100 Gigabit 'unstoppable'

A Q&A with Andrew Schmitt (@aschmitt), directing analyst for optical at Infonetics Research.

"40Gbps has even less value in the metro than in the core"

Andrew Schmitt, Infonetics Research

A study from market research firm, Infonetics Research, has found that operators have a strong preference for deploying 100 Gigabit-per-second (Gbps) technology as they upgrade their networks.

Infonetics interviewed 21 incumbent service providers, competitive operators and mobile operators that have either 40Gbps, 100Gbps or both wavelength types installed in their networks, or that plan to install by next year (2013).

The operators surveyed, from all the major regions, account for over a quarter (28%) of worldwide telecom carrier revenue and capital expenditure.

The study's findings include:

- A strong preference by the carriers for 100Gbps transport in both Brownfield and Greenfield installations. Carriers will use 40 and 100Gbps to the same degree in existing Brownfield networks while favouring 100Gbps for new, Greenfield builds.

- The reasons to deploy 40Gbps and 100Gbps optical transport equipment include lowering the cost per bit, taking advantage of the superior dispersion performance of coherent optics, and lowering incremental common equipment costs due to the increased spectral efficiency.

- Most respondents indicate 40Gbps is only a short-term solution and will move the majority of installations to 100Gbps once those products become widely available.

- Non-coherent 100Gbps is not yet viewed as an important technology.

- Colourless and directionless ROADMs and Optical Transport Network (OTN) switching are important components of Greenfield builds; gridless and contentionless ROADMs are much less so.

Q&A with Andrew Schmitt

Q. A key finding is that 40Gbps and 100Gbps are equally favoured for Brownfield routes. And is it correct that Brownfield refers to existing routes carrying 10Gbps and maybe 40Gbps wavelengths while Greenfield involves new 100Gbps wavelengths? What is it about Brownfield that 40Gbps and 100Gbps have equal footing? Equally, for Greenfield, is the thinking: "If we are deploying a new lit fibre, we might as well start with the newest and fastest"?

A: The assumptions on Brownfield versus Greenfield are correct, the definitions in the survey and the report are more detailed but that is right.

It is more an issue that they [carriers] are building with 40Gbps now but will transition to 100Gbps where it can be used. Where it can't be used they stick with 40Gbps. There are many reasons why 100Gbps may not work in existing networks.

Q: Another finding is that 40Gbps is seen as a short-term solution. What is short term? And will that also be true for the metro or does metro have its own dynamic?

A: We didn't test timing explicitly for Greenfield versus Brownfield networks. It [40Gbps] doesn't necessarily peak, it is just not growing at the same rate as 100Gbps. And 40Gbps has even less value in the metro than in the core, particularly in Greenfield builds. With Greenfield 100Gbps combined with soft-decision forward error correction (SD-FEC), it is almost as good as 40Gbps.

Q: The study found that non-coherent 100Gbps isn't yet viewed as an important technology. Why do you think that is so? And what is your take on the non-coherent 100Gbps opportunity?

A: The jury is still out.

The large customers I spoke with haven't looked at it and therefore can't form an opinion. A lot of promises and marketing at this point but that doesn't mean it won't work. Module vendors are pretty excited about it and they aren't stupid.

Q: You say colourless and directionless is seen as important ROADM attributes, gridless and contentionless much less so. If operators are building 100Gbps Greenfield overlays, is not gridless a must to future-proof the network investment?

A: The gridless requirement is completely overblown and folks positioning it as a requirement today haven't done the work to understand the issues trying to use it today. This survey was even more negative than I expected.

Reflections 2011, Predictions 2012 - Part 2

Gazettabyte asked industry analysts, CEOs, executives and commentators to reflect on the last year and comment on developments they most anticipate for 2012. Here are the views of Verizon's Glenn Wellbrock, Professor Rod Tucker, Ciena's Joe Berthold, Opnext's Jon Anderson, NeoPhotonics' Tim Jenks and Vladimir Kozlov of LightCounting.

Glenn Wellbrock, Verizon's director of optical transport network architecture & design

The most significant accomplishment from an optical transport perspective for me was the introduction of 100 Gigabit into Verizon's domestic - US - network.

"The key technology enabler in 2012 will be the flexible grid optical switching that can support data rates beyond 100 Gigabit"

That accomplishment has paved the way for us to hit the ground running in 2012 with a very aggressive 100 Gigabit deployment plan. I also believe this accomplishment gives others the confidence to start taking advantage of this leading-edge technology.

With coherent receiver technology and the associated high-speed electronics lowering the propagation latency by up to 15%, we see a much cleaner line system design that eliminates external dispersion compensation fibre while bringing down the cost, space and power per bit.

The value of the whole industry moving in this direction means higher volumes and, therefore, lower costs. This new infrastructure will allow operators to get ahead of customer demand, thus improving delivery intervals and introducing new, higher bandwidth services to those large key customers that require it.

In my opinion, the key technology enabler in 2012 will be the flexible grid optical switching that can support data rates beyond 100 Gigabit and provides the framework to support colourless, directionless and contentionless optical nodes.

Today, field technicians must plug a new transmitter/ receiver into the appropriate direction and filter port at both circuit ends. With this new technology, operations personnel can simply plug the new card into the next available port and it can then be provisioned, tested and even moved to a new colour or direction remotely without any on-site personnel involvement - even when there are multiple copies of the same colour on the same add/ drop structure coming from different fibres.

This new nodal architecture takes advantage of the inherent channel selection capability of the coherent receiver to eliminate fixed filters and opens up the door for a truly reconfigurable optical add/ drop multiplexer (ROADM) - creating new flexibility that can be used for optical restoration, network defragmentation, operational simplicity, and more.

Rod Tucker, Director of the Institute for a Broadband Enabled Society (IBES), Director of the Centre for Energy-Efficient Telecommunications (CEET), and professor of electrical and electronic engineering at the University of Melbourne.

Australia's National Broadband Network (NBN) hit the ground running in 2011.

The project is still many years from completion, but in 2011 the roll-out of fibre-to-the-premises infrastructure began in earnest. This is a very noteworthy project - a wholesale broadband access network delivering advanced broadband services to the entire population of the country, including fibre to 93% of all premises and a mixture of fixed wireless and satellite to the remainder. At an estimated cost of around AUS$36 billion, the price tag is not small.

"The environment created by [Australia's] National Broadband Network will greatly enhance opportunities for innovations in new services and new modes of broadband service delivery"

But the wholesale-only model maximises opportunities for competition at the service provider level, and reduces wasteful duplication of infrastructure in the last mile. A remarkable aspect of the NBN project is that a deal has been struck between the incumbent telco, Telstra, and the government-owned owner of the NBN.

Under this deal, Telstra will shut down its Hybrid-Fibre-Coax (HFC) network and decommission its legacy copper access network. Australia will become a truly fibre-connected country, with a future-proof broadband infrastructure.

My thoughts for 2012 also relate to Australia's National Broadband Network. The environment created by the NBN will greatly enhance opportunities for innovations in new services and new modes of broadband service delivery.

I anticipate that in 2012 and beyond, new services providers and aggregators in areas such as health care, education, entertainment and energy will emerge.

I am very excited about the opportunities.

Joe Berthold, vice president of network architecture at Ciena

One of the most memorable developments from a network architecture point of view was the clear emergence of the category of packet-optical switching products to serve as the transport layer of backbone IP networks.

For years two competing points of view have been put forth. First, in the 'IP-over-glass' position, long-haul optics is incorporated into core routers. This has never taken off, with some disappointing attempts in the early days of 40 Gigabit. The second approach involves a separate, very much simpler, packet optical transport platform being introduced to interconnect core routers. The packet transport could be based on Ethernet protocols, MPLS, MPLS-TE or MPLS-TP.

"It will be interesting to see if a large internet data centre operator decides to embrace the OpenFlow concept at this very early stage of its development"

What is quite significant in this development, traditional router vendors seem to be going in this direction too, with the vision of a much simpler packet switching platform to keep cost, space and power under control.

This is a clear response to the overwhelming need we see in the market, representing a separation of packet switching into two layers: one with global routing capability at strategic locations in the network, and the other with flexible transport functionality for network traffic engineering.

In 2012 it will be fascinating to see how the struggle for protocol dominance plays out within the data centre.

While the IETF has many competing proposals, worked in multiple groups, the IEEE is in final ballot now for Shortest Path Bridging (IEEE 802.1aq).

Shortest Path Bridging has broad applicability in networks, but we might see it first emerge as a solution within the data centre.

The other contender within the data centre is OpenFlow, which has developed quite a momentum too.

It will be interesting to see if a large internet data centre operator decides to embrace the OpenFlow concept at this very early stage of its development.

Jon Anderson, director of technology programme at Opnext

Our most significant 2011 events were the Japan great earthquake in March and the Thailand floods in October. Both events caused major disruptions and challenges in optical component supply-chain management and manufacturing.

JDS Uniphase's tunable SFP+ announcement was well ahead of the technology curve.

"Our most significant 2011 events were the Japan great earthquake in March and the Thailand floods in October."

In 2012 we expect initial production shipments and deployment of 100Gbps PM-QPSK/ coherent modules. Also a fast production ramp of 40 Gigabit Ethernet (GbE) QSFP+ modules for data centre applications.

Another development to watch is the next-generation 100 GbE interconnect technology and standards development for low-cost, high-density modules for data centre applications.

Lastly, there will be an increased focus on technologies and solutions for 100 Gigabit DWDM in metro and extended reach enterprise applications.

Tim Jenks, CEO of NeoPhotonics

NeoPhotonics made significant progress this year in developments of components and technologies for coherent transmission networks, including receivers, transmitters and advanced approaches toward switching.

We continue to see increasing adoption of coherent transmission systems, broad-scale deployment of access networks and a continuing emergence of large scale data centres as a prominent element of the communications network landscape.

Vladimir Kozlov, CEO of LightCounting

The industry was strong enough to get over an earthquake, tsunami and flood in 2011. Softer demand for optics in 2011 helped - is still helping - many vendors to ride the disruptions. Ironically, the industry was more stressed ramping up production in 2010 to meet demand than dealing with the disruptions of 2011. We are looking forward to a smoother ride in 2012, as demand/ supply reach equilibrium and nature cooperates.

"Ironically, the industry was more stressed ramping up production in 2010 to meet demand than dealing with the disruptions of 2011"

"Ironically, the industry was more stressed ramping up production in 2010 to meet demand than dealing with the disruptions of 2011"

Service provider revenue and capex were up significantly in 2011. Mobile data is driving the growth, but even wireline revenues are improving and FTTx is probably behind it. This should be a sustainable trend for 2012-2015, even as service providers curb expenses to improve profitability, a larger fraction of capex will be spend on equipment. New technology is critical to stay ahead of competition.

Data centre optics had another good year with 10GBASE-T falling further behind schedule and with 100 Gigabit generating much action. This will probably get even more interesting in 2012.

Our conservative forecast for active optical cable, criticised by some vendors, was not conservative enough in 2011. It will take a while for this segment to unfold.

For Part 1, click here

For Part 3, click here

ROADMs: core role, modest return for component players

Next-generation reconfigurable optical add/ drop multiplexers (ROADMs) will perform an important role in simplifying network operation but optical component vendors making the core component - the wavelength-selective switch (WSS) - on which such ROADMs will be based should expect a limited return for their efforts.

"[Component suppliers] are going to be under extreme constraints on pricing and cost"

"[Component suppliers] are going to be under extreme constraints on pricing and cost"

Sterling Perrin, Heavy Reading

That is one finding from an upcoming report by market research firm, Heavy Reading, entitled: "The Next-Gen ROADM Opportunity: Forecast & Analysis".

"We do see a growth opportunity [for optical component vendors]," says Sterling Perrin, senior analyst and author of the report. “But in terms of massive pools of money becoming available, it's not going to happen; it is a modest growth in spend that will go to next-generation ROADMs."

That is because operators’ capex spending on optical will grow only in single digits annually while system vendors that supply the next-generation ROADMs will compete fiercely, including using discounting, to win this business. "All of this comes crashing down on the component suppliers, such that they are going to be under extreme constraints on pricing and cost," says Perrin. The report will quantify the market opportunity but Heavy Reading will not discuss numbers until the report is published.

Next-generation ROADMs incorporate such features as colourless (wavelength-independence on an input port), directionless (wavelength routing to any port), contentionless (more than one same-wavelength light path accommodated at a port) and flexible spectrum (variable channel width for signal rates above 100 Gigabit-per-second (Gbps)).

Networks using such ROADMs promise to reduce service providers' operational costs. And coupled with the wide deployment of coherent optical transmission technology, next-generation ROADMs are set to finally deliver agile optical networks.

Other of the report’s findings include the fact that operators have been deploying colourless and directionless ROADMs since 2010, even though implementing such features using current 1x9 WSSs are cumbersome and expensive. However, operators wanting these features in their networks have built such systems with existing components. "Probably about 10% of the market was using colourless and directionless functions in 2010," says Perrin.

Service providers are requiring ROADMs to support flexible spectrum even though networks will likely adopt light paths faster than 100Gbps (400Gbps and beyond) in several years' time.

The need to implement a flexible spectrum scheme will force optical component vendors with microelectromechanical system (MEMS) technology to adopt liquid crystal technology – and liquid-crystal-on-silicon (LCoS) in particular - for their WSSs (see Comments). "MEMS WSS technology is great for all the stuff we do today - colourless, directionless and contentionless - but when you move to flexible spectrum it is not capable of doing that function," says Perrin. "The technology they (vendors with MEMS technology) have set their sights on - and which there is pretty much agreement as the right technology for flexible spectrum - is the liquid crystal on silicon." A shift from MEMS to LCoS for next-generation ROADM technology is thus to be expected, he says.

Perrin also highlights how coherent detection technology, now being installed for 100 Gbps optical transmission, can also implement a colourless ROADM by making use of the tunable nature of the coherent receiver. "It knocks out a bunch of WSSs added to the add/ drop," says Perrin. "It is giving a colourless function for free, which is a huge advantage."

Perrin views next-gen ROADMs as a money-saving exercise for the operators, not a money-making one. "This is hitting on the capex as well as the opex piece which is absolutely critical," he says. "You see the charts of the hockey stick of bandwidth growth and flat venue growth; that is what ROADMS hit at."

The Heavy Reading report will be published later this month.

Further reading:

Intelligent networking: Q&A with Alcatel-Lucent's CTO

Alcatel-Lucent's corporate CTO, Marcus Weldon, in a Q&A with Gazettabyte. Here, in Part 1, he talks about the future of the network, why developing in-house ASICs is important and why Bell Labs is researching quantum computing.

Marcus Weldon (left) with Jonathan Segel, executive director in the corporate CTO Group, holding the lightRadio cube. Photo: Denise Panyik-Dale

Marcus Weldon (left) with Jonathan Segel, executive director in the corporate CTO Group, holding the lightRadio cube. Photo: Denise Panyik-Dale

Q: The last decade has seen the emergence of Asian Pacific players. In Asia, engineers’ wages are lower while the scale of R&D there is hugely impressive. How is Alcatel-Lucent, active across a broad range of telecom segments, ensuring it remains competitive?

A: Obviously we have a Chinese presence ourselves and also in India. It varies by division but probably half of our workforce in R&D is in what you would consider a low-cost country. We are already heavily present in those areas and that speaks to the wage issue.

But we have decided to use the best global talent. This has been a trait of Bell Labs in particular but also of the company. We believe one of our strengths is the global nature of our R&D. We have educational disciplines from different countries, and different expertise and engineering foci etc. Some of the Eastern European nations are very strong in maths, engineering and device design. So if you combine the best of those with the entrepreneurship of the US, you end up with a very strong mix of an R&D population that allows for the greatest degree of innovation.

We have no intention to go further towards a low-cost country model. There was a tendency for that a couple of years ago but we have pulled back as we found that we were losing our innovation potential.

We are happy with the mix we have even though the average salary is higher as a result. And if you take government subsidies into account in European nations, you can get almost the same rate for a European engineer as for a Chinese engineer, as far as Alcatel-Lucent is concerned.

One more thing, Chinese university students, interestingly, work so hard up to getting into university that university is a period where they actually slack off. There are several articles in the media about this. The four years that students spend in university, away from home for the first time, they tend to relax.

Chinese companies were complaining that the quality of engineers out of university was ever decreasing because of what was essentially a slacker generation, they were arguing, of overworked high-school students that relaxed at college. Chinese companies found that they had to retrain these people once employed to bring them to the level needed.

So that is another small effect which you could argue is a benefit of not being in China for some of our R&D.

Alcatel-Lucent's Bell Labs: Can you spotlight noteworthy examples of research work being done?

Certainly the lightRadio cube stuff is pure Bell Labs. The adaptive antenna array design, to give you an example, was done between the US - Bell Labs' Murray Hill - and Stuttgart, so two non-Asian sites at Bell Labs involved in the innovations. These are wideband designs that can operate at any frequencies and are technology agnostic so they can operate for GSM, 3G and LTE (Long Term Evolution).

"We believe that next-generation network intelligence, 10-15 years from now, might rely on quantum computing"

The designs can also form beams so you can be very power-efficient. Power efficiency in the antenna is great as you want to put the power where it is needed and not just have omni (directional) as the default power distribution. You want to form beams where capacity is needed.

That is clearly a big part of what Bell Labs has been focussing on in the wireless domain as well as all the overlaying technologies that allow you to do beam-forming. The power amplifier efficiency, that is another way you lose power and you operate at a more costly operational expense. The magic inside that is another focus of Bell Labs on wireless.

In optics, it is moving from 100 Gig to 400 Gig coherent. We are one of the early innovators in 100 Gig coherent and we are now moving forward to higher-order modulation and 400 Gig.

On the DSL side it the vectoring/ crosstalk cancellation work where we have developed our own ASIC because the market could not meet the need we had. The algorithms ended up producing a component that will be in the first release of our products to maintain a market advantage.

We do see a need for some specialised devices like the FlexPath FP3 network processor, the IPTV product, the OTN (Optical Transport Network) switch that is at the heart of our optical products is our own ASIC, and the vectoring/ crosstalk cancellation engine in our DSL products. Those are the innovations Bell Labs comes up with and very often they lead to our portfolio innovations.

There is also a lot of novel stuff like quantum computing that is on the fringes of what people think telecoms is going to leverage but we are still active in some of those forward-looking disciplines.

We have quite a few researchers working on quantum computing, leveraging some of the material expertise that we have to fabricate novel designs in our lab and then create little quantum computing structures.

Why would quantum computing be useful in telecom?

It is very good for parsing and pattern matching. So when you are doing complex searches or analyses, then quantum computing comes to the fore.

We do believe there will be processing that will benefit from quantum computing constructs to make decisions in ever-increasingly intelligent networks. Quantum computing has certain advantages in terms of its ability to recognise complex states and do complex calculations. We believe that next-generation network intelligence, 10-15 years from now, might rely on quantum computing.

We don't have a clear application in mind other than we believe it is a very important space that we need to be pioneering.

"Operators realise that their real-estate resource - including down to the central office - is not the burden that it appeared to be a couple of years ago but a tremendous asset"

You wrote a recent blog on the future of the network. You mentioned the idea of the emergence of one network with the melding of wireless and wireline, and that this will halve the total cost of ownership. This is impressive but is it enough?

The half number relates to the lightRadio architecture. There are many ingredients in it. The most notable is that traffic growth is accounted for in that halving of the total cost of ownership. We calculated what the likely traffic demand would be going forward: a 30-fold increase in five years.

Based on that growth, when we computed how much the lightRadio architecture, involving the adaptive antenna arrays, small cells and the move to LTE, if you combine these things and map it into traffic demand, the number comes up that you can build the network for that traffic demand and with those new technologies and still halve the total cost of ownership.

It really is quite a bit more aggressive than it appears because it is taking account of a very significant growth in traffic.

Can we build that network and still lower the cost? The answer is yes.

You also say that intelligence will be increasingly distributed in the network, taking advantage of Moore's Law. This raises two questions. First, when does it make sense to make your own ASICs?

When I say ASICs I include FPGAs. FPGAs are your own design just on programmable silicon and normally you evolve that to an ASIC design once you get to the right volumes.

There is a thing called an NRE (non-recurring engineering) cost, a non-refundable engineering cost to product an ASIC in a fab. So you have to have a certain volume that makes it worthwhile to produce that ASIC, rather than keeping it in an FPGA which is a more expensive component because it is programmable and has excess logic. On the other hand, there is economics that says an FPGA is the right way for sub-10,000 volumes per annum whereas for millions of parts you would do an ASIC.

We work on both those types of designs. And generally, and I think even Huawei would agree with us, a lot of the early innovation is done in FPGAs because you are still playing with the feature set.

Photo: Denise Panyik-Dale

Photo: Denise Panyik-Dale

Often there is no standard at that point, there may be preliminary work that is ongoing, so you do the initial innovation pre-standard using FPGAs. You use a DSP or FPGA that can implement a brand new function that no one has thought of, and that is what Bell Labs will do. Then, as it starts becoming of interest to the standard bodies, you have it implemented in a way that tries to follow what the standard will be, and you stay in a FPGA for that process. At some point later, you take a bet that the functionality is fixed and the volume will be high enough, and you move to an ASIC.

So it is fairly commonplace for novel technology to be implemented by the [system] vendors. And only in the end stage when it has become commoditised to move to commercial silicon, meaning a Broadcom or a Marvell.

Also around the novel components we produce there are a whole host of commercial silicon components from Texas Instruments, Broadcom, Marvell, Vitesse and all those others. So we focus on the components where the magic is, where innovation is still high and where you can't produce the same performance from a commercial part. That is where we produce our own FPGAs and ASICs.

Is this trend becoming more prevalent? And if so, is it because of the increasing distribution of intelligence in network.

I think it is but only partly because of intelligence. The other part is speed. We are reaching the real edges of processing speed and generally the commercial parts are not at that nanometer of [CMOS process] technology that can keep up.

To give an example, our FlexPath processor for the router product we have is on 40nm technology. Generally ASICs are a technology generation behind FPGAs. To get the power footprint and the packet-processing performance we need, you can't do that with commercial components. You can do it in a very high-end FPGA but those devices are generally very expensive because they have extremely low yields. They can cost hundreds or thousands of dollars.

The tendency is to use FPGAs for the initial design but very quickly move to an ASIC because those [FGPA] parts are so rare and expensive; nor do they have the power footprint that you want. So if you are running at very high speeds - 100Gbps, 400Gbps - you run very hot, it is a very costly part and you quickly move to an ASIC.

Because of intelligence [in the network] we need to be making our own parts but again you can implement intelligence in FPGAs. The drive to ASICs is due to power footprint, performance at very high speeds and to some extent protection of intellectual property.

FPGAs can be reverse-engineered so there is some trend to use ASICs to protect against loss of intellectual property to less salubrious members of the industry.

Second, how will intelligence impact the photonic layer in particular?

You have all these dimensions you can trade off each other. There are things like flexible bit-rate optics, flexible modulation schemes to accommodate that, there is the intelligence of soft-decision FEC (forward error correction) where you are squeezing more out of a channel but not just making it a hard-decision FEC - is it a '0' or a '1' but giving a hint to the decoder as to whether it is likely to be a '0' or a '1'. And that improves your signal-to-noise ratio which allows you to go further with a given optics.

So you have several intelligent elements that you are going to co-ordinate to have an adaptive optical layer.

I do think that is the largest area.

Another area is smart or next-generation ROADMs - we call it connectionless, contentionless, and directionless.

There is a sense that as you start distributing resources in the network - cacheing resources and computing resources - there will be far more meshing in the metro network. There will be a need to route traffic optically to locally positioned resources - highly distributed data centre resources - and so there will be more photonic switching of traffic. Think of it as photonic offload to a local resource.

We are increasingly seeing operators realise that their real-estate resource - including down to the central office - is not the burden that it appeared to be a couple of years ago but a tremendous asset if you want to operate a private cloud infrastructure and offer it as a service, as you are closer to the user with lower latency and more guaranteed performance.

So if you think about that infrastructure, with highly distributed processing resources and offloading that at the photonic layer, essentially you can easily recognise that traffic needs to go to that location. You can argue that there will be more photonic switching at the edge because you don't need to route that traffic, it is going to one destination only.

This is an extension of the whole idea of converged backbone architecture we have, with interworking between the IP and optical domains, you don't route traffic that you don't need to route. If you know it is going to a peering point, you can keep that traffic in the optical domain and not send it up through the routing core and have it constantly routed when you know from the start where it is going.

So as you distribute computing and cacheing resources, you would offload in the optical layer rather than attempt to packet process everything.

There are smarts at that level too - photonic switching - as well as the intelligent photonic layer.

For the second part of the Q&A, click here

Q&A with JDSU's CTO

In Part 1 of a Q&A with Gazettabyte, Brandon Collings, JDS Uniphase's CTO for communications and commercial optical products, reflects on the key optical networking developments of the coming decade, how the role of optical component vendors is changing and next-generation ROADMs.

"For transmission components, photonic integration is the name of the game. If you are not doing it, you are not going to be a player"

Brandon Collings (left), JDSU

Q: What are the key optical networking trends of the next decade?

A: The two key pieces of technology at the photonic layer in the last decade were ROADMs [reconfigurable optical add-drop multiplexers] and the relentless reduction in size, cost and power of 10 Gigabit transponders.

If you look at the next decade, I see the same trends occupying us.

We are seeing a whole other generation of reconfigurable networks - this whole colourless, directionless, flexible spectrum - all this stuff is coming and it is requiring a complete overhaul of the transport network. We have to support Raman [amplifiers] and we need to support more flexible [optical] channel monitors to deal with flexible spectrum.

We have to overhaul every aspect of the transport system: the components, design, capability, usability and the management. It may take a good eight years for the dust to settle on how that all plays out.

The other piece is transmission size, cost and power.

Right now a 40 Gig or a 100 Gig transponder is large, power-hungry and extremely expensive. Ironically they don't look too different to a 10 Gig transponder in 1998 and you see where that has gone.

You have seen our recent announcement [a tunable laser in an SFP+ optical pluggable module]; that whole thing is now tunable, the size of your pinkie and costs a fraction of what it did in 1998.

I expect that same sort of progression to play out for 100 Gig, and we'll start to get into 400 Gig and some flexible devices in between 100 and 400 Gig.

The name of the game is going to be getting size, cost and power down to ensure density keeps going up and the cost-per-bit keeps going down; all that is enabled by the photonic devices themselves.

Is that what will occupy JDSU for the next decade?

This is what will occupy us at the component level. As you go up one level - and this will impact us more indirectly than it will our customers - we are seeing this ramp of capacity, driven by the likes of video, where the willingness to pay-per-bit is dropping through the floor but the cost to deliver that bit is dropping a lot less.

Operators are caught in the middle and they are after efficiency and cost advantages when operating their networks. We are seeing a re-evaluation of the age-old principles in how networks are operated: How they do protection, how they offer redundancy and how they do aggregation.

People are saying: 'Well, the optical layer is actual fairly cheap compared to the layer two and three. Let's see if we can't ask more of the somewhat cheaper network and maybe pull some of the complexity and requirements out of the upper layers and make that simpler, to end up with an overall cheaper and easier network to operate.'

That is putting a lot of feature requirements on us at the hardware level to build optical networks that are more capable and do more, as well as on our customers that must make that network easier to operate.

That is a challenge that will be a very interesting area of differentiation. There are so many knobs to turn as you try to build a better delivery system optimised over packets, OTN [Optical Transport Network] and photonics.

Are you noting changes among system vendors to become more vertically integrated?

I've heard whisperings of vendors wanting to figure out how they could be more vertically integrated. That's because: 'Well hey, that could make our products cheaper and we could differentiate'. But I think the reality is moving in the opposite direction.

To build differentiated, compelling products, you have to have expertise, capability and technology control all the way down to the materials level almost. Take for example the tunable XFP; that whole thing is enabled by complete technology ownership of an indium-phosphate fab and all the manufacturing that goes around it. That is a herculean effort.

It is tough to say they [system vendors] want to be vertically integrated because to do so effectively you need just a gigantic organisation.

JDSU is vertically integrated. We have an awful lot of technology and we have got a very large manufacturing infrastructure expertise and know-how. We can produce competitive products because for this particular application we use a PLC [planar lightwave circuit], and for that one, gallium arsenide. We can do this because we diversify all this infrastructure, operation and company size across a wide customer base.

Increasingly this is also into adjacent markets like solar, gesture recognition and optical interconnects. These adjacent spaces would not be something that a system vendor would probably want to get into.

The bottom line is that it [the trend] is actually going in the opposite direction because the level, size and scope of the vertical integration would need to be very large and completely non-trivial if system vendors want to be differentiating and compelling. And the business case would not work very well because it would only be for their product line.

"No one says exactly what they will pay for next-gen ROADMs but all can articulate why they want it and what it will do in general terms"

Is this system vendor trend changing the role of optical component players?

Our level of business and our competitors are looking to be more vertically integrated: semiconductors all the way to line cards.

We've proven it with things like our Super Transport Blade that the more you have control over, the more knobs you can turn to create new things when merging multiple functions.

Instead of selling a lot of small black boxes and having the OEMs splice them together, we can integrated those functions and make a more compact and cost-effective solution. But you have to start with the ability to make all those blocks yourself.

Whether it is a line card, a tunable XFP or a 100 Gig module, the more you own and control, the more you can integrate and the more effective your solution will be. This is playing out at the components level because you create more compelling solutions the more functional integration you accomplish.

How do you avoid competing with your customers? If system vendors are just putting cards together, what are they doing? Also, how do you help each vendor differentiate?

It is very true. There are several system vendors that don't build their line cards anymore. They have chosen to do so because they realise that from a design and manufacturing perspective, they don't add much value or even subtract value because we can do more functional integration and they may not be experts in wavelength-selective switch (WSS) construction and various other things.

A fair number of them basically acknowledge that giving these blades to the people who can do them is a better solution for them.

How they differentiate can go two ways.

First, they don't just say: 'Build me a ROADM card.' We work very closely; they are custom design cards for each vendor. They specify what the blade will do and they participate intimately in its design. They make their own choices and put in their own secret sauce.

That means we have very strong partnerships with these operations, almost to the extent that we are part of their development organisations.

The importance of things above the photonic layer collectively is probably more important than the photonic layer. Usability, multiplexing, aggregation, security - all the things that go into the higher levels of a network, this is where system vendors are differentiating.

They can still differentiate at the photonic layer by building strong partnerships with technology engines like JDSU and it allows them to focus more resources at the upper levels where they can differentiate their complete network offering.

"The new generation of reconfigurable networks are not able to reuse anything that is being built today"

"The new generation of reconfigurable networks are not able to reuse anything that is being built today"

Will is happening with regard photonic integration?

For transmission components, photonic integration is the name of the game. If you are not doing it, you are not going to be a player.

If you look at JDSU's tunable [laser] XFP, that is 100% photonic integration. Yes, we build an ASIC to control the device but it is just about getting a little bit extra volume and a little bit more power. The whole thing is about monolithic integration of a tunable laser, the modulator and some power control elements. And that is just 10 Gig.

If you look at 40 Gig, today's modulators are already putting in heavy integration and it is just the first round. These dual-polarisation QPSK modulators, they integrate multiple modulators - one for each polarisation as well as all the polarisation combining functionality, all into one device using waveguide-based integration. Today that is in lithium niobate, which is not a small technology.

100 Gig looks similar, it is just a little bit faster and when you go to 400 Gig, you go multi-carrier which means you make multiple copies of this same device.

So getting these things down in size, cost and power means photonic integration. And just the way 10 Gig migrated from lithium niobate down to monolithic indium phosphide, the same path is going to be followed for 40, 100 and 400 Gig.

It may be more complicated than 10 Gig but we are more advanced with our technology.

Operators are asking for advanced ROADM capabilities while system vendors are willing to provide such features but only once operators will pay for them. Meanwhile, optical component vendors must do significant ROADM development work without knowing when they will see a return. How does JDSU manage this situation and is there a way of working smart here?

I don't think there is a terrifically clever way to look at this other than to say that we speak very carefully and closely with our customers.

These next-generation ROADMs have been going on for three or four years now. We also meet operators globally and ask them very similar questions about when and how and to what extent their interest in these various features [colourless, directionless, contentionless, gridless (flexible spectrum)] lie.

We are a ROADM leader; this is a ROADM question so we'd be making critical decisions if we decided not to invest in this area. We have decided this is going to happen and we have invested very heavily in this space.

It is true; there is not a market there right now.

With anything that is new, if you want to be a market leader you can't enter a market that exists, otherwise you'll be late. So through those discussions with our customers and the trust we have with them, and understanding where their customers and their problems lie, we are confident in that investment.

If you look back at the initial round of ROADMs, the chitchat was the same. When WSSs and ROADMs first came out, the reaction was: 'Wow, these things are really expensive, why would I want this compared to a set of fixed filters which back then cost $100 a pop?".

The commentary on cost was all in that flavour but once they became available and the costs were known, the operators started adopting them because the operators could figure out how they could benefit from the flexibility. Today ROADMs are just about in every network in the world.

We expect the same track to follow. No one is going to say: 'Yes, I’m going to pay twice for this new functionality' because they are being cagey of course.

We are still in the development phase. We are starting to get to the end of that, so the costs and real capabilities - all enabled by the devices we are developing - are becoming clear enough so that our customers can now go to their customers and say: 'Here's what it is, here's what it does and here's what it cost'.

Operators will require time to get comfortable with that and figure out how that will work in their respective networks.

We have seen consistent interest in these next-generation ROADM features. No one says exactly what they will pay for it but all can articulate why they want it and what it will do in general terms.

You say you are starting to get to the end of the development phase of these next-generation ROADMs. What challenges remain?

The new generation of reconfigurable networks are not able to reuse anything that is being built today whether it is from JDSU or Finisar, whether it is MEMS or LCOS (liquid crystal on silicon).

All the devices that are on the shelf today simply are not adequate or you end up with extremely expensive solutions.

This requires us to have a completely new generation of products in the WSS and the multiplexing demultiplexing space - all the devices that will do these functions that were done by AWGs or today by a 1x9 WSS but what is under development, they just look completely different.

They are still WSSs but they use different technologies so without saying exactly what they are and what they do, it is basically a whole new platform of devices.

Can you say when we will know what these look like?

I think the general architecture is fairly well known.

The exact details of the devices and components are still not publicly being talked about but it is the general combination of high-port-count WSSs that support flexible spectrum, fast switching and low loss, and are being used in a route-and-select approach rather than a broadcast-and-select one. That is the node building block.

Then these multicast switches are being built - fibre amplifier arrays; what comprise the colourless, directionless and contentionless multiplexing and demultiplexing.

That is the general architecture - it seems that that is what everyone is settling on. The devices to support that are what the industry is working on.

For Part II of the Q&A with Brandon Collings, click here

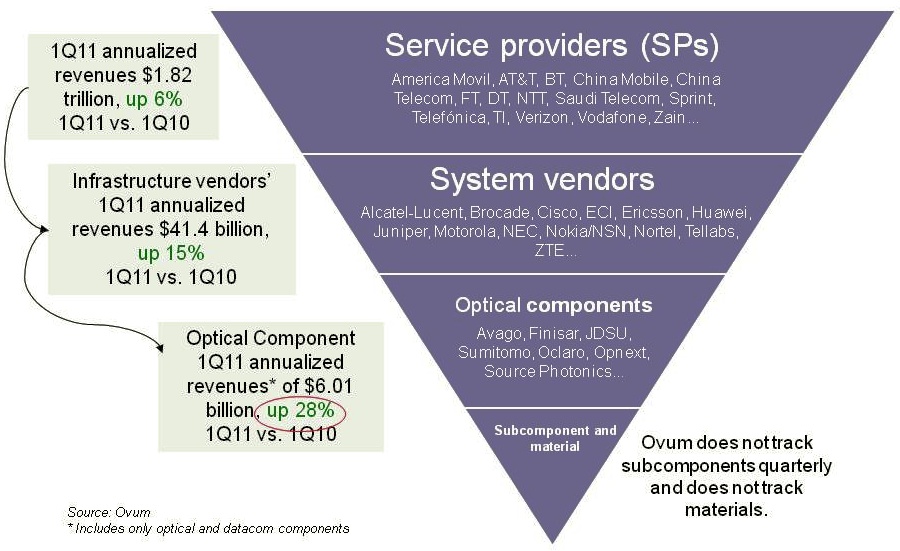

Optical components: The six billion dollar industry

The service provider industry, including wireless and wireline players, is up 6% year-on-year (2Q10 to 1Q11) to reach US $1.82 trillion, according to Ovum. The equipment market, mainly telecom vendors but also the likes of Brocade, has also shown strong growth - up 15% - to reach revenues of over $41.4 billion. But the most striking growth has occurred in the optical components market, up 28%, to achieve revenues of over $6 billion, says the market research firm.

Source: Ovum

Source: Ovum

“This is the first time optical components has exceeded six billion since 2001,” says Daryl Inniss, practice leader, Ovum Components. Moreover, the optical component industry growth has continued over six consecutive quarters with the growth being more than 25% for the past four quarters. “None of the other [two] segments have performed in this way,” says Inniss.

Ovum cites three factors accounting for the growth. Fibre-to-the-x (FTTx) is experiencing strong growth while revenues have entered the market from datacom players from the start of 2010. “The [optical] component recovery was led by datacom,” says Inniss. “We speculate that some of that money came from the Googles, Facebooks and Yahoos!.” A third factor accounting for growth has been optical equipment vendors ordering more long lead-time items than needed – such as ROADMs – to secure supply.

Source: Ovum

Source: Ovum

The second chart above shows the different market segments normalised since the start of 1999. Shown are the capex spending for optical networking, optical networking equipment revenues, optical components and FTTx equipment spending.

Optical networking spending is some 3.5x that of the components. FTTx equipment revenues are lower than the optical component industry’s and is therefore multiplied by 2.25, while capex is 9.2x that of optical equipment. The peak revenue in 2001 is the optical component revenues during the optical boom.

Several points can be drawn from the normalised chart:

- The strong recent growth in FTTx is the result of the booming Chinese market.

- From 2003 to 2008, the overall market showed steady growth, as illustrated by the best-fit line.

- From 2003 to 2008, capex and optical networking revenues were in line, while two thirds of the optical component revenues were due to this telecom spending.

- From 2010 onwards, components deviated from these two other segments due to the datacom spending from new players and the strong growth in FTTx.

- Once the market crashed in early 2009, optical components, networking and capex all fell. FTTx recovered after only one quarter and was followed by optical components. Optical networking and capex, meanwhile, have still not fully recovered when compared with the underlying growth line.

Capella: Why the ROADM market is a good place to be

The reconfigurable optical add-drop multiplexer (ROADM) market has been the best performing segment of the optical networking market over the last year. According to Infonetics Research, ROADM-based wavelength division multiplexing (WDM) equipment grew 20% from Q2, 2010 to Q1, 2011 whereas the overall optical networking market grew 7%.

“It’s the Moore’s Law: Every two years we are doubling the capacity in terms of channel count and port count”

Larry Schwerin, Capella

The ROADM market has since slowed down but Larry Schwerin, CEO of wavelength-selective-switch (WSS) provider, Capella Intelligent Subsystems, says the market prospects for ROADMs remain solid.

Capella makes WSS products that steer and monitor light at network nodes, while the company’s core intellectual property is closed-loop control. Its WSS products are compact, athermal designs based on MEMS technology that switch and monitor light.

Schwerin compares Capella to a plumbing company: “We clean out pipes and those pipes happen to be fibre-optics ones.” The reason such pipes need ‘cleaning’ – to be made more efficient - is because of the content they carry. “It is bandwidth demand and the nature of the bandwidth which has changed dramatically, that is the fundamental driver here,” says Schwerin.

Increasingly the content is high-bandwidth video and streamed to end-user devices no longer confined to the home, while the video requested is increasingly user-specific. Such changes in the nature of content are affecting the operators’ distribution networks.

“Using Verizon as an example, they are now pushing 50 wavelengths per fibre in the metro,” says Schwerin. Such broad lanes of traffic arrive at network congestion points where certain fibre is partially used while other fibre is heavily used. “What they [operators] need is a vehicle that allows them to dynamically and remotely reassign those wavelengths on-the-fly,” says Schwerin. “That is what the ROADM does.”

Capella attributes strong ROADM sales to a maturing of the technology coupled with a price reduction. The technology also brings valuable flexibility at the optical layer. “It [ROADM] extends the life of the existing infrastructure, avoiding the need for capital to put new fibre in - which is the last thing the operators want to do,” says Schwerin.

$20M funding

Capella raised US $20M in April as part of its latest funding round. The funding is being used for capital expansion and R&D. “We are working on new engine technology, new patentable concepts,” says Schwerin. “We were at Verizon a few weeks ago doing a world-first demo which we will be putting out as a press release.” For now the company will say that the demonstration is research-oriented and will not be implemented within ROADM systems anytime soon.

“You have to be competitive in this market, that is the downfall of our sector. People getting 30 or 40% gross margins and calling that a win – that is not a win - that is why this sector is in trouble”

One investor in the latest funding round is SingTel Innov8, the investment arm of the operator SingTel. Schwerin says it has no specific venture with the operator but that SingTel will gain insight regarding switching technologies due to the investment. “We will sit down with them and talk about their plans for network evolution and what is technologically possible,” says Schwerin, who points out that many of the carriers have lost contact with technologies since they shed their own large, in-house R&D arms.

Cappella offers two 1x9 WSS products and by the end of this year will also offer a 1x20 product. “It’s the Moore’s Law: Every two years we are doubling the capacity in terms of channel count and port count,” says Schwerin.

“We have a reasonable share of design wins shipping in volume - we have thousands of switches deployed throughout the world,” says Schwerin. “We are not of the size of a JDSU or a Finisar but our objective within the next 18 months is to capture enough market share that you would see us as a main supplier of that ilk.”

The CEO stresses that Capella’s presence a decade after the optical boom ended proves it is offering distinctive products. “Our whole business model is about innovation and differentiation,” says Schwerin.

But as a start-up how can Capella compete with a JDSU or a Finisar? “I have these conversations with the carriers: if all they are doing is looking for second or third sourcing of commodity product parts then there is no room for a company like a Capella.”

The key is taking a dumb switch and turning it into a complete wavelength managed solution that can be easily added within the network.

Schwerin also stresses the importance of ROADM specsmanship: wider lightpath channel passbands, lower insertion loss, smaller size, lower power consumption and competitive pricing: “You have to be competitive in this market, that is the downfall of our sector,” says Schwerin. “People getting 30 or 40% gross margins and calling that a win – that is not a win - that is why this sector is in trouble.”

Advanced ROADM features

There has been much discussion in the last year regarding the four advanced attributes being added to ROADM designs: colourless, directionless, contentionless and gridless or CDCG for short.

Interviewing six system vendors late last year, while all claimed they could support CDCG features, views varied as to what would be needed and by when. Meanwhile all the system vendors were being cautious until it was clearer as to what operators needed.

Schwerin says that what the operators really want is a ‘touchless’ ROADM. Capella says its platform is capable of supporting each of the four attributes and that the company has plans for implementing each one. “Just because the carriers say they want it, that doesn’t mean that they are willing to pay for it,” says Schwerin. “And given the intense pricing pressure our system friends are in, they are rightly being cautious.”

Capella says that talking to the carriers doesn’t necessarily answer the issue since views vary as to what is needed. “The one [attribute] that seems clearest of all is colourless,” says Schwerin. And colourless is served using higher-port-count WSSs.

The directionless attribute is more a question of implementation and the good news is that it requires more WSSs, says Schwerin. Contentionless addresses the issue of wavelength blocking and is the most vague, a requirement that has even “faded away a bit”. As for gridless, that may be furthest out as it has ramifications in the network.

Schwerin says that Capella is seeing requests for reduced WSS switching times as well as wavelength tracking, tagging a wavelength whose signature can be identified optically and which is useful for network restoration and when wavelengths are passed between carriers’ networks.

Roadmap

In terms of product plans, Capella will launch a 1x20 WSS product later this year. The next logical step in the development of WSS technology is moving to a solid-state-based design.

“All of the the technologies out there today– liquid crystal, MEMS, liquid-crystal-on-silicon - are all free space [designs],” says Schwerin. “We have a solid-state engine in the middle [of our WSS] and we are down to five photonic-integrated-circuit components so the obvious next stage is silicon photonics.”

Does that mean a waveguide-based design? “Something of that form – it may not be a waveguide solution but something akin to that - but the idea is to get it down to a chip,” says Schwerin. “We are not pure silicon photonics but we are heading that way.”

Such a compact chip-based WSS design is probably five years out, concludes Schwerin.

Further information:

A Fujitsu ROADM discussion with Verizon and Capella – a Youtube 30-min video

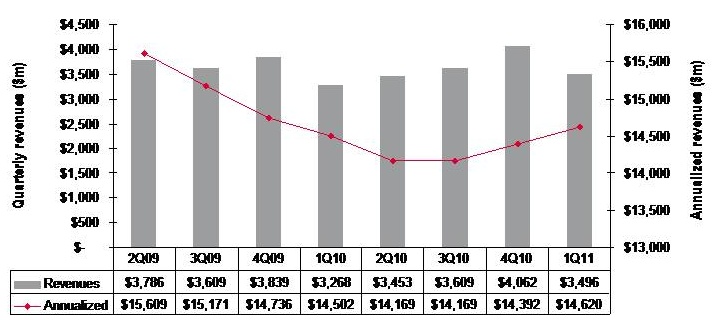

Optical networking market in rude health

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Despite recent falls in optical equipment makers’ stock, the optical networking market remains in good health with analysts predicting 6-7% growth in 2011.

For Andrew Schmitt, directing analyst for optical at Infonetics Research, unfulfilled expectations are nothing new. Optical networking is a market of single-digit yearly growth yet in the last year certain market segments have grown above average: spending on ROADM-based wavelength division multiplexing (WDM) optical network equipment, for example, has grown 20% since the first quarter of 2010.

“Every few years people get this expectation that there is going to be this hockey stick [growth] and it is not,” says Schmitt. “There has been a lot of Wall Street money moving into this sector in the latter part of 2010 and first part of this year and they have just had their expectations reset, but operationally the industry is very healthy.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate”

Andrew Schmitt, Infonetics Research

But Schmitt acknowledges that there is industry concern about the market outlook. “There have been lots of client calls in the first half of the year wanting to talk numbers,” says Schmitt. “When the market is growing rapidly there is no need for such calls but when it is uncertain, customers put more time into understanding what is going on.”

Both Infonetics and market research firm Ovum say the optical networking market grew 7% globally in the last year (2Q10 to 1Q11).

Ovum says the market reached US $3.5bn in the first quarter of 2011 and it expects 6% growth this year. “Most of the growth will come from North America—general recovery, stimulus-related spending, and LTE (Long Term Evolution)-inspired spending; and from South and Central America mostly mobile and fixed broadband-related,” says Dana Cooperson, network infrastructure practice leader at Ovum.

Ovum also notes that optical networking annualised spending for the last four quarters (2Q10-1Q11) finally went into the black with 1% growth, to reach $14.6bn. Annualised share figures are a strong indicator of longer-term market trends, says Ovum.

Market growth

Factors accounting for the growth include optical equipment demand for mobile and broadband backhaul. Carriers are also embarking on a multi-year optical upgrade to 40 and 100 Gigabit transmission over Optical Transport Network (OTN) and ROADM-based networks. Infonetics notes that ROADM spending in particular set a new high in the first quarter, rising 4% sequentially.

Ovum expects overall growth to come from metro and backbone WDM markets and from LTE. “For metro it is a combination of new builds, as DWDM continues to take over the metro core from SONET/SDH, and expansions of ROADM and 40 Gigabit,” says Cooperson. “For backbone it is a combination of retrofits for 40 and 100 Gigabit and overbuilds with 40 and 100 Gigabit coherent-optimised systems.”

Many operators are also looking at OTN switching and how it can help with network efficiency and manageability, she says, while mobile backhaul continues to be a hot spot as well at the access end of the network.

The Americas are the regions accounting for market growth whereas in Asia-Pacific and Europe, Middle East and Africa the spending remains flat.

“We’re not as bullish on Europe as I’ve heard some others are,” says Cooperson. “We expected China to slow down as capital intensities in the 34-35% seen in 2008 and 2009 were unsustainable. We saw the cooling down a bit earlier in 2010 than we had expected, but it did cool down and will continue to.”

Ovum expects Asia-Pacific as a whole to be moribund. But at least the pullbacks in China will be countered by slow growth in Japan and a big upsurge in India after a huge decline last year due to delayed 3G-related builds among other issues.

Outlook

Ovum is optimistic about the optical networking market due to continued competitive pressures and traffic growth. “We don’t think traffic growth can just continue without attention to the underlying issues related to revenue pressure, regardless of competitive pressures,” says Cooperson. “But newer optical and packet systems offer significant improvements over the old in terms of power efficiency, manageability, and of course 40 and 100 Gigabit coherent and ROADM features.”

“Most of the growth will come from North America"

Dana Cooperson, Ovum.

Many networks worldwide are also due for a core infrastructure update to benefit capacity and efficiency while many other operators are upgrading their access networks for mobile backhaul and enterprise Ethernet services.

Schmitt stresses that while it is right to talk about a 'core reboot', there are all sorts of operators that make up the market: the established carriers, those focussed on Layer 2 and Layer 3 transport, dark fibre companies and cable companies.

“Everyone has a different business so there is not a whole lot of group-think in this industry,” says Schmitt. “So when you talk about a transition to 40 and 100 Gigabit, some carriers will make that transition earlier than others because the nature of their business demands it.”

However, there are developments in equipment costs that are leading to change. “Once you get out to 2013-14, 100 Gigabit [transport] looks really good relative to 40 Gigabit and tunable XFPs at 10 Gigabit look really, really good,” says Schmitt, who believes these are going to be two dominating technologies. “People are going to use 100 Gigabit and when they can afford to throw more 10 Gigabit at the [capacity] problem, in shorter metro and regional spans, they will use tunable XFPs,” he says. “That is a whole new level in terms of driving down cost at 10 Gigabit that people haven’t factored in yet.”

Pacier change

The move to 100 Gigabit will not lead to increased spending, stresses Schmitt. Rather its significance is as a ‘mix shift’: The adoption of 100 Gigabit will shift spending from older systems to newer ones so that the technology is interesting in terms of market share shift rather than by growing overall revenues.

That said, there are areas of optical spending where capital expenditure (capex) is growing faster than the single-digit trend. These include certain competitive telco providers and dark fibre providers like AboveNet, TimeWarner Telecom and Colt. “You look at their capex year-over-year and it is increasing in some cases more over 20% a year,” says Schmitt.

He also notes that while the likes of Google, Yahoo, Microsoft and Apple do not spend on optical equipment as much as established operators such as Verizon or AT&T, their growth rate is higher. “There are sectors of the market that are growing quickly, and competition that are positioned to service those sectors successfully are going to see above-trend growth,” says Schmitt.

He highlights three areas of innovations - ‘big vectors’- that are going to change the business.

One is optical transport's move away from simple on-off keying signalling that opens up all kinds of innovation. Another is the shift in the players buying optical equipment. “A lot more of the R&D is driven by the AboveNets, Time Warners, Comcasts and the Googles and less by the old time PTTs,” says Schmitt. “That is going to change the way R&D is done.”

The third is photonic integration which Schmitt equates to the very early state of the electronics business. While Infinera has done some interesting things with integration, its latest 500 Gigabit PIC (photonic integrated circuit) is a big leap in density, he says: “It will be interesting if that sort of technology crosses over into other applications such as short- and intermediate-reach applications.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate,” says Schmitt. “These three things, when you throw them together in a pot, are going to result in some unpredictable outcomes.”

OFC announcements and market trends

More compact transceiver designs at 10, 40 and 100 Gigabit, advancements in reconfigurable optical add-drop multiplexer (ROADM) technology and parallel optical engine developments were all in evidence at this year’s OFC/NFOEC show held in Los Angeles in March.

“MSAs are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market”

“MSAs are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market”

Victor Krutul, Avago Technologies

Finisar said that the show was one of the busiest in recent years. “There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts,” says Rafik Ward, vice president of marketing at Finisar.

Ethernet interfaces

Opnext demonstrated an IEEE 100GBASE-ER4 module design at the show, the 100 Gigabit Ethernet (GbE) standard with a 40km reach. Based on the company’s CFP-based 100GBASE-LR4 10km module, the design uses a semiconductor optical amplifier (SOA) on the receive path to achieve the extended reach. The IEEE standard calls for an SOA in front of the photo-detectors for the 100GBASE-ER4 interface.

“We don’t have that [SOA] integrated yet, we are just showing the [design] feasibility,” says Jon Anderson, director of technology programme at Opnext. The extended reach interface will be used to connect IP core routers to transport system when the two platforms reside in separate facilities. Such a 40km requirement for a 100GbE interface is not common but is an important one to meet, says Anderson.

Opnext’s first-generation LR4, currently shipping, is a discrete design comprising four discrete transmitter optical sub-assemblies (TOSAs) and four receiver optical sub-assemblies (ROSAs) and an optical multiplexer and demultiplexer. The company’s next-generation design will integrate the four lasers and the optical multiplexer into a package and will be used in future more compact CFP2 and CFP4 modules.

The CFP2 module is half the size of the CFP module and the CFP4 is a quarter. In terms of maximum power, the CFP module is rated at 32W, the CFP2 12W and the CFP4 5W. “The CFP4 is a little bit wider and longer than the QSFP,” says Anderson. The first CFP2 modules are expected to become available in 2012 and the CFP4 in 2013.

System vendors are interested in the CFP4 as they want to support over one terabit of capacity on a 15-inch faceplate. Up to 16 ports can be supported –1.6Tbps – on a faceplate using the CFP4, and using a “belly-to-belly” configuration two rows of 16 ports will be possible, says Anderson.

Finisar demonstrated a distributed feedback laser (DFB) laser-based CFP module at OFC that implements the 10km 100GBASE-LR4 standard. The adoption of DFB lasers promises significant advantages compared to existing first-generation -LR4 modules that use electro-absorption modulated lasers (EMLs). “If you look at current designs, ours included, not only do they use EMLs which are significantly more expensive, but each is in its own package and has its own thermo-electric cooler,” says Ward.

Finisar’s use of DFBs means an integrated array of the lasers can be packaged and cooled using a single thermo-electric cooler, significantly reducing cost and nearly halving the power to 12W. “Now that the power [of the DFB-based] LR4 is 12W, we can place it within a CFP2 with its 25-28 Gigabit-per-second (Gbps) electrical I/O,” says Ward.

Moving to the faster input/output (I/O) compared to the CFP’s 10Gbps I/O means that that serialiser/ deserialiser (serdes) chipset can be replaced with simpler clock data recovery (CDR) circuitry. “By the time we move to the CFP4, we remove the CDRs completely,” says Ward. “It’s an un-retimed interface.” Finisar’s existing -LR4 design already uses an integrated four-photodetector array.

An early application of the 100GbE -LR4, as with the -ER4, is linking core routers with optical transport systems in operators’ central offices. Many Ethernet switch vendors have chosen to focus their early high-data efforts at 40GbE but Finisar says the move to 100GbE has started.

Finisar argues that the adoption of DFBs will ultimately prove the cost-benefits of a 4-channel 100GbE design which faces competition from the emerging 10x10 multi-source agreement (MSA). “Everything we have heard about the 10x10 [MSA] has been around cost,” says Ward. “The simple view inside Finisar is that by the time the Gen2 100GbE module that we showed at OFC gets to market, this argument [4x25Gig vs. 10x10Gig] will be a moot point.”

“40Gig is definitely still strong and healthy”

“40Gig is definitely still strong and healthy”

Jon Anderson, Opnext

By then the second-generation -LR4 module design will be cost competitive if not even lower cost than the 10x10 MSA. “If you look at optoelectronic components, at the end of the day what really drives cost is yield,” says Ward. “If we can get our yields of 25Gig DFBs down to a level that is similar to 10Gig DFB yields- it doesn’t have to match, just in the ballpark - then we have a solution where the 4x25Gig looks like a 4x10Gig solution and then I believe everyone will agree that 4x25Gig is a less expensive architecture.” Finisar expects the Gen2 CFP -LR4 in production by the first half of 2012.

Opnext demonstrated a 40GBASE- LR4 (40Gbps, up to 10km) standard in a QSFP+ module at OFC. Anderson says it is seeing demand for such a design from data centre operators and from switch and transport vendors.

Avago Technologies announced a 40Gbps QSFP+ module at OFC that implements the 100m IEEE 40GBASE-SR4. “It will interoperate with Avago’s SFP+ modules,” says Victor Krutul, director of marketing for the fibre optics division at Avago Technologies. The QSFP+ can interface to another QSFP+ module or to four 10Gbps SFP+ modules.

Avago also announced a proprietary mini-SFP+ design, 30% smaller than the standard SFP+ but which is electrically compatible. According to Krutul, the design came about following a request from one of its customers: “What it allows is the ability to have 64 ports on the front [panel] rather than 48.”

Did Avago consider making the mini-SFP+ design an MSA? “What we found with MSAs is that they are designed by committee, and when you have a committee you throw away innovation and you throw away time-to-market,” says Krutul.

Krutul was previously a marketing manager for Intel’s LightPeak before joining Avago over half a year ago.

“There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts”

“There was an increasing system-vendor presence at OFC, and there was a lot more interest from investor analysts”

Rafik Ward, Finisar.

Line-side interfaces

Opnext will be providing select customers with its 100Gbps DP-QPSK coherent module for trialling this quarter. The module has a 5-inch by 7-inch footprint and uses a 168-pin connector. “We are working to try and meet the OIF spec [with regard power consumption] which is 80W.” says Anderson. “It is challenging and it may not be met in the first generation [design].”

The company is also moving its 40Gbps 2km very short reach (VSR) transponder to support the IEEE 40GBASE-FR standard within a CFP module, dubbed the “tri-rate” design. “The 40BASE-FR has been approved, with the specification building on the ITU’s 40Gig VSR,” says Anderson. “It continues to support the [OC-768] SONET/SDH rate, it will support the new OTN ODU3 40Gbps and the intermediate 40 Gigabit Ethernet.”

Opnext and Finisar are both watching with interest the emerging 100Gbps direct detection market, an alternative to 100 Gigabit coherent aimed shorter reach metro applications.

“We certainly are watching this segment and do have an interest, but we don’t have any product plans to share at this point,” says Anderson.

“The [100Gbps] direct-detection market is very interesting,” says Ward. Coherent is not going to be the only way people will deploy 100Gbps light paths. “There will be a market for shorter reach, lower performance 100 Gigabit DWDM that will be used primarily in datacentre-to-datacentre,” he says. Tier 2 and tier 3 carriers will also be interested in the technology for use in shorter metro reaches. “There is definitely a market for that,” says Ward.

Opnext also announced its small form-factor – 3.5-inch by 4.5-inch - 40Gbps DPSK module. “With a smaller form factor, the next generation could move to a CFP type pluggable,” says Anderson. “But that is if our customers are interested in migrating to a pluggable design for DPSK and DQPSK.”

Are there signs that the advent of 100 Gigabit is affecting 40Gbps uptake? “We definitely not seeing that,” says Anderson. “We are continuing to see good solid demand for both 40G line side – DPSK and DQPSK – and a lot of pull to being this tri-rate VSR.”

Such demand is not just from China but also North Ametican carriers. “40 Gig is definitely still strong and healthy,” says Anderson “But there are some operators that are waiting to see how 100G does and approved in for major build-outs.”

At 10Gbps, Opnext also had on show a tunable TOSA for use in an XFP module, while Finisar announced an 80km, 10Gbps SFP+ module. “SFP+ has become a very successful form factor at 10Gbps,” says Ward. “All the market data I see show SFP+ leads in overall volumes deployed by a significant margin.” Its success has been achieved despite being a form factor was not designed to achieve all the 10Gbps reaches required initially. This is some achievement, says Ward, since the XFP+ form factor used for 80km has a power rating of 3.5W while the 80km SFP+ has to work within a less than 2W upper limit.

Parallel Optics

Avago detailed its main parallel optic designs: the CXP module and its two optical engine designs.

The company claims it seeing much interested from high-performance computing vendors such as IBM and Fujitsu for its CXP 120 Gigabit (12x10Gbps) parallel transceiver module. Avago is sampling the module and it will start shipping in the summer.

The company also announced the status of its embedded parallel optics devices (PODs). Such parallel optic designs offer several advantages, says Krutul. Embedding the optics on the motherboard offers greater flexibility in cooling since the traditional optics is normally at the edge of the card, furthest away from the fans. Such optics also simplify high-speed signal routing on the printed circuit board since fibre is used.

Avago offers two designs – the 8x8mm MicroPod and the 22x18mm MiniPod. The 12x10Gbps MicroPods are being used in IBM’s Blue Gene computer and Avago says it is already shipping tens of thousands of the devices a month. “The [MicroPod’s] signal pins have a very tight pitch and some of our customers find that difficult to do,” says Krutul. The MiniPod design tackles this by using the MicroPod optical engine but a more relaxed pitch. At OFC, Avago said that the MiniPod is now sampling.

Gridless ROADMs

Finisar demonstrated what it claims is the first gridless wavelength-selective switch (WSS) module at the show. A gridless ROADM supports variable channel widths beyond the fixed International Telecommunication Union's (ITU) defined spacings. Such a capability enables ROADMs to support variable channel spacings that may be required for transmission rates beyond 100Gbps: 400Gbps, 1Tbps and beyond.

“We have an increasing amount of customer interest in this [FlexGrid], and from what we can tell, there is also an increasing amount of carrier interest as well,” says Ward, adding that the company is already shipping FlexGrid WSSs to customers.

Finisar is a contributing to the ongoing ITU work to define what the grid spacings and the central channels should be for future ROADM deployments. Finisar demonstrated its FlexGrid design implementing integer increments of 12.5GHz spacing. “We could probably go down to 1GHz or even lower than that,” says Ward. “But the network management system required to manage such [fine] granularity would become incredibly complicated.” What is required for gridless is a balance between making good use of the fibre’s spectrum while ensuring the system in manageable, says Ward.

To efficiency and beyond

Part 3: ROADM and control plane developments

ROADMs and control plane technology look set to finally deliver reconfigurable optical networks but challenges remain.

Operators are assessing how best to architect their networks - from the router to the optical layer - to boost efficiencies and reduce costs. It is developments at the photonic layer that promise to make the most telling contribution to lowering the cost of transport, a necessity given how the revenue-per-bit that carriers receive continues to dwindle.

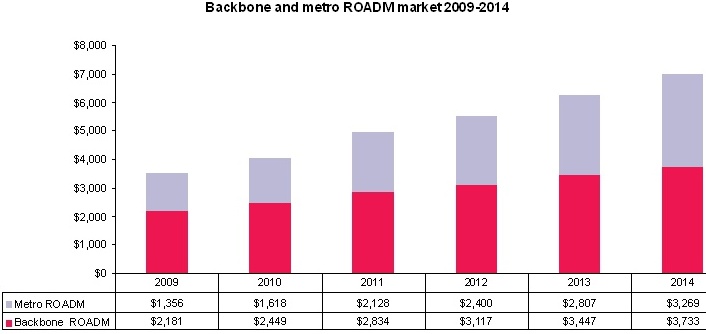

Global ROADM forecast 2009 -14 in US $ miliions Source: Ovum

Global ROADM forecast 2009 -14 in US $ miliions Source: Ovum