetric traffic, and the need to support higher quality-of-service traffic than in the past," says Professor Ioannis Tomkos of the Athens Information Technology Center.

"The growth of internet traffic will require core network interfaces to migrate from the current 10, 40 and 100Gbps to 1 Terabit by 2018-2020"

Operators want a more flexible infrastructure that can adapt to meet these changes, hence their interest in flexible elastic-bandwidth networks. The operators also want to grow bandwidth as required while making best use of the fibre's spectrum. They also require more advanced control plane technology to restore the network elegantly and promptly following a fault, and to simplify the provisioning of bandwidth.

The growth of internet traffic will require core network interfaces to migrate from the current 10, 40 and 100Gbps to 1 Terabit by 2018-2020, says Tomkos. Such bit-rates must be supported with very high spectral efficiencies, which according to latest demonstrations are only a factor of 2 away of the Shannon's limit. Simply put, optical fibre is rapidly approaching its maximum limit.

"We cannot design anymore optical networks assuming that the available fibre capacity is abundant," says Tomkos. "As is the case in wireless networks where the available wireless spectrum/ bandwidth is a scarce resource, the future optical communication systems and networks should become flexible in order to accommodate more efficiently the envisioned shortage of available bandwidth.”

The attraction of multi-carrier schemes and advanced modulation formats is the prospect of operators modifying capacity in a flexible and elastic way based on varying traffic demands, while maintaining cost-effective transport.

Elastic elements

Optical systems providers now realise they can no longer keep increasing a light path's data rate while expecting the signal to still fit in the standard International Telecommunication Union (ITU) - defined 50GHz band.

It may still be possible to fit a 200 Gigabit-per-second (Gbps) light path in a 50GHz channel but not a 400Gbps or 1 Terabit signal. At 400Gbps, 80GHz is needed and at 1 Terabit it rises to 170GHz, says Tomkos. This requires networks to move away from the standard ITU grid to a flexible-based one, especially if operators want to achieve the highest possible spectral efficiency.

Vendors can increase the data rate of a carrier signal by using more advanced modulation schemes than dual polarisation, quadrature phase-shift keying (DP-QPSK), the defacto 100Gbps standard. Such schemes include amplitude modulation at 16-QAM, 64-QAM and 256-QAM but the greater the amplitude levels used and hence the data rates, the shorter the resulting reach.

Another technique vendors are using to achieve 400Gbps and 1Tbps data rates is to move from a single carrier to multiple carriers or 'super-channels'. Such an approach boosts the data rate by encoding data on more than one carrier and avoids the loss in reach associated with higher order QAM. But this comes at a cost: using multiple carriers consumes more, precious spectrum.

As a result, vendors are looking at schemes to pack the carriers closely together. One is spectral shaping. Tomkos also details the growing interest in such schemes as optical orthogonal frequency division multiplexing (OFDM) and Nyquist WDM. For Nyquist WDM, the subcarriers are spectrally shaped so that they occupy a bandwidth close or equal to the Nyquist limit to avoid inter symbol interference and crosstalk during transmission.

Both approaches have their pros and cons, says Tomkos, but they promise optimum spectral efficiency of 2N bits-per-second-per-Hertz (2N bits/s/Hz), where N is the number of constellation points.

The attraction of these techniques - multi-carrier schemes and advanced modulation formats - is the prospect of operators modifying capacity in a flexible and elastic way based on varying traffic demands, while maintaining cost-effective transport.

"With flexible networks, we are not just talking about the introduction of super-channels, and with it the flexible grid," says Tomkos. "We are also talking about the possibility to change either dynamically."

According to Tomkos, vendors such as Infinera with its 5x100Gbps super-channel photonic integrated circuit (PIC) are making an important first step towards flexible, elastic-bandwidth networks. But for true elastic networks, a flexible grid is needed as is the ability to change the number of carriers on-the-fly.

"Once we have those introduced, in order to get to 1 Terabit, then you can think about playing with such parameters as modulation levels and the number of carriers, to make the bandwidth really elastic, according to the connections' requirements," he says.

Meanwhile, there are still technology advances needed before an elastic-bandwidth network is achieved, such as software-defined transponders and a new advanced control plane.

Tomkos says that operators are now using control plane technology that co-ordinates between layer three and the optical layer to reduce network restoration time from minutes to seconds. Microsoft and Infinera cite that they have gone from tens of minutes down to a few seconds using the more advanced optical infrastructure. "They [Microsoft] are very happy with it," says Tomkos.

But to provision new capacity at the optical layer, operators are talking about requirements in the tens of minutes; something they do not expect will change in the coming years. "Cloud services could speed up this timeframe," says Tomkos.

"There is usually a big lag between what operators and vendors do and what academics do," says Tomkos. "But for the topic of flexible, elastic networking, the lag between academics and the vendors has become very small."

Further reading:

AppliedMicro samples 100Gbps CMOS multiplexer

AppliedMicro has announced the first CMOS merchant multiplexer chip for 100Gbps coherent optical transmission. The S28032 device supports dual polarisation, quadrature phase-shift keying (DP-QPSK) and has a power consumption of 4W, half that of current multiplexer chip designs implemented in BiCMOS.

The S28032 100 Gig multiplexer IC. Source: AppliedMicro

The S28032 100 Gig multiplexer IC. Source: AppliedMicro

"CMOS has a very low gain-bandwidth product, typically 100GHz," says Tim Warland, product marketing manager, connectivity solutions at AppliedMicro. “Running at 32GHz, we have been able to achieve a very high bandwidth with CMOS."

Significance

The availability of a CMOS merchant device will be welcome news for optical transport suppliers and 100Gbps coherent module makers. CMOS has better economics than BiCMOS due to the larger silicon wafers used and the chip yields achieved. The reduced power consumption also promotes the move to smaller-sized optical modules than the current 5x7-inch multi-source agreement (MSA).

"By reducing the power and the size, we can get to a 4x6-inch next-generation module,” says Warland. “And perhaps if we go for a shorter [optical transmission] reach - 400-600km - we could get into a CFP; then you can get four modules on a card.”

"Coherent ultimately is the solution people want to go to [in the metro] but optical duo-binary will do just fine for now"

Tim Warland, AppliedMicro

Chip details

The S28032 has a CAUI interface: 10x12Gbps input lanes that are multiplexed into four lanes at 28Gbps to 32Gbps. The particular data rate depends on the forward error correction (FEC) scheme used. The four lanes are DQPSK-precoded before being fed to the polarisation multiplexer to create the DP-QPSK waveforms.

The device also supports the SFI-S interface - 21 input channels, each at 6Gbps. This is significant as it enables the S28032 to be interfaced to NTT Electronics' (NEL) DSP-ASIC coherent receiver chip that has been adopted by 100Gbps module makers Oclaro and Opnext (now merged) as well as system vendors including Fujitsu Optical Systems and NEC.

The mux IC within a 100Gbps coherent 5x7-inch optical module. Source: AppliedMicro

The mux IC within a 100Gbps coherent 5x7-inch optical module. Source: AppliedMicro

The AppliedMicro multiplexer IC, which is on the transmit path, interfaces with NEL's DSP-ASIC that is on the receiver path, because the FEC needs to be a closed loop to achieve the best efficiency, says Warland. "If you know what you are transmitting and receiving, you can improve the gain and modify the coherent receiver sampling points if you know what the transmit path looks like," he says.

The DSP-ASIC creates the transmission payloads and uses the S28032 to multiplex those into 28Gbps or greater speed signals.

The SFI-S interface is also suited to interface to FPGAs, for those system vendors that have their own custom FPGA-based FEC designs.

"Packet optical transport systems is more a potential growth engine as the OTN network evolves to become a real network like SONET used to be"

Francesco Caggioni. AppliedMicro

The multiplexer chip's particular lane rate is set by the strength of the FEC code used and its associated overhead. Using OTU4 frames with its 7% overhead FEC, the resulting data rate is 27.95Gbps. With a stronger 15% hard-decision FEC, each of the 4 channel's data rate is 30Gbps while it is 31.79Gbps with soft-decision FEC.

"It [the chip] has got sufficient headroom to accommodate everything that is available today and that we are considering in the OIF [Optical Internetworking Forum],” says Warland. The multiplexer is expected to be suitable for coherent designs that achieve a reach of up to 2,000-2,500km but the sweet spot is likely to be for metro networks with a reach of up to 1,000km, he says.

But while the CMOS device can achieve 32Gbps, it has its limitations. "For ultra long haul, we can't support a FEC rate higher than 20%," says Warland. "For that, a 25% to 30% FEC is needed."

AppliedMicro is sampling the device to lead customers and will start production in 1Q 2013.

What next

The S28032 joins AppliedMicro's existing S28010 IC suited for the 10km 100 Gigabit Ethernet 100GBASE-LR4 standard, and for optical duo-binary 100Gbps direct detection that has a reach of 200-1,000km.

"Our next step is to try and get a receiver to match this chip," says Warland. But it will be different to NEL's coherent receiver: "NEL's is long haul." Instead, AppliedMicro is eyeing the metro market where a smaller, less power-hungry chip is needed.

"Coherent ultimately is the solution people want to go to [in the metro] but optical duo-binary will do just fine for now," says Warland.

Two million 10Gbps OTN ports

AppliedMicro has also announced that it has shipped 2M 10Gbps OTN silicon ports. This comes 18 months after it announced that it had shipped its first million.

"OTN is showing similar growth to the 10 Gigabit Ethernet market but with a four-year lag," says Francesco Caggioni, strategic marketing director, connectivity solutions at AppliedMicro.

The company sees OTN growth in the IP edge router market and for transponder and muxponder designs, while packet optical transport systems (P-OTS) is an emerging market.

"Packet optical transport systems is more a potential growth engine as the OTN network evolves to become a real network like SONET used to be," says Caggioni. "We are seeing development but not a lot of deployment."

Further reading:

Cortina unveils multi-channel dispersion compensation chip

Cortina Systems has announced its latest electronic dispersion compensation (EDC) chip. The CS4342 is a compact device that supports eight duplex 10 Gigabit-per-second (Gbps) links.

"Some customers are doing 2,000 signals at 10 Gig across the backplane"

Scott Feller, Cortina

The chip is suited for use with optical modules and on line cards to counter the effect of transmission distortion where a bit's energy leaks into one or more adjacent bits, known as inter-symbol interference (ISI).

The Cortina device can be used for 10, 40 and 100Gbps line card and backplane designs and supports copper cable and optical fibre standards such as the multimode 10GBASE‐LRM and the 80km 10GBASE‐ZR interface.

Significance

Routeing high-speed signals from an ASIC to the various high-speed interfaces - 10Gbps and greater - is becoming harder as more interfaces are crammed onto a card.

"Boards are getting denser: from 48 ports to 96," says Scott Feller, director of the EDC product line at Cortina Systems. The issue with an ASIC on the board is that the distance it can span to the modules is only about 6-8 inches (~15-20cm). Placing the PHY chip on the board relaxes this constraint.

The use of the octal EDC chip between a line card IC and SFP+ optical transceivers. Source: Cortina Systems

The use of the octal EDC chip between a line card IC and SFP+ optical transceivers. Source: Cortina Systems

Vendors also gain greater flexibility in terms of the interfaces they can support. "These types of PHYs allow them [designers] to avoid having to make hard decisions," says Feller. "They put the PHY in front of the optical connector and they almost get every single optical format on the market."

The platforms using such EDC PHYs include data centre switches and telecom platforms such as packet optical transport systems (P-OTS). Data centre switches typically support Direct Attach Copper cable - a market area that has been growing significantly, says Cortina - and short-reach optical interfaces. For P-OTS the interfaces include the 10GBASE-ZR where EDC is a necessity.

The device is also being used for system backplanes where bandwidth requirements are increasing significantly. "Some customers are doing 2,000 signals at 10 Gig across the backplane," says Feller. "Now that there are so many signals - so much crosstalk - and the ASICs are further away from the backplane, so PHYs are starting to be put into systems."

EDC employed in a backplane design. Source: Cortina Systems

EDC employed in a backplane design. Source: Cortina Systems

Chip details

Cortina claims the 17x17 ball grid array CS4342 is a third smaller than competing devices. The chip compensates the received signal in the analogue domain. An on-chip DSP calculates the filter's weights to counter ISI while the filtering is performed using analogue circuitry. As a result, the EDC has a latency of 1ns only.

Cortina has dual, quad and now octal EDC ICs. It says that the delay between the different devices is the same such that both an octal and dual chip can be used to implement a 10-channel 100 Gig interface, for example the 10x10 MSA. In turn, future line cards supporting four 100Gbps interfaces would use five octal PHYs ICs.

The CS4342 is available in sample form and will enter production from October.

What next

"This type of product is at the very end of the food chain so there is always macro developments that could change the market," says Feller. Silicon photonics is one but Feller expects that it will be years before the technology is adopted widely in systems.

The external EDC PHYs must also compete with PHYs integrated within custom ASIC designs and FPGAs. "We always have to be ahead of the cost and performance curves on the PHY," says Feller. "If not, they [companies] are just going to integrate PHYs into their ASICs and FPGAs."

Meanwhile, Cortina says it has two more EDC devices in development.