Software-defined networking: A network game-changer?

OFC/NFOEC reflections: Part 1

"We [operators] need to move faster"

Andrew Lord, BT

Q: What was your impression of the show?

A: Nothing out of the ordinary. I haven't come away clutching a whole bunch of results that I'm determined to go and check out, which I do sometimes.

I'm quite impressed by how the main equipment vendors have moved on to look seriously at post-100 Gigabit transmission. In fact we have some [equipment] in the labs [at BT]. That is moving on pretty quickly. I don't know if there is a need for it just yet but they are certainly getting out there, not with live chips but making serious noises on 400 Gig and beyond.

There was a talk on the CFP [module] and whether we are going to be moving to a coherent CFP at 100 Gig. So what is going to happen to those prices? Is there really going to be a role for non-coherent 100 Gig? That is still a question in my mind.

"Our dream future is that we would buy equipment from whomever we want and it works. Why can't we do that for the network?"

I was quite keen on that but I'm wondering if there is going to be a limited opportunity for the non-coherent 100 Gig variants. The coherent prices will drop and my feeling from this OFC is they are going to drop pretty quickly when people start putting these things [100 Gig coherent] in; we are putting them in. So I don't know quite what the scope is for people that are trying to push that [100 Gigabit direct detection].

What was noteworthy at the show?

There is much talk about software-defined networking (SDN), so much talk that a lot of people in my position have been describing it as hype. There is a robust debate internally [within BT] on the merits of SDN which is essentially a data centre activity. In a live network, can we make use of it? There is some skepticism.

I'm still fairly optimistic about SDN and the role it might have and the [OFC/NFOEC] conference helped that.

I'm expecting next year to be the SDN conference and I'd be surprised if SDN doesn't have a much greater impact then [OFC/NFOEC 2014] with more people demoing SDN use cases.

Why is there so much excitement about SDN?

Why now when it could have happened years ago? We could have all had GMPLS (Generalised Multi-Protocol Label Switching) control planes. We haven't got them. Control plane research has been around for a long time; we don't use it: we could but we don't. We are still sitting with heavy OpEx-centric networks, especially optical.

"The 'something different' this conference was spatial-division multiplexing"

So why are we getting excited? Getting the cost out of the operational side - the software-development side, and the ability to buy from whomever we want to.

For example, if we want to buy a new network, we put out a tender and have some 10 responses. It is hard to adjudicate them all equally when, with some of them, we'd have to start from scratch with software development, whereas with others we have a head start as our own management interface has already been developed. That shouldn't and doesn't need to be the case.

Opening the equipment's north-bound interface into our own OSS (operating systems support) in theory, and this is probably naive, any specific OSS we develop ought to work.

Our dream future is that we would buy equipment from whomever we want and it works. Why can't we do that for the network?

We want to as it means we can leverage competition but also we can get new network concepts and builds in quicker without having to suffer 18 months of writing new code to manage the thing. We used to do that but it is no longer acceptable. It is too expensive and time consuming; we need to move faster.

It [the interest in SDN] is just competition hotting up and costs getting harder to manage. This is an area that is now the focus and SDN possibly provides a way through that.

Another issue is the ability to put quickly new applications and services onto our networks. For example, a bank wants to do data backup but doesn't want to spend a year and resources developing something that it uses only occasionally. Is there a bandwidth-on-demand application we can put onto our basic network infrastructure? Why not?

SDN gives us a chance to do something like that, we could roll it out quickly for specific customers.

Anything else at OFC/NFOEC that struck you as noteworthy?

The core networks aspect of OFC is really my main interest.

You are taking the components, a big part of OFC, and then the transmission experiments and all the great results that they get - multiple Terabits and new modulation formats - and then in networks you are saying: What can I build?

The networks have always been the poor relation. It has not had the great exposure or the same excitement. Well, now, the network is becoming centre stage.

As you see components and transmission mature - and it is maturing as the capacity we are seeing on a fibre is almost hitting the natural limit - so the spectral efficiency, the amount of bits you can squeeze in a single Hertz, is hitting the limit of 3,4,5,6 [bit/s/Hz]. You can't get much more than that if you want to go a reasonable distance.

So the big buzz word - 70 to 80 percent of the OFC papers we reviewed - was flex-grid, turning the optical spectrum in fibre into a much more flexible commodity where you can have wherever spectrum you want between nodes dynamically. Very, very interesting; loads of papers on that. How do you manage that? What benefits does it give?

What did you learn from the show?

One area I don't get yet is spatial-division multiplexing. Fibre is filling up so where do we go? Well, we need to go somewhere because we are predicting our networks continuing to grow at 35 to 40 percent.

Now we are hitting a new era. Putting fibre in doesn't really solve the problem in terms of cost, energy and space. You are just layering solutions on top of each other and you don't get any more revenue from it. We are stuffed unless we do something different.

The 'something different' this conference was spatial-division multiplexing. You still have a single fibre but you put in multiple cores and that is the next way of increasing capacity. There is an awful lot of work being done in this area.

I gave a paper [pointing out the challenges]. I couldn't see how you would build the splicing equipment, how you would get this fibre qualified given the 30-40 years of expertise of companies like Corning making single mode fibre, are we really going to go through all that again for this new fibre? How long is that going to take? How do you align these things?

"SDN for many people is data centres and I think we [operators] mean something a bit different."

I just presented the basic pitfalls from an operator's perspective of using this stuff. That is my skeptic side. But I could be proved wrong, it has happened before!

Anything you learned that got you excited?

One thing I saw is optics pushing out.

In the past we saw 100 Megabit and one Gigabit Ethernet (GbE) being king of a certain part of the network. People were talking about that becoming optics.

We are starting to see optics entering a new phase. Ten Gigabit Ethernet is a wavelength, a colour on a fibre. If the cost of those very simple 10GbE transceivers continues to drop, we will start to see optics enter a new phase where we could be seeing it all over the place: you have a GigE port, well, have a wavelength.

[When that happens] optics comes centre stage and then you have to address optical questions. This is exciting and Ericsson was talking a bit about that.

What will you be monitoring between now and the next OFC?

We are accelerating our SDN work. We see that as being game-changing in terms of networks. I've seen enough open standards emerging, enough will around the industry with the people I've spoken to, some of the vendors that want to do some work with us, that it is exciting. Things like 4k and 8k (ultra high definition) TV, providing the bandwidth to make this thing sensible.

"I don't think BT needs to be delving into the insides of an IP router trying to improve how it moves packets. That is not our job."

Think of a health application where you have a 4 or 8k TV camera giving an ultra high-res picture of a scan, piping that around the network at many many Gigabits. These type of applications are exciting and that is where we are going to be putting a bit more effort. Rather than the traditional just thinking about transmission, we are moving on to some solid networking; that is how we are migrating it in the group.

When you say open standards [for SDN], OpenFlow comes to mind.

OpenFlow is a lovely academic thing. It allows you to open a box for a university to try their own algorithms. But it doesn't really help us because we don't want to get down to that level.

I don't think BT needs to be delving into the insides of an IP router trying to improve how it moves packets. That is not our job.

What we need is the next level up: taking entire network functions and having them presented in an open way.

For example, something like OpenStack [the open source cloud computing software] that allows you to start to bring networking, and compute and memory resources in data centres together.

You can start to say: I have a data centre here, another here and some networking in between, how can I orchestrate all of that? I need to provide some backup or some protection, what gets all those diverse elements, in very different parts of the industry, what is it that will orchestrate that automatically?

That is the kind of open theme that operators are interested in.

That sounds different to what is being developed for SDN in the data centre. Are there two areas here: one networking and one the data centre?

You are quite right. SDN for many people is data centres and I think we mean something a bit different. We are trying to have multi-vendor leverage and as I've said, look at the software issues.

We also need to be a bit clearer as to what we mean by it [SDN].

Andrew Lord has been appointed technical chair at OFC/NFOEC

Further reading

Part 2: OFC/NFOEC 2013 industry reflections, click here

Part 3: OFC/NFOEC 2013 industry reflections, click here

Part 4: OFC/NFOEC industry reflections, click here

Part 5: OFC/NFEC 2013 industry reflections, click here

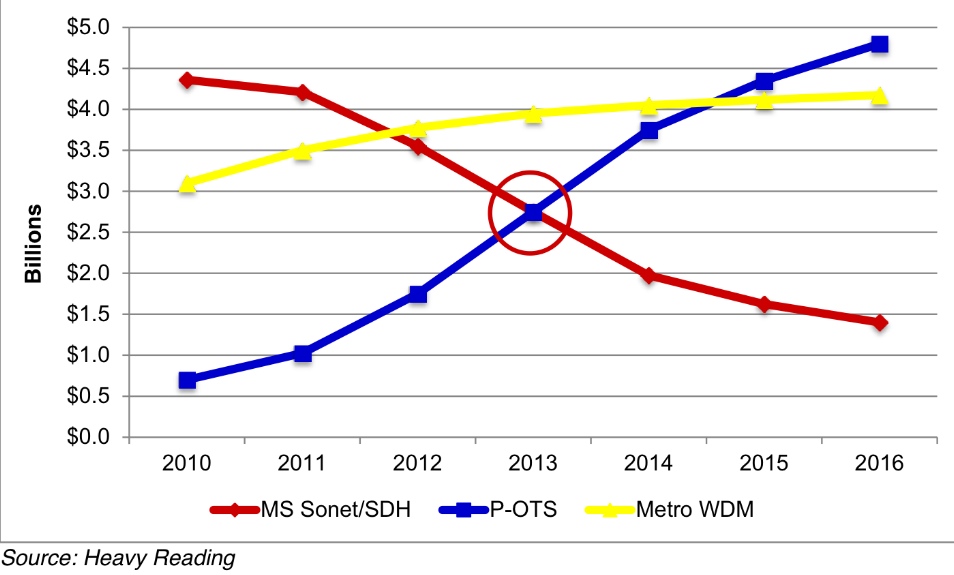

P-OTS 2.0: 60s interview with Heavy Reading's Sterling Perrin

Q: Heavy Reading claims the metro packet optical transport system (P-OTS) market is entering a new phase. What are the characteristics of P-OTS 2.0 and what first-generation platform shortcomings does it address?

A: I would say four things characterise P-OTS 2.0 and separate 2.0 from the 1.0 implementations:

- The focus of packet-optical shifts from time-division multiplexing (TDM) functions to packet functions.

- Pure-packet implementations of P-OTS begin to ramp and, ultimately, dominate.

- Switched OTN (Optical Transport Network) enters the metro, removing the need for SONET/SDH fabrics in new elements.

- 100 Gigabit takes hold in the metro.

The last two points are new functions while the first two address shortcomings of the previous generation. P-OTS 1.0 suffered because its packet side was seen as sub-par relative to Ethernet "pure plays" and also because packet technology in general still had to mature and develop - such as standardising MPLS-TP (Multiprotocol Label Switching - Transport Profile).

Your survey's key findings: What struck Heavy Reading as noteworthy?

The biggest technology surprise was the tremendous interest in adding IP/MPLS functions to transport. There was a lot of debate about this 10 years ago. Then the industry settled on a de facto standard that transport includes layers 0-2 but no higher. Now, it appears that the transport definition must broaden to include up to layer 3.

A second key finding is how quickly SONET/SDH has gone out of favour. Going forward, it is all about packet innovation. We saw this shift in equipment revenues in 2012 as SONET/SDH spend globally dropped more than 20 percent. That is not a one-time hit - it's the new trend for SONET/SDH.

Heavy Reading argues that transport has broadened in terms of the networking embraced - from layers 0 (WDM) and 1 (SONET/SDH and OTN) to now include IP/MPLS. Is the industry converging on one approach for multi-layer transport optimisation? For example, IP over dense WDM? Or OTN, Carrier Ethernet 2.0 and MPLS-TP? Or something else?

We did not uncover a single winning architecture and it's most likely that operators will do different things. Some operators will like OTN and put it everywhere. Others will have nothing to do with OTN. Some will integrate optics on routers to save transponder capital expenditure, but others will keep hardware separate but tightly link IP and optical layers via the control plane. I think it will be very mixed.

You talk about a spike in 100 Gigabit metro starting in 2014. What is the cause? And is it all coherent or is a healthy share going to 100 Gigabit direct detection?

Interest in 100 Gigabit in the metro exceeds interest in OTN in the metro - which is different from the core, where those two technologies are more tightly linked.

Cloud and data centre interconnect are the biggest drivers for interest in metro 100 Gig but there are other uses as well. We did not ask about coherent versus direct in this survey, but based on general industry discussions, I'd say the momentum is clearly around coherent at this stage - even in the metro. It does not seem that direct detect 100 Gig has a strong enough cost proposition to justify a world with two very different flavours of 100 Gig.

What surprised you from the survey's findings?

It was really the interest-level in IP functionality on transport systems that was the most surprising find.

It opens up the packet-optical transport market to new players that are strongest on IP and also poses a threat to suppliers that were good at lower layers but have no IP expertise - they'll have to do something about that.

Heavy Reading surveyed 114 operators globally. All those surveyed were operators; no system vendors were included. The regional split was North America - 22 percent, Europe - 33 percent, Asia Pacific - 25 percent, and the rest of the world - Latin America mainly - 20 percent.

JDSU's Brandon Collings on silicon photonics, optical transport & the tunable SFP+

JDSU's CTO for communications and commercial optical products, Brandon Collings, discusses reconfigurable optical add/drop multiplexers (ROADMs), 100 Gigabit, silicon photonics, and the status of JDSU's tunable SFP+.

"We have been continually monitoring to find ways to use the technology [silicon photonics] for telecom but we are not really seeing that happen”

Brandon Collings, JDSU

Brandon Collings highlights two developments that summarise the state of the optical transport industry.

The industry is now aligned on the next-generation ROADM architecture of choice, while experiencing a ’heavy component ramp’ in high-speed optical components to meet demand for 100 Gigabit optical transmission.

The industry has converged on the twin wavelength-selective switch (WSS) route-and-select ROADM architecture for optical transport. "This is in large networks and looking forward, even in smaller sized networks," says Collings.

In a route-and-select architecture, a pair of WSSes reside at each degree of the ROADM. The second WSS is used in place of splitters and improves the overall optical performance by better suppressing possible interference paths.

JDSU showcased its TrueFlex portfolio of components and subsystems for next-generation ROADMs at the recent European Conference on Optical Communications (ECOC) show. The company first discussed the TrueFlex products a year ago. "We are now in the final process of completing those developments," says Collings.

Meanwhile, the 100 Gigabit-per-second (Gbps) component market is progressing well, says Collings. The issues that interest him include next-generation designs such as a pluggable 100Gbps transmission form factor.

Direct detection and coherent

JDSU remains uncertain about the market opportunities for 100Gbps direct-detection solutions for point-to-point and metro applications. "That area remains murky," says Collings. "It is clearly an easy way into 100 Gig - you don't have to have a huge ASIC developed - but its long-term prospects are unclear."

The price point of 100Gbps direct-detection, while attractive, is competing against coherent transmission solutions which Collings describes as volatile. "As coherent becomes comparable [in cost], the situation will change for the 4x25 Gig [direct detection] quite quickly," he says. "Coherent seems to be the long-term, robust cost-effective way to go, capturing most of the market."

At present, coherent solutions are for long-haul that require a large, power-consuming ASIC. Equally the accompanying optical components - the lasers and modulators - are also relatively large. For the coherent metro market, the optics must become cheaper and smaller as must the coherent ASIC.

"If you are looking to put that [coherent ASIC and optics] into a CFP or CFP2, the problem is based on power; cost is important but power is the black-and-white issue," says Collings. Engineers are investigating what features can be removed from the long-haul solution to achieve the target 15-20W power consumption. "That is pretty challenging from an ASIC perspective and leaves little-to-no headroom in a pluggable," says Collings.

The same applies to the optics. "Is there a lesser set of photonics that can sit on a board that is much lower cost and perhaps has some weaker performance versus today's high-performance long-haul?" says Collings. These are the issues designers are grappling with.

Silicon photonics

Another area in flux is the silicon photonics marketplace. "It is a very fluid and active area," says Collings. "We are not highly active in the area but we are very active with outside organisations to keep track of its progress, its capabilities and its overall evolution in terms of what the technology is capable of."

The silicon photonics industry has shifted towards datacom and interconnect technology in the last year, says Collings. The performance levels silicon photonics achieves are better suited to datacom than telecom's more demanding requirements. "We have been continually monitoring to find ways to use the technology for telecom but we are not really seeing that happen,” says Collings.

Tunable SFP+

JDSU demonstrated its tunable laser in an SFP+ pluggable optical module at the ECOC exhibition.

The company was first to market with the tunable XFP, claiming it secured JDSU an almost two-year lead in the marketplace. "We are aiming to repeat that with the SFP+," says Collings.

The SFP+ doubles a line card's interface density compared to the XFP module. The SFP+ supports both 10Gbps client-side and wavelength-division multiplexing (WDM) interfaces. "Most of the cards have transitioned from supporting the XFP to the SFP+," says Collings. This [having a tunable SFP+] completes that portfolio of capability."

JDSU has provided samples of the tunable pluggable to customers. "We are working with a handful of leading customers and they typically have a preference on chirp or no-chirp [lasers], APD [avalanche photo-diode] or no APD, that sort of thing," says Collings.

JDSU has not said when it will start production of the tunable SFP+. "It won't be long," says Collings, who points out that JDSU has been demonstrating the pluggable for over six months.

The company plans a two-stage rollout. JDSU will launch a slightly higher power-dissipating tunable SFP+ "a handful of months" before the standard-complaint device. "The SFP+ standard calls for 1.5W but for some customers that want to hit the market earlier, we can discuss other options," says Collings.

Further reading

60-second interview with .... Dell'Oro's Jimmy Yu

"For the year, it is going to be a fivefold growth rate [for 100 Gig transport]."

Jimmy Yu, Dell'Oro

Q: That fact that the market is down 5 percent on a year ago. Why is this?

A: There are a few factors. First, the macro-economy in Europe continues to get worse; that causes a slowdown.

A second factor is that in North America there was a decline in the second quarter, which is pretty unusual. Part of it, we think, might be that operators have caught up with a lot of the spending to increase broadband, after adding [to the network] for a couple of good years.

The third issue is that the China market has had a really slow start. And while there has been talk about the Chinese market softening, it seems that the CapEx [capital expenditure] is there for a strong second half.

What categories does Dell'Oro include when it talks about optical transport?

There are two main pieces: WDM [wavelength division multiplexing], both metro and long haul, and the multi-service multiplexer used for aggregation. The third piece, which is really small, is optical switching - optical cross-connect used in the core and lately more so in the metro.

According to Dell'Oro, wavelength division multiplexing was up 5 percent in the first half of 2012 compared to the same period a year ago, due to demand for 40 Gig and 100 Gig. What is happening in these two markets?

At 100 Gig we are at an inflection point where demand growth rates are really high. We've got a doubling in demand and shipments quarter-on-quarter [in the second quarter]. For the year, it is going to be a fivefold growth rate.

Also the 40 Gig is still growing. It has been around for a few years so its growth rate is not as strong [as 100 Gig transport] but it is still a significant part of the market.

Has the market settled on particular modulation scheme, especially at 40 Gig?

For 100 Gig the majority [deployed] is coherent. There is one company at least, ADVA Optical Networking, which is coming out with its direct-detection scheme for 100 Gig. This has now been shipping for one quarter. There is a market for the price point and the lower-span link of direct-detection.

For 40 Gig there is still a mix of modulations. Vendors coming out with 100 Gig coherent are also coming out with 40 Gig coherent options. So coherent at 40 Gig is now approaching half of the total market and is happening pretty quickly.

As for [40 Gig] DQPSK [differential quadrature phase-shift keying] modulation, it is probably a little bit more than DPSK [differential phase-shift keying].

You also report a rise in the adoption of optical packet products and that it contributed close to one-third of the optical market revenues in the first half 2012. Why is that?

The optical packet platform is a wider definition than just packet optical transport systems (P-OTS).

One reason why optical packet is growing is that with traditional P-OTS, you have cross-connect and switching capabilities in a WDM system so as you go to higher 40 and 100 Gig wavelengths you want some bandwidth management in that system.

Another thing is that people are trying to make the aggregation layer - the traditional SONET/SDH - more Ethernet friendly and MPLS-TP [multiprotocol label switching, transport profile] is gaining traction.

Combined, we are seeing this optical packet market has grown 12 percent year-on-year in the second quarter whereas the overall market has declined.

Dell'Oro said Huawei has 20 percent market share, which other vendors have double-digit market share?

Besides Huawei, the other vendors with double-digit percentage for the quarter - in order - are ZTE, Alcatel-Lucent and Ciena.

Did you see anything in this latest study that was surprising?

There was nothing in this quarter but I saw it last quarter. The legacy equipment – traditional SONET/SDH – is declining. Most of the market decline for optical is in legacy.

SONET/SDH sales in the second quarter of 2012 declined by 20 percent year-on-year. It is finally happening: the market is shifting away from SONET/SDH.

Challenges, progress & uncertainties facing the optical component industry

In recent years the industry has moved from direct detection to coherent transmission and has alighted on a flexible ROADM architecture. The result is a new level in optical networking sophistication. OFC/NFOEC 2012 will showcase the progress in these and other areas of industry consensus as well as shining a spotlight on issues less clear.

Optical component players may be forgiven for the odd envious glance towards the semiconductor industry and its well-defined industry dynamics.

The semiconductor industry has Moore’s Law that drives technological progress and the economics of chip-making. It also experiences semiconductor cycles - regular industry corrections caused by overcapacity and excess inventory. The semiconductor industry certainly has its challenges but it is well drilled in what to expect.

Optical challenges

The optical industry experienced its own version of a semiconductor cycle in 2010-11 - strong growth in 2010 followed by a correction in 2011. But such market dynamics are irregular and optical has no Moore's Law.

Optical players must therefore work harder to develop components to meet the rapid traffic growth while achieving cost efficiencies, denser designs and power savings.

Such efficiencies are even more important as the marketplace becomes more complex due to changes in the industry layers above components. The added applications layer above networks was highlighted in the OFC/NFOEC 2012 news analysis by Ovum’s Karen Liu. The analyst also pointed out that operators’ revenues and capex growth rates are set to halve in the years till 2017 compared to 2006-2010.

Such is the challenging backdrop facing optical component players.

Consensus

Coherent has become the defacto standard for long-haul high-speed transmission. Optical system vendors have largely launched their 100Gbps systems and have set their design engineers on the next challenge: addressing designs for line rates beyond 100Gbps.

Infinera detailed its 500Gbps super-channel photonic integrated circuit last year. At OFC/NFOEC it will be interesting to learn how other equipment makers are tackling such designs and what activity and requests optical component vendors are seeing regarding the next line rates after 100Gbps.

Meanwhile new chip designs for transport and switching at 100Gbps are expected at the show. AppliedMicro is sampling its gearbox chip that supports 100 Gigabit Ethernet and OTU4 optical interfaces. More announcements should be expected regarding merchant 100Gbps digital signal processing ASIC designs.

An architectural consensus for wavelength-selective switches (WSSes) - the key building block of ROADMs - are taking shape with the industry consolidating on a route-and-select architecture, according to analysts.

Gridless - the ROADM attribute that supports differing spectral widths expected for line rates above 100Gbps - is a key characteristic that WSSes must support, resulting in more vendors announcing liquid crystal on silicon designs.

Client-side 40 and 100 Gigabit Ethernet (GbE) interfaces have a clearer module roadmap than line-side transmission. After the CFP comes the CFP2 and CFP4 which promise denser interfaces and Terabit capacity blades. Module form factors such as the QSFP+ at 40GbE and in time 100GbE CFP4s require integrated photonic designs. This is a development to watch for at the show.

Others areas to note include tunable-laser XFPs and even tunable SFP+, work on which has already been announced by JDS Uniphase.

Lastly, short-link interfaces and in particular optical engines is another important segment that ultimately promises new system designs and the market opportunity that will unleash silicon photonics.

Optical engines can simplify high-speed backplane designs and printed circuit board electronics. Electrical interfaces moving to 25Gbps is seen as the threshold trigger when switch makers decide whether to move their next designs to an optical backplane.

The Optical Internetworking Forum will have a Physical and Link Layer (PLL) demonstration to showcase interoperability of the Forum’s Common Electrical Interface (CEI) 28Gbps Very Short Reach (VSR) chip-to-module electrical interfaces, as well as a demonstration of the CEI-25G-LR backplane interface.

Companies participating in the interop include Altera, Amphenol, Fujitsu Optical Components, Gennum, IBM, Inphi, Luxtera, Molex, TE Connectivity and Xilinx.

Altera has already unveiled a FGPA prototype that co-packages 12x10Gbps transmitter and receiver optical engines alongside its FPGA.

Uncertainties

OFC/NFOEC 2012 also provides an opportunity to assess progress in sectors and technology where there is less clarity. Two sectors of note are next-generation PON and the 100Gbps direct-detect market.

For next-generation PON, several ideas are being pursued, faster extensions of existing PON schemes such as a 40Gbps version of the existing time devision multiplexing PON schemes, 40G PON based on hybrid WDM and TDM schemes, WDM-PON and even ultra dense WDM-PON and OFDM-based PON schemes.

The upcoming show will not answer what the likely schemes will be but will provide an opportunity to test what the latest thinking is.

The same applies for 100 Gigabit direct detection.

There are significant cost advantages to this approach and there is an opportunity for the technology in the metro and for data centre connectivity. But so far announcements have been limited and operators are still to fully assess the technology. Further announcements at OFC/NFOEC will highlight the progress being made here.

The article has been written as a news analysis published by the organisers before this year's OFC/NFOEC event.