From spin-out to scale-up: OpenLight’s $34M funding

Part 1: Start-up funding

OpenLight Photonics, a Santa Barbara-based start-up specialising in silicon photonics, has raised $34 million in an oversubscribed Series A funding round.

The start-up will use the funding to expand production and its photonic integrated circuit (PIC) design staff.

OpenLight Photonics raises $34M in an oversubscribed Series A.

“We’re starting to get customers taking in production mask sets, so it’s about scaling operations and how we handle production,” says OpenLight CEO, Adam Carter (pictured). The start-up needs more PIC designers to work with customers.

Technology

OpenLight’s technology originated at Aurrion, a fabless silicon photonics start-up from the University of California, Santa Barbara.

Aurrion’s heterogeneous integration silicon photonics technology supports III-V materials, enabling components such as lasers, modulators, and optical amplification to be part of a photonic integrated circuit (PIC). Intel has its own heterogeneous integration silicon photonics process, which it has used to make millions of pluggable optical transceivers. OpenLight is offering the technology to customers effectively as a photonic ASIC design house.

Juniper Networks bought Aurrion in 2016 and, in 2022, spun out the unit that became OpenLight. Electronic design tool specialist Synopsys joined Juniper in backing the venture. Synopsys announced it was acquiring simulation company Ansys, a $35 billion deal it completed in July. Given that Synopsys would be focused on integrating Ansys, it suggested to OpenLight in January that they should part ways.

Funding

“We were only looking for $25 million to start with, and we finished at $34 million,” says Carter. Capricorn Investment Group was a late entrant and wanted to co-lead the funding round. Given initial commitments from other funders, Mayfield and Xora Innovation, set specific ownership percentages, it required an increase to accommodate Capricorn.

Xora’s first contact with OpenLight was after it approached the start-up’s stand at the OFC 2025 event held in March.

Juniper—now under HPE—is also an investor. The company played a key role in helping OpenLight while it sought funding. “Juniper could see that we were very close to an intercept point regarding our business model and our customers, so that’s why Juniper invested,” says Carter.

HPE continually looks at technologies it will require; silicon photonics with heterogeneous integration is one such technology, says Carter. However, HPE has no deal with OpenLight at this time.

Design roadmap

OpenLight is developing a 1.6-terabit PIC, now at an advanced prototype (beta) stage. The design uses eight channels for a 1.6T-DR8 OSFP pluggable design, implemented using four lasers and eight modulators, each operating at 200 gigabit-per-second (Gbps).

Carter says the first wafers will come from foundry Tower Semiconductor around October. This will be OpenLight’s largest production run — 100 wafers in four batches of 25. Some ten customers will evaluate the PICs, potentially leading to qualification.

A coarse wavelength division multiplexing (CWDM) 1.6-terabit design will follow in 2026. The CWDM uses 4 wavelengths, each at 200Gbps, on a fibre, with two such paths used for the 1.6T OSFP-XD 2xFR4 optical module.

The company is also pushing to develop 400Gbps channels, increasing the frequency response and improving the extinction ratio through process changes.

“We’ve got a whole series of experiments coming out over the next few months,“ says Carter. The frequency response of the indium phosphide modulator has already been improved by 10 gigahertz (GHz) to 90-95GHz. The process changes will be adopted for some alpha sample wafers in production that may enable modulation at 400Gbps, hence a 3.2-terabit PIC design.

“If we can show some good 3.2-terabit eyes, just as a demo, it shows that there’s a technology route to get there whenever 3.2-terabit modules are needed,” he says.

Customer growth

OpenLight’s customers have grown from three in 2023 to 17 last year to 20 actively designing. “We are growing the pipeline,” says Carter.

Early adopters were start-ups, but now larger firms are engaging Openlight. “Investors noted start-ups take more risk, but now bigger companies are coming in to drive volume,” says Carter.

Optical interconnect will drive initial volumes, but automotive and industrial sensing will follow. “The mix will change, but for the next couple of years, the revenues will be from optical interconnect,” says Carter.

Co-packaged optics is another interconnect opportunity. Here, OpenLight’s integrated laser technology would not be needed, given the co-packaged optics designs favour external laser sources. Instead, the company can offer integrated indium phosphide modulator banks or modulator banks with semiconductor optical amplifiers (SOAs), their compact size—“microns, not millimetres”—aiding packaging.

In addition to the foundry Tower Semiconductor for its wafers, OpenLight partners with Jabil, Sanmina, and TFC for the packaging and does its testing via ISC, an ASE subsidiary.

“They know test and certain customers with ISC, and ASE could do a complete turnkey solution,” says Carter. “But our priority is to get the test area set up to deal with the production; we’ve not had 100 wafers in a year being delivered for test.”

Silicon photonics

Carter, who was at Cisco when it acquired Lightwire in 2012, says silicon photonics’ potential to shrink optical designs was already recognised then. Since then, a lot of progress has been made, but now the focus is on building the supporting ecosystem. This includes a choice of foundries offering optical process design kits (PDKs) and outsourced assembly and test houses (OSATs) that can handle volumes.

Until now, silicon photonics has been all passive circuits. Now OpenLight, working with Tower and its PDK, is offering customers the ability to design and make heterogeneous integrated silicon photonics circuits. “Every customer gets the same PDK,” says Carter.

And it need not just be indium phosphide. The idea is to expand the PDK to support modulation materials such as polymer and thin-film lithium niobate. “If it is a better material, we’ll integrate it,” he says.

Having secured the funding, Carter is clear about the company’s priority: “It’s all about execution now.”

Acacia uses silicon photonics for its 100G coherent CFP

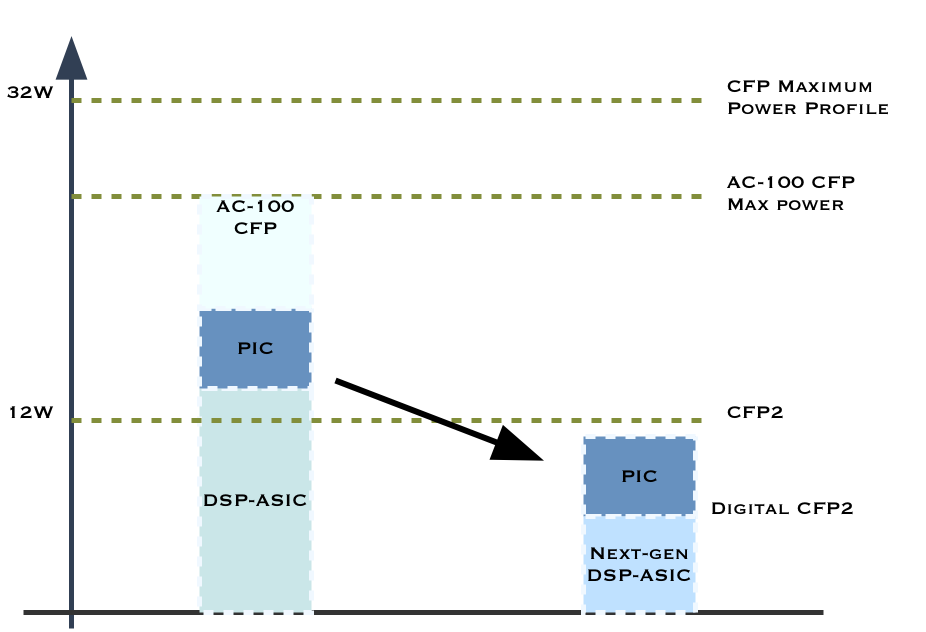

Acacia Communications has revealed the innards of its 100 Gig coherent pluggable module for metro networks. The AC-100 CFP combines a low-power DSP-ASIC with a silicon-photonics-based optics chip. The CFP's reach is 80km to 1,200km, and its power consumption is 24-26W, well within the pluggable's maximum power profile of 32W.

The power consumption of the AC-100 CFP, and its main components, and the target power consumptions of the components needed for a digital CFP2. Source: Gazettabyte

The power consumption of the AC-100 CFP, and its main components, and the target power consumptions of the components needed for a digital CFP2. Source: Gazettabyte

The start-up says it is shipping samples of the AC-100 CFP and already has 15 customers. "That includes some of the bigger [systems] players that have their own internal DSP," says Raj Shanmugaraj, CEO of Acacia. "The coherent CFP is not their focus; they are going after long-haul."

The start-up is shipping samples of the AC-100 CFP and already has 15 customers

Acacia chose to develop it own DSP chips as it sees the technology as core for coherent-based optical transmission. "That is where we see the big market," says Shanmugaraj. "We have a 100 Gig [MSA] that has been shipping, and a 200-400 Gig product that is in development."

DSP-ASIC and silicon photonics

The DSP-ASIC for the AC-100 CFP is Acacia's second chip design. Its first, a DSP-ASIC for its long-haul 5x7-inch OIF MSA transponder, is implemented using a 40nm CMOS process. The latest metro DSP-ASIC uses 28nm CMOS.

The DSP-ASIC includes analogue-to-digital (A/D) and digital-to-analogue (D/A) converters and a serialiser/ deserialiser (Serdes). Also on-chip is the digital signal processor (DSP) that implements soft-decision, forward error correction (SD-FEC) and compensation algorithms for chromatic and polarisation-mode dispersion.

Other DSP-ASIC features include spectral shaping for flexible grid transmission. "The signal processing on the transmit side fits in the one ASIC," says Benny Mikkelsen, CTO at Acacia. Also on-chip are a 100 Gig OTN (Optical Transport Network) framer and a microprocessor to manage the DSP-ASIC and the overall CFP.

The DSP-ASIC consumes 12-14W: the A/D, D/A converters and Serdes consume 5W, while the DSP consumes 7W for an 80km link - the 100 Gig equivalent of the -ZR spec - and 9W for 1,200km transmission due to the more powerful SD-FEC needed.

Mikkelsen says achieving a low-power ASIC requires several approaches. The SD-FEC is designed to be extremely low power, he says, as is the dispersion compensation: "Not just the algorithms but how we code the algorithms." Also, how the ASIC's circuitry is laid out impacts power consumption.

Acacia's engineers have also developed a silicon-photonics chip that combines the coherent transmitter and receiver optics. "The PIC [photonic integrated circuit] is the first silicon-photonics chip targeted at metro/ metro-regional," says Shanmugaraj. "It is an IC that has all the components except the laser, and is co-packaged in a gold box with the drivers and trans-impedance amplifiers."

Acacia's PIC is monolithic; all the functional blocks are implemented in silicon rather than combined silicon and III-V materials, a technique known as heterogeneous integration.

Using silicon photonics rather than indium phosphide has advantages, says Shanmugaraj. Silicon photonics benefits from mature CMOS processes developed for the semiconductor industry: "With the large silicon wafers, you can have thousands of these silicon PICs on them," he says.

Acacia tests the PICs directly on the wafer. This avoids having to dice the wafer and package each die before testing. "We also don't need thermal control [of the chip] or hermetic packaging," says Shanmugaraj. With indium phosphide, the modulators do require thermal cooling, adding to the design complexity and the power consumption. The PIC is 10mm long and consumes less than 5W.

The AC-100 CFP is expected to cost less than half the 5x7-inch 100 Gig coherent MSA which sells for $20,000. "One of the biggest pain points in metro is cost, if you ask most of the service providers," says Shanmugaraj. At below $10,000, the coherent CFP will be cost-competitive with the 100 Gig direct-detection CFP that uses 4x25 Gig wavelengths. However, the 100 Gig direct-detection CFP continues to come down in price as more products come to market.

Roadmap

Acacia will continue to address long-haul and metro, each requiring its own ASIC. "We don't believe that you can have one ASIC that serves both submarine and the metro," says Mikkelsen. In turn, silicon photonics will be used for pluggables while discrete optics will be used for the more demanding submarine.

The company says it is developing a multi-core ASIC to support super-channels and 16-QAM modulation for 200 Gig and 400 Gig transmission. The company says it will provide more details of its flexible, adaptive-rate ASIC at ECOC, to be held in September this year.

The company's product roadmap also features a co-packaged DSP-ASIC and PIC that will fit within a CFP2. Achieving such a pluggable, dubbed a digital CFP2, require a further halving of the DSP-ASIC's power consumption. This, says Acacia, is achievable using the next CMOS process node after 28nm.

The advantages of a digital CFP2 compared to a CFP2 with optics only, with the DSP-ASIC on the line card, include using the DSP-ASIC only when it is needed. When a fault occurs, the relevant pluggable can be replaced rather than having to remove the complete line card. Lastly, new functionality in the DSP-ASIC can be introduced by plugging in the new CFP2 pluggable compared with having to redesign the line card.

See also:

Transmode adopts 100 Gigabit coherent CFPs, click here

ClariPhy samples a 200 Gigabit coherent DSP-ASIC, click here

Infinera adds software to its PIC for instant bandwidth

Infinera has enabled its DTN-X platform to deliver rapidly 100 Gigabit services. The ability to fulfill capacity demand quickly is seen as a competitive advantage by operators. Gazettabyte spoke with Infinera and TeliaSonera International Carrier, a DTN-X customer, about the merits of its 'instant bandwidth' and asked several industry analysts for their views.

Infinera has added a WDM line card hosting its 500 Gigabit super-channel photonic integrated circuit to its DTN-X platform

Infinera has added a WDM line card hosting its 500 Gigabit super-channel photonic integrated circuit to its DTN-X platform

Pravin Mahajan, Infinera.

Infinera is claiming an industry first with the software-enablement of 100 Gigabit capacity increments. The company's DTN-X platform's 'instant bandwidth' feature shortens the time to add new capacity in the network, from weeks as is common today to less than a day.

The ability to add bandwidth as required is increasingly valued by operators. TeliaSonera International Carrier points out that its traffic demands are increasingly variable, making capacity requirements harder to forecast and manage.

"It [the DTN-X's instant bandwidth] enables us to activate 100 Gig services between network spans to manage our own IP traffic which is growing rapidly," says Ivo Pascucci, head of sales, Americas at TeliaSonera International Carrier. "We will also be able to sell in the market 100 Gig services and activate the capacity much more rapidly."

What has been done

Infinera has added three elements to enable its DTN-X platform to enable 100 Gigabit services.

One is a new wavelength division multiplexing (WDM) line card that features its 500 Gigabit-per-second (Gbps) super-channel photonic integrated circuit (PIC). Infinera says the line card has 500Gbps of capacity enabled, of which only 100Gbps is activated. "The remaining 400Gbps is latent, waiting to be activated," says Pravin Mahajan, director of corporate marketing and messaging at Infinera.

Infinera uses the DTN-X's Optical Transport Network (OTN) switch fabric to pack the client side signals onto any of the 100Gbps channels activated on the line side. This capacity pool of up to 500 Gbps, says Infinera, results in better usage of backbone capacity compared to traditional optical networking equipment based on individual 100Gbps 'siloed' channels.

A software application has also been added to Infinera's network management system, the digital network administrator (DNA), to activate the 100Gbps capacity increments.

Lastly, Infinera has in place a just-in-time system that enables client-side 10 Gigabit Ethernet optical transceivers to be delivered to customers within 10 days, if they out of stock. Infinera says it is achieving a 6-day delivery time in 95% of the cases.

Advantages

TeliaSonera International Carrier confirms the advantages to having 100 Gigabit capacities pre-provisioned and ready for use.

"Having the ability to turn up large bandwidth is critical to our business, especially as the [traffic] numbers continue to grow"

"Having the ability to turn up large bandwidth is critical to our business, especially as the [traffic] numbers continue to grow"

Ivo Pascucci, TeliaSonera International Carrier

"If it is individual line cards across the network when you have as many PoPs as we do, it does get tricky," says Pascucci. "If we have 500 Gig channels pre-provisioned with the ability to activate 100 Gig segments as needed, that gives us an advantage versus having to figure out how many line cards to have deployed in which nodes, and forecasting which nodes should have the line cards in the first place."

The operator is already seeing demand for 100 Gigabit services, from the carrier market and large content providers. The operator already provides 10x10Gbps and 20x10Gbps services to customers. "With that there are all the challenges of provisioning ten or 20 10 Gig circuits and 10 or 20 cross-connects for each site," says Pascucci. The operator also manages one and two Terabits of network capacity for certain customers.

"Having the ability to turn up large bandwidth is critical to our business, especially as the [traffic] numbers continue to grow," says Pascucci.

Analysts' comments

Gazettabye asked several industry analysts about the significance of Infinera's announcement. In particular the uniqueness of the offering, the claim to reduce rapidly bandwidth enablement times and its importance for operators.

Infonetics Research

Andrew Schmitt, directing analyst for optical

Schmitt believes Infinera's announcement is significant as it is the first announced North American win. It also shows the company has a solution for carriers that only want to roll out a single 100 Gbps but don't want to buy 500Gbps.

More importantly, it should allow some carriers to deploy extra capacity for future use at no cost to them and that opens up interesting possibilities for automatically switched optical network (ASON) management or even software-defined networking (SDN).

"As to the claim that it reduces capacity enablement from weeks to potential minutes, to some degree, yes," says Schmitt.

Certainly Ciena, Alcatel-Lucent or Cisco could ship extra line cards into customers and not charge the customer until they are used and that would effectively achieve the same result. "But if the PIC truly has better economics than the discrete solutions from these vendors then Infinera can ship hardware up front and then recognise the profits on the back end," he says.

"You simply can't predict where the best places to put bandwidth will be"

In turn, if customers get free inventory management out of the deal and Infinera equipment can support that arrangement more economically, that is a significant advantage for Infinera.

"This instant bandwidth is unique to Infinera. As I said, anyone could do this deal. But you need a hardware cost structure that can support it or it gets expensive quickly," says Schmitt. "Everyone is working on super-channels but it is clear from the legacy of the way the 10 Gig DTN hardware and software worked that Infinera gets it."

Schmitt believes the term super-channel is abused. He prefers the term virtualised bandwidth - optical capacity that can be allocated the same way server or storage resources are assigned through virtualization.

"The SDN hype is hitting strong in this business but Infinera is really one of the only companies that have a history of a hardware and software architecture that lends itself well to this concept," he says. This is validated with its customer list which is loaded heavily with service providers that are not just talking about SDN but actively doing something, he says.

"It [turning capacity up quickly] is important for SDN as well as more advanced protection arrangements. You simply can't predict where the best places to put bandwidth will be," says Schmitt. "If you can have spare capacity in the network that is lit on demand but not paid for if you don't need it, it is the cheapest approach for avoiding overbuilding a network for corner-case requirements.

"I think the accounting for this product will be interesting, it is likely that we will know in a year how successful this concept was just by a careful examination of the company's financials," he concludes.

ACG Research

Eve Griliches, vice president of optical networking

Infinera delivered this year the DTN-X with 500 Gig super-channels based on PIC technology. Now, a new 500 Gig line card has been added that can operate at 100 Gig and the remaining 400 Gig can be lit in 100 Gig increments using software. This allows customers to purchase 100 Gig at a time, and turn up subsequent bandwidth via software when they require it.

“No other vendor has a software-based solution, and no one else is delivering 500 Gig yet either,” says Griliches.

With this solution, ACG Research says in its research note, operators can start to develop a flexible infrastructure where bandwidth can grow and move around the network instantly. This is useful to address varying demands in bandwidth, triggered by incidents such as natural disasters or sporting events.

Rapid bandwidth enablement has always been important and takes way too long, so this development is key, says Griliches: “Also, it enables Infinera to enter markets which only need one 100 Gig wavelength for now, which they could not do before.”

“No other vendor has a software-based solution, and no one else is delivering 500 Gig yet either”

Looking forward, ACG Research expects this software and hardware-based instant bandwidth utility model will enable Infinera to widen its potential market base and increase its global market share in 2013 and 2014.

Ovum

Ron Kline, principal analyst, and Dana Cooperson, vice president, of the network infrastructure practice

Ovum also thinks Infinera's announcement is significant. It brings essentially the same value proposition Infinera had with 10 Gigabit to the 100 Gigabit market - low operational expenditure (opex) and quick time-to-market. ”Remember 10 Gig in 10 days?” says Kline.

It further fixes an issue for customers in that with the 10x10Gbps, they had to essentially pay for the full 100Gbps up front, and then they could be very efficient with turn-up and opex. Customers made an efficient opex for more capital expenditure (capex) up-front trade. "With instant bandwidth, they don't have to make the upfront capex-versus-opex tradeoff; they can be most efficient with both,” says Cooperson.

Any vendor can shorten capacity enablement times if they can convince the operator to pre-position bandwidth in the network that is ready to be turned on at a moment's notice.

Ron Kline

Kline says operators has different processes for turning up services and in many cases it is these processes and not the equipment directly that is the cause of the additional time for provisioning. “For example the operator may not use the DNA system or may have a very complex OSS/BSS used in the process,” says Kline.

Nevertheless, the capability to have really short provisioning is there, if an operator wants to take advantage. In the TeliaSonera case, Infinera is managing the network so the quick time to market will be there, says Kline.

Cooperson adds that there can be many factors that impede the capacity enablement process, based on Ovum's own research. “But it is clear from talking to Infinera's customers that its system design and approach is a big benefit to those carriers, often the competitive carriers, in competing in the market,” she says. “Multiple carriers told us that with the Infinera system, they were able to win business from competitors.”

Any vendor can shorten capacity enablement times if they can convince the operator to pre-position bandwidth in the network that is ready to be turned on at a moment's notice. However what is unique to Infinera is its system is deployed 500Gbps at a time and all the switching is done electrically by the OTN switch at each node. Others are working on super-channels but none are close to deploying, says Ovum.

“Multiple carriers told us that with the Infinera system, they were able to win business from competitors.”

Dana Cooperson

The ability to turn on bandwidth rapidly is becoming increasingly important. From a wholesale operator perspective it is very important and a key differentiator.

"It's particularly relevant to wholesale applications where large bandwidth chunks are required and the customer is another carrier," says Cooperson. "Whether you view a Google or a Facebook as a carrier or a very large enterprise, it would apply to them as well as a more traditional carrier."

Photonic integration specialist OneChip tackles PON

Briefing: PON

Part 1: Monolithic integrated transceivers

OneChip Photonics is moving to volume production of PON transceivers based on its photonic integrated circuit (PIC) design. The company believes that its transceivers can achieve a 20% price advantage.

"We will be able to sell [our integrated PON transceivers] at a 20% price differential when we reach high volumes"

Andy Weirich, OneChip Photonics

OneChip Photonics has already provided transceiver engineering samples to prospective customers and will start the qualification process with some customers this month. It expects to start delivering limited quantities of its optical transceivers in the next quarter.

The company's primary products are Ethernet PON (EPON) and Gigabit PON (GPON) transceivers. But it is also considering selling a bi-directional optical sub-assembly (BOSA), a component of its transceivers, to those system providers that want to attach the BOSA directly to the printed circuit board (PCB) in their optical network units (ONUs).

"The BOSA is the sub-assembly that contains all the optics, usually the TIA [trans-impedance amplifier] and sometimes the laser driver," says Andy Weirich, OneChip Photonics' vice president of product line management.

The company will roll out its Ethernet PON (EPON) ONU transceivers in the second quarter of 2012, followed by GPON ONU transceivers in the third quarter.

PON Technologies

EPON operates at 1.25 Gigabit-per-second (Gbps) upstream and downstream. OneChip had planned to develop a 2.5Gbps EPON variant which, says OneChip, has been standardised by the China Communications Standards Association (CCSA). But the company has abandoned the design since volumes have been extremely small and there have been no deployments in China.

GPON is a 2.5Gbps downstream/ 1.25Gbps upstream technology. The main differences between GPON and EPON transceiver optical components are the requirement of the ONU's receiver optics and circuitry, and the laser type, says Weirich. GPON's Class B+ specification, used for nearly all the GPON deployments, calls for a 28-29dB sensitivity. This is a more demanding specification requirement to meet than EPON's. GPON also calls for a Distributed Feedback (DFB) laser, whereas an EPON ONU may use either a Fabry-Perot laser or a DFB laser.

OneChip uses the same DFB for GPON and EPON ONUs. Where the PIC designs differ is the receiver assembly where GPON requires amplification. This, says Weirich, is achieved using either an avalanche photodiode (APD) or a semiconductor optical amplifier (SOA).

OneChip will start with an APD but will progress to an SOA. Once it integrates an SOA as part of the PIC, a simpler, cheaper photo-detector can be used.

Weirich admits that it has taken OneChip longer than it expected to develop its monolithically-integrated design.

Part of the challenge has been the issue of packaging the PIC. "Because of our integrated approach and non-alignment-requiring assembly, we have had to solve a few more technology problems," he says. "Our suppliers have had a challenge with some of those issues, and it has taken a couple of iterations to solve."

OneChip says that the good news is that the price erosion of EPON transceivers has slowed down in the last two years. So while Weirich admits the market is more competitive now, what is promising is that volumes have continued to grow.

"There is no sign of saturation happening either in the EPON or GPON markets," he says. And OneChip believes it can compete on price. "What we are saying is that we will be able to sell [our monolithically integrated PON transceivers) at a 20% price differential when we reach high volumes." That is because the monolithic design is simpler and the optical components that make up the design are cheaper, says the company.

10G EPON and XGPON

OneChip believes the end of 2012 will be when 10G EPON volumes start to ramp. "10G EPON is a significantly larger market than 10G GPON [XGPON]," says Weirich, pointing out that some of the largest operators such as China Telecom have backed 10G EPON.

With 10G EPON there are two flavours: the asymmetric (10Gbps downstream and 1.25Gbps upstream) and the symmetric (10Gbps bidirectional) versions.

For an asymmetric 10Gbps ONU transceiver, the laser does not need to change but the optics and electronics at the receiver do, because of the 10Gbps receive signal and because operators want 28-29dB optical link budgets so that 10G EPON can run on the same fibre plant as EPON. "This is an order of magnitude more difficult from a sensitivity perspective than for EPON," says Weirich.

There is demand for the 10G symmetric EPON but it is much lower than the asymmetric version primarily due to cost. "The ONU transceiver with its 10 Gbps laser and photo-detector is quite a bit more costly," says Weirich, complicating the PON's business case.

OneChip says it has a 10G EPON in its product roadmap, but it has not yet made any announcements or made any demonstrations to customers.

Challenges

OneChip is not aware of any other company developing a monolithic integrated design for PON transceivers, in part due to the challenge. It has to be made cheaply enough to compete with the traditional TO-can design. The key is to develop low-cost integration techniques and processes right at the start of the PIC design, he says.

The company says that it is also exploring using its PIC technology to address data centre connectivity.

OneChip Photonics at a glance

OneChip employs some 80 staff and is headquartered in Ottawa, Canada, where it has a 4,000 sq. ft. cleanroom. The start-up also has a regional office in Shenzhen, China which includes a test lab to serve regional customers.

The company is primarily a transceiver supplier and its main target customers are the tier-one system vendors that supply OLT and ONU equipment. "When you think of the big three players in China, Huawei, ZTE and Fiberhome would be among those we are targeting," says Steve Bauer, vice president of marketing and communications, as well as players such as Alcatel-Lucent and Motorola. As mentioned, the company is also considering selling its BOSA design to ONU makers.

In May 2011 the company received $18M in its latest round of funding. "We are transitioning from product development to becoming operationally ready to manufacture in volume," says Bauer.

Fabrinet and Sanmina-SCI are two contract manufacturers that the company is using for transceiver testing and assembly while it has partnerships with several other fabs for supply of wafers, wafer fabrication and silicon optical benches.

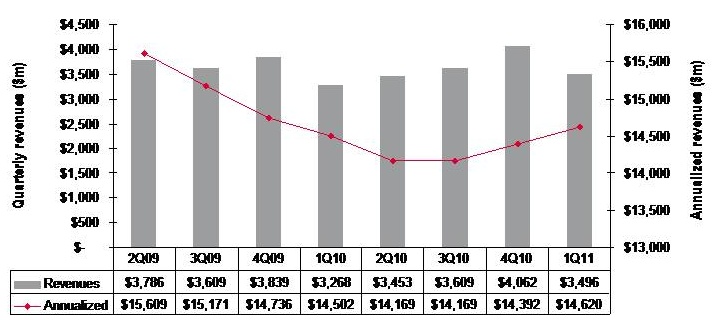

Optical networking market in rude health

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Despite recent falls in optical equipment makers’ stock, the optical networking market remains in good health with analysts predicting 6-7% growth in 2011.

For Andrew Schmitt, directing analyst for optical at Infonetics Research, unfulfilled expectations are nothing new. Optical networking is a market of single-digit yearly growth yet in the last year certain market segments have grown above average: spending on ROADM-based wavelength division multiplexing (WDM) optical network equipment, for example, has grown 20% since the first quarter of 2010.

“Every few years people get this expectation that there is going to be this hockey stick [growth] and it is not,” says Schmitt. “There has been a lot of Wall Street money moving into this sector in the latter part of 2010 and first part of this year and they have just had their expectations reset, but operationally the industry is very healthy.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate”

Andrew Schmitt, Infonetics Research

But Schmitt acknowledges that there is industry concern about the market outlook. “There have been lots of client calls in the first half of the year wanting to talk numbers,” says Schmitt. “When the market is growing rapidly there is no need for such calls but when it is uncertain, customers put more time into understanding what is going on.”

Both Infonetics and market research firm Ovum say the optical networking market grew 7% globally in the last year (2Q10 to 1Q11).

Ovum says the market reached US $3.5bn in the first quarter of 2011 and it expects 6% growth this year. “Most of the growth will come from North America—general recovery, stimulus-related spending, and LTE (Long Term Evolution)-inspired spending; and from South and Central America mostly mobile and fixed broadband-related,” says Dana Cooperson, network infrastructure practice leader at Ovum.

Ovum also notes that optical networking annualised spending for the last four quarters (2Q10-1Q11) finally went into the black with 1% growth, to reach $14.6bn. Annualised share figures are a strong indicator of longer-term market trends, says Ovum.

Market growth

Factors accounting for the growth include optical equipment demand for mobile and broadband backhaul. Carriers are also embarking on a multi-year optical upgrade to 40 and 100 Gigabit transmission over Optical Transport Network (OTN) and ROADM-based networks. Infonetics notes that ROADM spending in particular set a new high in the first quarter, rising 4% sequentially.

Ovum expects overall growth to come from metro and backbone WDM markets and from LTE. “For metro it is a combination of new builds, as DWDM continues to take over the metro core from SONET/SDH, and expansions of ROADM and 40 Gigabit,” says Cooperson. “For backbone it is a combination of retrofits for 40 and 100 Gigabit and overbuilds with 40 and 100 Gigabit coherent-optimised systems.”

Many operators are also looking at OTN switching and how it can help with network efficiency and manageability, she says, while mobile backhaul continues to be a hot spot as well at the access end of the network.

The Americas are the regions accounting for market growth whereas in Asia-Pacific and Europe, Middle East and Africa the spending remains flat.

“We’re not as bullish on Europe as I’ve heard some others are,” says Cooperson. “We expected China to slow down as capital intensities in the 34-35% seen in 2008 and 2009 were unsustainable. We saw the cooling down a bit earlier in 2010 than we had expected, but it did cool down and will continue to.”

Ovum expects Asia-Pacific as a whole to be moribund. But at least the pullbacks in China will be countered by slow growth in Japan and a big upsurge in India after a huge decline last year due to delayed 3G-related builds among other issues.

Outlook

Ovum is optimistic about the optical networking market due to continued competitive pressures and traffic growth. “We don’t think traffic growth can just continue without attention to the underlying issues related to revenue pressure, regardless of competitive pressures,” says Cooperson. “But newer optical and packet systems offer significant improvements over the old in terms of power efficiency, manageability, and of course 40 and 100 Gigabit coherent and ROADM features.”

“Most of the growth will come from North America"

Dana Cooperson, Ovum.

Many networks worldwide are also due for a core infrastructure update to benefit capacity and efficiency while many other operators are upgrading their access networks for mobile backhaul and enterprise Ethernet services.

Schmitt stresses that while it is right to talk about a 'core reboot', there are all sorts of operators that make up the market: the established carriers, those focussed on Layer 2 and Layer 3 transport, dark fibre companies and cable companies.

“Everyone has a different business so there is not a whole lot of group-think in this industry,” says Schmitt. “So when you talk about a transition to 40 and 100 Gigabit, some carriers will make that transition earlier than others because the nature of their business demands it.”

However, there are developments in equipment costs that are leading to change. “Once you get out to 2013-14, 100 Gigabit [transport] looks really good relative to 40 Gigabit and tunable XFPs at 10 Gigabit look really, really good,” says Schmitt, who believes these are going to be two dominating technologies. “People are going to use 100 Gigabit and when they can afford to throw more 10 Gigabit at the [capacity] problem, in shorter metro and regional spans, they will use tunable XFPs,” he says. “That is a whole new level in terms of driving down cost at 10 Gigabit that people haven’t factored in yet.”

Pacier change

The move to 100 Gigabit will not lead to increased spending, stresses Schmitt. Rather its significance is as a ‘mix shift’: The adoption of 100 Gigabit will shift spending from older systems to newer ones so that the technology is interesting in terms of market share shift rather than by growing overall revenues.

That said, there are areas of optical spending where capital expenditure (capex) is growing faster than the single-digit trend. These include certain competitive telco providers and dark fibre providers like AboveNet, TimeWarner Telecom and Colt. “You look at their capex year-over-year and it is increasing in some cases more over 20% a year,” says Schmitt.

He also notes that while the likes of Google, Yahoo, Microsoft and Apple do not spend on optical equipment as much as established operators such as Verizon or AT&T, their growth rate is higher. “There are sectors of the market that are growing quickly, and competition that are positioned to service those sectors successfully are going to see above-trend growth,” says Schmitt.

He highlights three areas of innovations - ‘big vectors’- that are going to change the business.

One is optical transport's move away from simple on-off keying signalling that opens up all kinds of innovation. Another is the shift in the players buying optical equipment. “A lot more of the R&D is driven by the AboveNets, Time Warners, Comcasts and the Googles and less by the old time PTTs,” says Schmitt. “That is going to change the way R&D is done.”

The third is photonic integration which Schmitt equates to the very early state of the electronics business. While Infinera has done some interesting things with integration, its latest 500 Gigabit PIC (photonic integrated circuit) is a big leap in density, he says: “It will be interesting if that sort of technology crosses over into other applications such as short- and intermediate-reach applications.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate,” says Schmitt. “These three things, when you throw them together in a pot, are going to result in some unpredictable outcomes.”

CyOptics gets $50m worth of new investors and funding

“Volume production scale is very important to having a successful business”

Ed Coringrato, CyOptics

The $50m investment in CyOptics has two elements: the amount paid by new investors in CyOptics to replace existing ones and funding for the company.

“This is different from the years-ago, traditional funding round but not all that different from what is more and more taking place,” says Ed Coringrato, CEO of CyOptics. “Fifty million is a big number but it is a ‘primary/ secondary’: the secondary is tendering out current investors that are choosing to exit, while the primary is what people think of as a traditional investment.” CyOptics has not detailed how the $50m is split between the two.

The funding is needed to bolster the company’s working capital, says Coringrato, despite CyOptics achieving over $100m in revenues in 2010. The money is required because of growth, he says: inventories the company holds are growing, there is more cash outstanding and the company’s payments are also rising.

There is also a need to invest in the company. “For the first time in a long time we are starting to make significant capital investments in our business,” says Coringrato. “We are ramping the fab, the packaging capability, and the assembly and test.”

The company is investing in R&D. At the moment 11 percent of its revenue is invested in R&D and the company wants to approach 13 percent. “That is a challenge in our industry – the investment in R&D is pretty significant,” says Coringrato. “If we are to continue to be significant and have leading-edge products, we must continue to make that investment.”

Manufacturing

CyOptics acquired Triquint Semiconductor’s optoelectronics operations in 2005, and before that Triquint had bought the optoelectronics operations of Agere Systems. This resulted in CyOptics inheriting automated manufacturing facilities and as a result it never felt the need to move manufacturing to the Far East to achieve cost benefits. CyOptics does use some contract manufacturing but its high-end products are made in-house.

“We have been focussed on automated production, cycle-time reduction and yield improvement,” says Coringrato. “The capital investment is to replicate what we have, adding more machines to get more output.”

Markets

CyOptics supplies fibre-to-the-x (FTTx) components to transmit optical subassembly (TOSA) and receive optical subassembly (ROSA) makers, optical transceiver players and board manufacturers. FTTx is an important market for CyOptics as it is a volume driver. “Volume production scale is very important to having a successful business,” says Coringrato.

The company also supplies 2.5 and 10 Gigabit-per-second (Gbps) TOSAs and ROSAs for XFP and SFP pluggable modules for the metro. “We want to play at the higher end as well as that is the where the growth opportunities are and the healthier margins,” says Coringrato.

CyOptics is also active in what it calls high-end product areas.

One area is as a supplier of components for the US defence industry. CyOptics entered the defence market in 2005. “These are custom products designed for specific applications,” says Stefan Rochus, vice president of marketing and business development. These include custom chip fabrication and packaging undertaking for defence contractors that supply the US Department of Defense. “When you look around there are not many companies that can do that,” says Rochus. One example CyOptics cites is a 1480nm pump-laser, part of a fibre-optic gyroscope for use in a satellite.

“We are shipping 40Gbps and 100Gbps coherent receivers into the PM-QPSK market”

Stefan Rochus, CyOptics

The defence market may require long development cycles but CyOptics believes that in the next few years several of its products could lead to reasonable volumes and a better average selling price than telecom components.

Another high-end product segment CyOptics is pursuing is photonic integrated circuits (PICs) using the company's indium-phosphide and planar lightwave circuit expertise.

Rochus says the company has several PIC developments including 10x10Gbps TOSAs and ROSAs as well as emerging 40GBASE-LR4 and coherent detection designs. “We are shipping 40Gbps and 100Gbps coherent receivers into the PM-QPSK market,” says Rochus.

CyOptics’ product portfolio is a good balance between high-volume and high average selling price components, says Rochus.

10x10 MSA

CyOptics is part of the recent 10X10 MSA, the 100Gbps multi-source agreement that includes Google and Brocade. “There is a follow-up high density 10x10Gbps MSA and we will be a member of this as well,” says Rochus. “This [10x10G design] is for short reach, up to 2km, but we are also shipping product for DWDM for an Nx10Gbps TOSA/ROSA solution.”

Why is CyOptics supporting the Google-backed 10x10Gbps MSA?

“The IEEE has only standardised the 100GBASE-SR10 which is 100m and the 100GBASE-LR4 which is 10km, there is a gap in the middle for [a] 2km [interface] which the MSA tries to solve,” says Rochus. “This is particularly important for the larger data centres.”

Rochus claims the 10x10Gbps design is the cheapest solution and that the volumes that will result from growth in the 10 Gigabit PON market will further reduce the component costs used for the interface. Furthermore the interface will be lower power.

That said, CyOptics is backing both interface styles, selling TOSAs and ROSAs for the 10x10Gbps interface and lasers for the 4x25Gbps-styled 100 Gigabit interfaces.

What next?

“The bigger we can get in terms of volume and revenue, the better our financials,” says Coringrato. “Potentially CyOptics is not only attractive for our preferred path, which is an IPO offering at the right time, but also I think it won't discourage others from being interested in us.”

Further reading

Jagdeep Singh's Infinera effect

Talking to gazettabyte, he reflects on the ups and downs of being a CEO, his love of running, 40 Gigabit transmission and why he is looking forward to his next role at Infinera.

"We are looking to lead the 40 Gig market, not be first to market.”

Jagdeep Singh, Infinera CEO

Ask Jagdeep Singh about how Infinera came about and there is no mistaking the enthusiasm and excitement in his voice.

During the bubble era of 2000 he started to question whether the push to all-optical networking pursued by numerous start-ups made sense. “The reason for these all-optical device companies was that they were developing the analogue functions needed,” says Singh. “Yet what operators really wanted was access to the [digital] bits.”

This led him to think about optical-to-electrical (O-E) conversion and the digital processing of signals to correct for transmission impairments. “The question then was: could this be done in a low-cost way?” says Singh. Achieving O-E conversion would also allow access to the bits for add/ drop, switching and grooming functions at the sub-wavelength level before using inverse electrical-to-optical (E-O) conversion to continue the optical transmission.

“We came at this from an orthogonal direction: building lower-cost O-E-O. Was it possible?” says Singh. “The answer was that most of the cost was in the packaging and that led us to think about photonic integration.”

Singh started out with his colleague Drew Perkins (now Infinera’s CTO) with whom he co-founded Lightera, a company acquired by Ciena in 1999. Then the two met with Dave Welch at a Christmas party in 2000. Welch had been CTO of SDL, a company just acquired by JDS Uniphase. “It was clear that he was not that happy and there were a lot of VCs (venture capitalists) chasing him,” says Singh. “He (Welch) recognised the power of what we were planning.” In January 2001 the three founded Infinera.

So why is he stepping down as CEO? The answer is to focus on long-term strategy. And perhaps to reclaim time outside work, given he has a young family.

He may even have more time for running.

Singh typically runs at least two marathons a year. “As a CEO your schedule is fully booked. There is so much stuff there is no time to think.” Running for him is quiet time. “I can get out and recharge the batteries. I find it invaluable. I can process things and it keeps the stress levels down.”

Being CEO

“There are two roles to being a CEO: running the business – the P&Ls (profit and loss statements), financials, sales – all real-time and urgent; and then there is the second part – setting the product vision: what products will be needed in two, three, four years’ time?” he says.

This second part is particularly important for Infinera given it develops products around its photonic integrated circuit (PIC) designs, requiring a longer development cycle than other optical equipment makers. “We have to get the requirements right up front,” says Singh.

And it is this part of the CEO’s role, he says, that gets trumped due to real-time tasks that must be addressed. Thus, from January, Singh will become Infinera’s executive chairman focussing exclusively on product planning. “If I had to choose [between the two roles], the longer term stuff is more appealing,” he says.

Looking back over his period as CEO, he believes his biggest achievement has been the team assembled at Infinera. “What I’ve learnt over the years is that the quality of success depends on the quality of the team.

“We started after the telecom bust,” says Singh. “There were world-class people that were never that locked in and [once on board] they knew people that they respected.” Now Infinera has a staff of 1,000, and had gone from a start-up to a publicly-listed company.

One downside of becoming a large company is that Singh regrets no longer personally knowing all his staff. “What I miss is that I knew everyone, I was part of a small team with a lot of energy,” he says. Another change is all the regulatory, legal and accounting that a public company must do. “I was also free to do and say what I wanted. Now I have to be a lot more careful.”

The Infinera effect

Asked about why Infinera is still not shipping a PIC with 40Gbps line rate channels, it is Singh-as-scrutinised-CEO that kicks in. “If we built 40 Gig purely using off-the-shelf components we’d have a product.” But he argues that the economics of 40 Gigabit-per-second (Gbps) are still not compelling. According to market research firm Ovum, he says, it will only be 2012 when 40Gbps dips below four times the cost of 10Gbps.

Indeed in Q3 2009 shipments of 40Gbps slipped. According to Ovum, this was in part due to what it calls the “Infinera effect” that is lowering the cost of existing 10Gbps technology. Only when 40Gbps is around 2.5x the cost of 10Gbps that it is likely to take off; the economic rule-of-thumb with all previous optical speed hikes.

“Our goal is to come in with a 40 Gig solution that is economically viable,” says Singh. This is what Infinera is working on with its 10x40Gbps PIC pair of chips that integrate hundreds of optical functions. “With the PIC we are looking to lead the 40 Gig market, not be first to market.”

This year also saw Infinera introduce its second class of platform, the ATN, aimed at metro networks. The platform was developed across three Infinera sites: in Silicon Valley, India and China.

Coupled with Infinera’s DTN, the ATN allows end-to-end bandwidth management of its systems. “Until now we have only played in long-haul; this now doubles the market we play in,” says Infinera's CEO. Italian operator Tiscali announced in December 2009 its plan to deploy Infinera’s systems with the ATN being deployed in 80 metro locations.

How are cheap wavelength-selective switches and tunability impacting Infinera’s business? Singh bats away the question: “We just don’t see it in our space.”

Singh agrees with Infinera’s Dave Welch’s thesis that PICs are optics’ current disruption. What developments can he cite that will indicate this is indeed happening?

There are several examples that would confirm this, he says: “PICs in adjacent devices such as routers or switches; you would need something like a PIC to reduce the power and space of such platforms.” Other areas of adoption include connecting multiple bays such as required for the largest IP core routers, and even chip-to-chip interconnect.

Surely chip-to-chip is silicon photonics not Infinera’s PICs’ based on indium phosphide technology? Is silicon photonics of interest to Infinera?

"We are an optical transport company. To generate light over vast distances requires indium phosphide,” says Singh. “But if and when there is a breakthrough in silicon to generate light efficiently, we’d want to take advantage of that.”

One wonders what ideas Singh will come up with on his two-hour runs once he can think beyond the next financial quarter.