Telcos eye servers & software to meet networking needs

- The Network Functions Virtualisation (NFV) initiative aims to use common servers for networking functions

- The initiative promises to be industry disruptive

"The sheer massive [server] volumes is generating an innovation dynamic that is far beyond what we would expect to see in networking"

"The sheer massive [server] volumes is generating an innovation dynamic that is far beyond what we would expect to see in networking"

Don Clarke, NFV

Telcos want to embrace the rapid developments in IT to benefit their networks and operations.

The Network Functions Virtualisation (NFV) initiative, set up by the European Telecommunications Standards Institute (ETSI), has started work to use servers and virtualisation technology to replace the many specialist hardware boxes in their networks. Such boxes can be expensive to maintain, consume valuable floor space and power, and add to the operators' already complex operations support systems (OSS).

"Data centre technology has evolved to the point where the raw throughput of the compute resources is sufficient to do things in networking that previously could only be done with bespoke hardware and software," says Don Clarke, technical manager of the NFV industry specification group, and who is BT's head of network evolution innovation. "The data centre is commoditising server hardware, and enormous amounts of software innovation - in applications and operations - is being applied.”

"Everything above Layer 2 is in the compute domain and can be put on industry-standard servers"

The operators have been exploring independently how IT technology can be applied to networking. Now they have joined forces via the NFV initiative.

"The most exciting thing about the technology is piggybacking on the innovation that is going on in the data centre," says Clarke. "The sheer massive volumes is generating an innovation dynamic that is far beyond what we would expect to see in networking."

Another key advantage is that once networks become software-based, enormous amounts of flexibility results when creating new services, bringing them to market quickly while also reducing costs.

NFV and SDN

The NFV initiative is being promoted as a complement to software-defined networking (SDN).

The complementary relationship between NFV and SDN. Source: NFV.

The complementary relationship between NFV and SDN. Source: NFV.

SDN is focussed on control mechanisms to reconfigure networks that separate the control plane and the data plane. The transport network can be seen as dumb pipes with the control mechanisms adding the intelligence.

“There are other areas of the network where there is intrinsic complexity of processing rather than raw throughput,” says Clarke.

These include firewalls, session border controllers, deep packet inspection boxes and gateways - all functions that can be ported onto servers. Indeed, once running as software on servers such networking functions can be virtualised.

"Everything above Layer 2 is in the compute domain and can be put on industry-standard servers,” says Clarke. This could even include core IP routers but clearly that is not the best use of general-purpose computing, and the initial focus will be equipment at the edge of the network.

Clarke describes how operators will virtualise network elements and interface them to their existing OSS systems. “We see SDN as a longer journey for us,” he says. “In the meantime we want to get the benefits of network virtualisation alongside existing networks and reusing our OSS where we can.”

NFV will first be applied to appliances that lend themselves to virtualisation and where the impact on the OSS will be minimal. Here the appliance will be loaded as software on a common server instead of current bespoke systems situated at the network's end points. “You [as an operator] can start to draw a list of target things as to what will be of most interest,” says Clarke.

Virtualised network appliances are not a new concept and examples are already available on the market. Vanu's software-based radio access network technology is one such example. “What has changed is the compute resources available in servers is now sufficient, and the volume of servers [made] is so massive compared to five years ago,” says Clarke

The NFV forum aims to create an industry-wide understanding as to what the challenges are while ensuring that there are common tools for operators that will also increase the total available market.

Clarke stresses that the physical shape of operators' networks - such as local exchange numbers - will not change greatly with the uptake of NFV. “But the kind of equipment in those locations will change, and that equipment will be server-based," says Clarke.

"One of the things the software world has shown us is that if you sit on your hands, a player comes out of nowhere and takes your business"

One issue for operators is their telecom-specific requirements. Equipment is typically hardened and has strict reliability requirements. In turn, operators' central offices are not as well air conditioned as data centres. This may require innovation around reliability and resilience in software such that should a server fail, the system adapts and the server workload is moved elsewhere. The faulty server can then be replaced by an engineer on a scheduled service visit rather than an emergency one.

"Once you get into the software world, all kinds of interesting things that enhance resilience and reliability become possible," says Clarke.

Industry disruption

The NFV initiative could prove disruptive for many telecom vendors.

"This is potentially massively disruptive," says Clarke. "But what is so positive about this is that it is new." Moreover, this is a development that operators are flagging to vendors as something that they want.

Clarke admits that many vendors have existing product lines that they will want to protect. But these vendors have unique telecom networking expertise which no IT start-up entering the field can match.

"It is all about timing," says Clarke. "When do they [telecom vendors] decisively move their product portfolio to a software version is an internal battle that is happening right now. Yes, it is disruptive, but only if they sit on their hands and do nothing and their competitors move first."

Clarke is optimistic about to the vendors' response to the initiative. "One of the things the software world has shown us is that if you sit on your hands, a player comes out of nowhere and takes your business," he says.

Once operators deploy software-based network elements, they will be able to do new things with regard services. "Different kinds of service profiles, different kinds of capabilities and different billing arrangements become possible because it is software- not hardware-based."

Work status

The NFV initiative was unveiled late last year with the first meeting being held in January. The initiative includes operators such as AT&T, BT, Deutsche Telekom, Orange, Telecom Italia, Telefonica and Verizon as well as telecoms equipment vendors, IT vendors and technology providers.

One of the meeting's first tasks was to identify the issues to be addressed to enable the use of servers for telecom functions. Around 60 companies attended the meeting - including 20-odd operators - to create the organisational structure to address these issues.

Two experts groups - on security, and on performance and portability - were set up. “We see these issues as key for the four working groups,” says Clarke. These four working groups cover software architecture, infrastructure, reliability and resilience, and orchestration and management.

Work has started on the requirement specifications, with calls between the members taking place each day, says Clarke. The NFV work is expected to be completed by the end of 2014.

Further information:

White Paper: Network Functions Virtualisation: An Introduction, Benefits, Enablers, Challenges & Call for Action, click here

Fibre-to-the-NPU: optics reshapes the IP core router

Start-up Compass Electro-Optical Systems has announced an IP core router based on a chip with a Terabit-plus optical interface.

Asaf Somekh, vice president of marketing, showing Gazettabyte Compass-EOS's novel icPhotonics chip

Asaf Somekh, vice president of marketing, showing Gazettabyte Compass-EOS's novel icPhotonics chip

Having an optical interface linking directly to the chip, which includes a merchant network processor, simplifies the system design and enables router features such as real output queuing. The r10004 IP router is in production and is already deployed in an operator's network.

The company's icPhotonics chip integrates 168, 8 Gigabit VCSELs and 168 photodetectors for a bandwidth of 1.344 Terabit-per-second (Tbps) each direction. Eight of the chips are connected in a full mesh, doing away with the need for a router's switch fabric and mid-plane used to interconnect the router cards.

The resulting architecture saves power, space and cost, says Asaf Somekh, vice president of marketing at Compass-EOS. The start-up estimates that its platform's total cost of ownership over five years is a quarter to a third of existing IP core routers.

The high-bandwidth optical links will also be used to connect multiple platforms, enabling operators to add routing resources as required. Compass-EOS is coming to market with a 6U-high standalone platform but says it will scale up to 21 platforms to appear as one logical router.

The 800Gbps-capacity r10004 comes with 2x100 Gigabit-per-second (Gbps) and 20x10Gbps line cards options. The platform has real output queuing where all the input ports' packets are queued with quality of service applied prior to the exit port. The router also supports software-defined networking (SDN) that enables external control of traffic routing.

The company has its own clean room where it makes its optical interface. Compass-EOS has also developed its own ASICs and the router software for the r10004.

Somekh says developing the optical interface has been challenging, requiring years of development working with the Fraunhofer Institute and Tel-Aviv University. One challenge was developing a glue to fix the VCSELs on top of the silicon.

The start-up has raised US $120M with investors such as Cisco Systems, Deutsche Telekom and Comcast as well as several venture capitalist firms.

icPhotonics technology

Compass-EOS refers to its optical interface IC as silicon photonics but a more accurate description is integrated silicon-optics; silicon itself is not used as a medium for light. But its use of embedded optics to the chip has created a disruptive system.

The optical-interconnect addresses two chip design challenges: signal integrity for long transmission lengths and chip input/output (I/O).

With high-speed interfaces, achieving signal integrity across a high-speed line card and between boards is challenging. Routers use a midplane and switch fabric to connect the the router cards within a platform and parallel optics to connect chassis.

Compass-EOS has taken board-mounted optics one step further and integrated VCSELs and photodetectors to the packaged chip. This simplifies the platform by connecting cards using a mesh architecture, and allows scaling by linking systems.

The chip window shows the VCSELs and photodetectors Source: Compass-EOS

The chip window shows the VCSELs and photodetectors Source: Compass-EOS

The design also addresses chip I/O issues. "The I/O density is about 30x higher than traditional solutions and the gap will grow in future," says Somekh.

Directly attaching the optical interconnect to the CMOS chip overcomes limitations imposed by ball grid array and printed circuit board (PCB) technologies.

Typically data is routed from the host PCB to an ASIC via a ball grid array matrix which has a ball pitch of 0.8mm. Shrinking this further is non-trivial given PCB signal integrity issues. Moreover, each electrical serdes (serialiser/ deserialiser) for data I/O uses at least eight bumps (transmit, receive, signal and ground) occupying a cell of 3.2×1.6 mm. For a 10Gbps device the resulting duplex data density is 2Gbps/mm2, increasing to 5Gbps/mm2 if a 25Gbps device is used, according to Compass-EOS.

The start-up says its optical-interconnect achieves a chip I/O of 61Gbps/mm2. "This will increase to 243Gbps/mm2 once we move to 32Gbps."

The resulting design uses 10 percent of the total CMOS area for I/O. "This is a more efficient chip design," says Somekh. "Most of the silicon is used for logic tasks."

The serdes on chip still need to interface to hundreds of 8Gbps channels. And moving to 32Gbps will present a greater challenge. In comparison, silicon photonics promises to simplify the coupling of optics and electronics.

Another design challenge is that the VCSELs are co-packaged with a large chip consuming 30-50W and generating heat. The design needs to make sure that the operating temperature of the VCSELs is not affected by the heat from the chip.

This is another promised advantage of silicon photonics where the operating temperature of the optics and silicon are matched.

Analysts' perspective

Gazettabyte asked two analysts - IDC's Vernon Turner and ACG Research's Eve Griliches - about the significance of Compass-EOS's announcement. The analysts were also asked for their views on the router's modularity, the total cost of ownership claims, the support for SDN and real output queueing, and whether the platform will gain market share from the IP core router incumbents.

IDC

Vernon Turner, senior vice president & general manager enterprise computing, network, telecom, storage, consumer and infrastructure.

One of the hardest places to innovate in the ICT (information and communications technology) world is at or around the speed of light. Anytime you can make things run faster, the last hurdle tends to be the speed by which things travel over an optical network.

Therefore, to see something that changes the form factor of a network router and innovates at the interconnect speed, it may be able to disrupt a significant part of the network industry.

"Separating the interconnect with the physical building block is huge. It means that you scale the pieces that you need, when and where you want them; this is not just a repackaging announcement"

Building the capacity of a router as needed is great for service providers and large enterprises since you deploy capacity only as you need it. Second, by using a photonics interconnect, the speed and distance over which two devices can sit is enhanced greatly, changing the way one builds network infrastructures.

Separating the interconnect with the physical building block is huge. It means that you scale the pieces that you need, when and where you want them; this is not just a repackaging announcement.

Regarding the total-cost-of-ownership claims, if these are valid, they are of a magnitude that does fit into a 'disruptive innovation' class where it will deliver network services to an underserved market and create new network services markets.

SDN is the latest buzzword [regarding the router's support for SDN]. But it is the last part of the virtualised data centre as the compute and I/O have already been figured out. SDN is not new, but the need to separate the data plane from the control plane for the service provider industry means that they can begin to create network services through virtualisation without impacting the network performance, something that already happens in server and storage performance.

Existing core router vendors use their own ASIC designs as the last-stop differentiation, so to do this [as Compass-EOS has done] on merchant silicon could have wide implications on router commoditisation, or at least at a faster rate than current trends.

ACG Research

Eve Griliches, vice president of optical networking

As to the significance of the announcement, it is not huge in the scheme of things, but it does bring the optical component use of replacing a backplane to market earlier than what has been quoted to ACG Research.

"Virtual output queueing is a smart way to do quality of service"

In theory, the router should be a smaller footprint which results in better total cost of ownership due to the optical modules. The advantage with this optical patch-panel approach is that it allows a much higher bandwidth to cross the backplane which is now an optical interconnect. That means you don't have to do as much flow control, or drop as many packets, or keep the utilization of the router so low. You can bring up the utilisation rate from let's say 15 percent to maybe 25 percent or higher. All that results in lower total cost of ownership in theory.

SDN in a bit nebulous. Virtual output queueing is a smart way to do quality of service, but there are key software features like how many BGP (border gateway protocol) peers are supported, multicast capability, as well as signaling for MPLS (multiprotocol label switching), do they support RSVP-TE (resource reservation protocol - traffic engineering) or LDP (label distribution protocol)? Or both? Building a real router still takes years of work.

Faster interconnects are the way to go across routing and optical platforms, period. This [Compass-EOS platform] can help. Do I see this optical piece fitting nicely into an already existing router? Yes. I think if that doesn't happen, they will have a bit of an uphill battle nudging the incumbents.

On the other hand, if full router functionality is not needed at some junctures, as we've seen with the LSR (label switch router) technology, then they may have a place in the network. But operators don't like to play around with their routed network too much, so it may be greenfield application that are mostly available to them [Compass-EOS] initially.

Optical components enter an era of technology-pull

Gazettabyte asked ADVA Optical Networking, Ciena, Cisco Systems and Ovum about their impressions following the recent OFC/NFOEC 2012 exhibition and conference.

OFC/NFOEC reflections: Part 2

"As the economy continues to navigate its way through yet another very difficult period, it was good to see so many companies innovating and introducing solutions."

"As the economy continues to navigate its way through yet another very difficult period, it was good to see so many companies innovating and introducing solutions."

Massimo Prati, Cisco Systems

Massimo Prati, Cisco Systems

For Cisco Systems, 100 Gigabit was a key focus at the show. "There were many system and component vendors, including Cisco, demonstrating newly available, economically feasible 100 Gig innovations," says Massimo Prati, vice president and general manager for Cisco.

Linking data centres was another conference theme. "Inter-data centre connectivity continues to focus on scalable and simple solutions in long-haul and metro networks connecting data centres worldwide." Cisco believes metro 100 Gigabit deployments will become prevalent in 2013 and 2014, especially if low‐cost coherent technology becomes available.

"A dedicated workshop focused on data centre architectures, held on the first day of the conference, was heavily attended," says Prati. "So certainly the link between cloud and optical is being established and is a key driver for high-speed transport networks."

Another conference theme was interconnect within the data centre, and the need for photonic integration for low‐cost, low‐power links, says Prati: "From a Cisco standpoint, several of our customers were pleasantly surprised by our recently completed acquisition of Lightwire, which develops advanced optical interconnect technology for high-speed networking applications." Lightwire is a silicon photonics startup that Cisco acquired recently for US $271 million.

What Cisco says it learned from OFC/ NFOEC was that service providers are planning 100Gbps deployments within the next 12 months and are looking at second- and third-generation solutions. "There is quite a bit of energy around future upgrades to 400 Gig and one Terabit transport solutions, but service providers continue to monitor if and how these solutions will operate within their existing fibre plants."

Prati expects more industry consolidation. "With the influx of 100 Gig solutions, it appears we may be ripe for further consolidation within the industry, particularly further down the technology food chain," he says.

He also remains optimistic about the industry's prospects.

"We believe that the excitement around high-speed, long-haul transport, combined with cloud and data centre innovation, continues to fuel a lot of new product solutions and architectures," he says. "Content providers like Google and Facebook have clearly expressed interest in optical technologies addressing their issues with bandwidth demands and need for high-speed interconnect for their data centres."

Joe Berthold, Ciena

Whereas last year there was much discussion about of the next rate for Ethernet - 400 Gig or one Terabit - this year 400 Gigabit had most mindshare, says Joe Berthold, vice president of network architecture at Ciena. "I barely heard any mention of one Terabit in the context of a contest with 400 Gigabit," he says.

"I could hear some rumblings about alternative form factors – which might lead to fragmentation of the market"

"I could hear some rumblings about alternative form factors – which might lead to fragmentation of the market"

Joe Berthold, Ciena

400 Gigabit was given a boost with the line-side transmission component announcements. Ciena announced its WaveLogic3 and Alcatel-Lucent detailed its Photonic Service Engine.

Another noteworthy development was the buzz around silicon photonics, stirred in part by Cisco's Lightwire acquisition. "Silicon photonics has passed from a technology of research interest to one that has progressed to serious development," says Berthold. "Data centre interconnects look like a promising initial application."

There was no developments at the show that surprised Berthold. But he is concerned about the potential for proliferation of 100 Gigabit client-side form factors, especially for pluggable modules.

"I am going under the assumption that there is still broad industry support for the CFP progression - from the current CFP to a CFP2 followed by a CFP4 for single-mode fiber applications over metro distances," he says.

Even though there are a variety of technologies appearing in the CFP form factor, this common physical module has helped control system development cost. "I could hear some rumblings about alternative form factors – which might lead to fragmentation of the market," he says.

Berthold is encouraged by the broad base of development efforts underway, particularly for 100Gbps transceivers, but also lower-cost 10Gbps and 40Gbps client-side modules. He notes the progress in reducing the cost of 100 Gigabit client interfaces over the next year. "Their high cost has held back adoption of 100 Gig," says Berthold. "We have had very cost effective 10 Gig multiplexing technology to fall back on, but it looks like native 100G interfaces are poised for growth."

Jörg-Peter Elbers, ADVA Optical Networking

Jörg-Peter Elbers, vice president, advanced technology at ADVA Optical Networking, was struck by the wide range of hot topics discussed at the show.

These include software-defined optics based on programmable transceivers that use advanced DSP technology and flexgrid ROADMs as the basis of a new coherent express layer. He also notes that control plane technologies are becoming an essential asset in managing network complexity when unleashing untapped network capacity.

"Traffic and content keeps growing at exponential scale - the fundamental demand-drivers are intact"

"Traffic and content keeps growing at exponential scale - the fundamental demand-drivers are intact"

Jörg-Peter Elbers, ADVA Optical Networking

Meanwhile, the rapid increase in end-user traffic, specifically mobile, is driving PON. As a result WDM is moving closer to the network edge, entering aggregation and access networks. He believes dense WDM-PON is gaining traction for mobile backhaul as fibre becomes the bottleneck when moving from Long Term Evolution (LTE) to the LTE-Advanced cellular technology.

Other trends to note, he says, are software-defined networking (SDN) and OpenFlow. "Originating from the campus and data centre world, network programmability is increasingly seen as key for tighter integration, more automation, and virtualisation of IT and computing services," says Elbers.

The industry increasingly sees the metro market as important to ramp up 100Gbps volumes, with different modulation solutions being promoted by vendors. These include performance reduced 100Gbps DP-QPSK (dual polarisation, quadrature phase-shift keying), 200Gbps DP-16QAM (dual polarisation, 16-quadrature amplitude modulation) and 4x28G direct-detection.

While some people expressed concerns about a fragmentation of the 100 Gig market, power consumption, footprint and cost are of primary importance in the metro, he says. "One analyst at the Ovum 100Gbps metro workshop at OFC said: 'Maybe, for a hammer everything looks like a nail…'," says Elbers. "With 4x28G optical duobinary being able to make use of 10Gbps T-XFP/SFP+, IEEE 802.3ba and CFP technologies, we believe there is a justification to differentiate."

ADVA demonstrated its 4x28Gbps optical duobinary direct-detection product at the show.

Elbers noted an interest in multi-core and few-mode fibres. "The next x10 in bandwidth is difficult to reach as additional gains from amplification, modulation, FEC and denser carrier spacing will be limited." he says. "The research community therefore is looking into new fibre types to add the spatial and modal dimensions alongside the current optimisation strategy." An area interesting to watch, but fundamental technical and economic challenges remain, he says.

He too is optimistic about the industry's prospects: "Traffic and content keeps growing at exponential scale - the fundamental demand drivers are intact." As a result, optical innovation will play an even bigger role in the future to keep pace with the bandwidth growth, he says.

Karen Liu, Ovum

"We're clearly in a technology-pull phase rather than technology-push phase with multiple system vendors doing 400Gbps-capable stuff instead of component guys showing demonstrations years in advance of system activity," says Karen Liu, principal analyst, components telecoms at Ovum.

"Optical burst mode switching may be crossing over from rather 'pie-in-the-sky' to practical"

"Optical burst mode switching may be crossing over from rather 'pie-in-the-sky' to practical"

Karen Liu, Ovum

It is not that that the components vendors aren't making innovative products, she says, just that they are not making announcements until there is real demand. "Corning, for example, showed a fiber that has already been shipping into Lightpeak," says Liu.

What surprised Liu at the show was Huawei's optical burst transport network prototype. "Optical burst mode switching may be crossing over from rather 'pie-in-the-sky' to practical," says Liu.

She notes how there isn't as much optics-versus-electronics positioning anymore but more a case of optics working with electronics. "Huawei's OBTN is an example," says Liu. "Instead of using optical burst mode to make an all-optical network, optics is part of a hybrid design."

Liu says there are now multiple relationships between silicon and optics including the two working together instead of in competition. "In networking, the term translucent networks seems to have gained popularity."

ZTE takes PON optical line terminal lead

ZTE shipped 1.8 million passive optical network (PON) optical line terminals (OLTs) in 2011 to become the leading supplier with 41 percent of the global market, according to Ovum.

"ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing"

"ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing"

Song Shi Jie, ZTE

The market research firm also ranks the Chinese equipment maker as the second largest supplier of PON optical network terminals (ONT), with 28 per cent global market share in 2011.

China now accounts for over half the total fibre-to-the-x (FTTx) deployments worldwide. ZTE says 1.05 million of its OLTs were deploy in China, with 70 percent for the EPON standard and the rest GPON. Overall EPON accounts for 85% of deployments in China. However GPON deployments are growing and ZTE expects the technology to gain market share in China.

There are some 300 million broadband users in China, made up of DSL, fibre-to-the-building (FTTB) and -curb (FTTC), says Song Shi Jie, director of fixed network product line at ZTE.

Of the three main operators, China Telecom is the largest. It is deploying FTTB and is moving to fibre-to-the-home (FTTH) deployments using GPON. China Unicom has a similar strategy. China Mobile is focussed on FTTB and LAN technology; because it is a mobile operator and has no copper line assets it uses LAN cabling for networking within the building.

The split ratio - the number of PON ONTs connected to each OLT - varies depending on the deployment. "In the fibre-to-the-building scenario, the typical ratio is 1:8 or 1:16; for fibre-to-the-home the typical ratio is 1:64," says Song.

ZTE has also deployed 200,000 10 Gigabit EPON (10GEPON) lines in China but none elsewhere, either 10GEPON or XGPON1 (10 Gigabit GPON). "ZTE is co-operating with some Tier 1 operators in Europe and the US for 10GEPON and XGPON1 testing," says Song.

Song attributes ZTE's success to such factors as reduced power consumption of its PON systems and its strong R&D in access.

The vendor says its PON platforms consume a quarter less power than the industry average. Its systems use such techniques as shutting down those OLT ports that are not connected to ONTs. It also employs port idle and sleep modes to save power when there is no traffic. Meanwhile, ZTE has 3,000 engineers engaged in fixed access product R&D.

As for the next-generation NGPON2 being development by industry body FSAN, Song says there are a variety of technologies being proposed but that the picture is still unclear.

ZTE is focussing on three main next-generation PON technologies: wavelength division multiplexing PON (WDM-PON), hybrid time division multiplexing (TDM)/ WDM-PON (or TWDM-PON) and orthogonal frequency division multiplexing (OFDM) PON. "We think OFDM PON can provide high security, high bandwidth and easy network maintenance," says Song.

ZTE says that the NGPON2 standard will be mature in 2015 but that commercial deployments will only start in 2018.

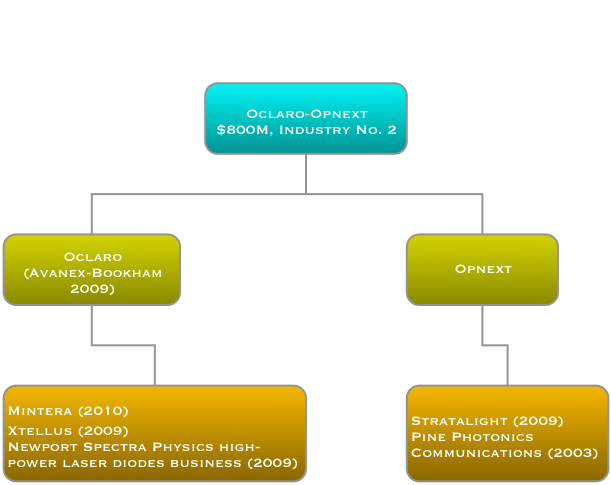

Oclaro-Opnext merger will create second largest optical component company

Oclaro has announced its plan to merge with Opnext. The deal, valued at US $177M, will result in Opnext's shareholders owning 42% of the combined company. The merger of the fifth and sixth largest optical component players, according to Ovum, will create a company with annual revenues of $800M, second only to Finisar. The deal is expected to be completed in the next 3-6 months.

Source: Gazettabyte

Source: Gazettabyte

Other details of the merger include:

- Combining the two companies will save between $35M-45M but will take 18 months to achieve.

- Restructuring and system integration will cost $20M-$30M.

- All five of the new company's fabs will be kept. The fabs are viewed as key assets.

- The new company will continue its use of contract manufacturers in Asia. Oclaro announced a recent deal with Venture, and that included the possibility of an Oclaro-Opnext merger.

- Oclaro's CEO, Alain Couder, will become the CEO of the new company. Harry Bosco, Opnext's CEO, will join the company's board of directors, made up of six Oclaro and four Opnext members.

- In 4Q 2011, Oclaro reported three customers, each accounting for greater than 10% sales: Fujitsu, Infinera and Ciena. Opnext reported 43% of its sales to Cisco Systems and Hitachi in the same period.

Industry scale

The motivation for the merger is to achieve industry scale, says Oclaro. "We have never been shy [of mergers and acquisitions] - we did Avanex and Bookham," says Yves LeMaitre, chief marketing officer for Oclaro. "We believe industry scale allows you to absorb certain fixed costs like fab infrastructure and the sales force." Scale also increases the absolute amount that can be invested in R&D, estimated at 12-13% of its revenues.

"It [the acquisition] is really about building a company that directly competes with Finisar," says Daryl Inniss, practice leader, components at Ovum. "It creates a stronger, vertically integrated company that starts at chips and goes all the way to the line card."

"We will be one of the most vertically integrated suppliers for 100 Gigabit coherent technology"

Mike Chan, Opnext

LightCounting believes the Oclaro-Opnext merger will be a success. Moreover, the market research firm expects further optical component M&As. Since the Oclaro-Opnext was announced, Sumitomo Electric Device Innovations has announced it will acquire Emcore's VCSEL and associated transceiver technology for $17M.

Meanwhile, Morgan Stanley Research is less positive about the merger, believing that the Opnext acquisition carries 'material risk'. It argues that the stated synergies are aggressive and that the integration of the two firms could distract Oclaro and lower its share price.

Products and technology

The deal expands Oclaro's transceiver portfolio, enhancing its offerings in telecom and strengthening its presence in datacom. It also expands the customer base: Opnext supplies Juniper, Google and H-P, new customers for Oclaro.

Common products shared by the two firms are limited, for high-end products the overlap is mainly 100 Gigabit coherent and tunable laser XFPs. LightCounting also points out that the two share some legacy SONET/SDH, WDM and Ethernet products: "Nothing that reduces competition significantly," it says in a research note.

"[With the Avanex-Bookham merger] There was a little bit of overlap in a few areas which we managed," says Oclaro's LeMaitre. "It is even easier in this case."

"We see potential, further down the road, for new very-short-reach optical interfaces"

Yves LeMaitre, Oclaro

Opnext acquired optical transmission subsystem vendor StrataLight in 2009 while Oclaro acquired Mintera in 2010. Both Oclaro and Opnext have used the expertise of the two subsystem vendors to become early market entrants of 100 Gigabit 168-pin multi-source modules.

But Oclaro makes the optical components for the modules - tunable lasers, lithium niobate modulators and integrated coherent transceivers - items that Opnext has to buy for its 100 Gig coherent module, says Ovum's Inniss: "Opnext has built decent gross margins when you consider that a lot of the optics they don't own themselves.” Oclaro's components will be used within Opnext's modules.

"We will be one of the most vertically integrated suppliers for key 100 Gigabit coherent technology moving forward," says Mike Chan, executive vice president of business development and marketing at Opnext.

Opnext stresses that it has its own programmes for integrated photonics. "We have been telling our customers that we have been working on some of these integrated photonics [for 100G coherent]," says Chan. "The StrataLight portion of Opnext also has a lot of work done, and IP created, in the coherent modem area."

Currently both companies' 100 Gigabit modules use NEL's coherent receiver DSP-ASIC. Oclaro has also made an investment in coherent chip start-up, ClariPhy. But for future coherent adaptive-rate designs, the joint company will be able to develop its own coherent chip. "We have the in-house know-how for the coherent modem chip," says Chan.

The merged company is well positioned to address client-side 100 Gigabit-ber-second (Gbps) transceivers. "Here the challenge is to achieve high density and low power [interfaces]," says Chan. Oclaro has VCSEL technology that can be used for very short reach 4x28Gbps arrays. Oclaro says it is the world's leading supplier of VCSELs for a variety of commercial applications and has now shipped over 150M units.

At OFC/NFOEC Opnext demonstrated a 1310nm LISEL (Lens-integrated Surface-Emitting distributed feedback Laser) array operating at 25-40Gbps. The surface-emitting distributed feedback (DFB) laser can also be used for the same 4x28Gbps design, says Chan. "Within the data centre 500m is the sweet-spot," says Chan. "It is not just the physical distance but the link-budget as the signal may have to go through a patch panel." The DFB can be used with multi-mode and single-mode fibre and Opnext believes it can achieve a 1km reach.

Oclaro does not rule out using its VCSEL technology to address such applications as optical engines, connecting racks and for backplanes. "We see potential, further down the road, for new very-short-reach optical interfaces into consumer, backplane, and board-to-board to really expand our addressable market," says LeMaitre

Further mergers

LightCounting argues that the 2011 floods in Thailand have added urgency to industry consolidation, with the Oclaro and Opnext merger being the first of several. Oclaro and Opnext were among the most impacted by the flood with Q4 2011 revenues being down 18% and 38%, respectively, says LightCounting.

Ovum also expects further mergers as companies strengthen their coherent and ROADM technologies.

Inniss believes ROADMs is the next area that Oclaro is likely to strengthen. Oclaro has acquired Xtellus but Ovum says the main ROADM leaders are Finisar, JDS Uniphase and CoAdna. Companies to watch include JDS Uniphase, Fujitsu Optical Components, CoAdna and Sumitomo, says Inniss.

A day after Ovum's and LightCounting's M&A comments, Sumitomo announced the acquisition of Emcore's VCSEL business unit.

ROADMs: core role, modest return for component players

Next-generation reconfigurable optical add/ drop multiplexers (ROADMs) will perform an important role in simplifying network operation but optical component vendors making the core component - the wavelength-selective switch (WSS) - on which such ROADMs will be based should expect a limited return for their efforts.

"[Component suppliers] are going to be under extreme constraints on pricing and cost"

"[Component suppliers] are going to be under extreme constraints on pricing and cost"

Sterling Perrin, Heavy Reading

That is one finding from an upcoming report by market research firm, Heavy Reading, entitled: "The Next-Gen ROADM Opportunity: Forecast & Analysis".

"We do see a growth opportunity [for optical component vendors]," says Sterling Perrin, senior analyst and author of the report. “But in terms of massive pools of money becoming available, it's not going to happen; it is a modest growth in spend that will go to next-generation ROADMs."

That is because operators’ capex spending on optical will grow only in single digits annually while system vendors that supply the next-generation ROADMs will compete fiercely, including using discounting, to win this business. "All of this comes crashing down on the component suppliers, such that they are going to be under extreme constraints on pricing and cost," says Perrin. The report will quantify the market opportunity but Heavy Reading will not discuss numbers until the report is published.

Next-generation ROADMs incorporate such features as colourless (wavelength-independence on an input port), directionless (wavelength routing to any port), contentionless (more than one same-wavelength light path accommodated at a port) and flexible spectrum (variable channel width for signal rates above 100 Gigabit-per-second (Gbps)).

Networks using such ROADMs promise to reduce service providers' operational costs. And coupled with the wide deployment of coherent optical transmission technology, next-generation ROADMs are set to finally deliver agile optical networks.

Other of the report’s findings include the fact that operators have been deploying colourless and directionless ROADMs since 2010, even though implementing such features using current 1x9 WSSs are cumbersome and expensive. However, operators wanting these features in their networks have built such systems with existing components. "Probably about 10% of the market was using colourless and directionless functions in 2010," says Perrin.

Service providers are requiring ROADMs to support flexible spectrum even though networks will likely adopt light paths faster than 100Gbps (400Gbps and beyond) in several years' time.

The need to implement a flexible spectrum scheme will force optical component vendors with microelectromechanical system (MEMS) technology to adopt liquid crystal technology – and liquid-crystal-on-silicon (LCoS) in particular - for their WSSs (see Comments). "MEMS WSS technology is great for all the stuff we do today - colourless, directionless and contentionless - but when you move to flexible spectrum it is not capable of doing that function," says Perrin. "The technology they (vendors with MEMS technology) have set their sights on - and which there is pretty much agreement as the right technology for flexible spectrum - is the liquid crystal on silicon." A shift from MEMS to LCoS for next-generation ROADM technology is thus to be expected, he says.

Perrin also highlights how coherent detection technology, now being installed for 100 Gbps optical transmission, can also implement a colourless ROADM by making use of the tunable nature of the coherent receiver. "It knocks out a bunch of WSSs added to the add/ drop," says Perrin. "It is giving a colourless function for free, which is a huge advantage."

Perrin views next-gen ROADMs as a money-saving exercise for the operators, not a money-making one. "This is hitting on the capex as well as the opex piece which is absolutely critical," he says. "You see the charts of the hockey stick of bandwidth growth and flat venue growth; that is what ROADMS hit at."

The Heavy Reading report will be published later this month.

Further reading:

New editorial calendar for 2012

Please click here for details.

Luxtera's 100 Gigabit silicon photonics chip

Luxtera has detailed a 4x28 Gigabit optical transceiver chip. The silicon photonics company is aiming the device at embedded applications such as system backplanes and high-performance computing (HPC). The chip is also being used by Molex for 100 Gigabit active optical cables. Molex bought Luxtera's active optical cable business in January 2011.

“Do I want to invest in a copper backplane for a single generation or do I switch over now to optics and have a future-proof three-generation chassis?”

Marek Tlalka, Luxtera

What has been done

To make the optical transceiver, a distributed-feedback (DFB) laser operating at 1490nm is coupled to the silicon photonics CMOS-based chip. One laser only is required to serve the four individually modulated 28Gbps transmit channels, giving the chip a 112Gbps maximum data rate. There are also four receive channels, each using a germanium-based photo-detector that is grown on-chip.

The DFB is the same laser that Luxtera uses for its 4x10Gbps and 4x14Gbps designs. What has been changed is the Mach-Zehnder waveguide-based modulators that must now operate at 28Gbps, and the electronics amplifiers at the receivers. “The chip [at 5mmx6mm] is pretty much the same size as our 4x10 and 4x14 Gig designs,” says Marek Tlalka, director of marketing at Luxtera.

Source: Luxtera

Source: Luxtera

Luxtera is announcing the 100 Gigabit chip which it is sampling to customers. Molex, for example, will package the chip and the laser to make its active optical cable products. Luxtera will package the transceiver chip and laser in a housing as an OptoPHY, a packaged product it already provides at lower speeds. The company will sell the 100Gbps OptoPHY for embedded applications such as system backplanes and HPC.

Applications

The 100GbE transceiver chip is targeted at next-generation backplane applications as well as active optical cables. And it is enterprise vendors that make switches, routers and blade servers that are considering adopting optical backplanes for their next-generation platforms, says Luxtera.

According to Tlalka, system vendors are moving their backplanes from 15Gbps to 28Gbps: “It is pretty obvious that building an electrical backplane at this data rate will be extremely challenging.”

When vendors design a new chassis, they want it to support three generations of line cards. Even if a system vendor develops a 28Gbps copper-based backplane, it will need to go optical when the backplane data rate increases to 40-50Gbps in 2-3 years’ time and 100Gbps when that speed transition occurs. “Do I want to invest in a copper backplane for a single generation or do I switch over now to optics and have a future-proof three-generation chassis?” says Tlalka.

Exascale computers, 1000x more powerful than existing supercomputers planned for the second half of the decade, is another application area. Here there is a need for 25-28Gbps links between chips, says Tlalka.

System platforms and HPC are ideal candidates for the packaged transceiver chip but longer term Luxtera is eyeing the move of optics inside chips such as ASICs. Such system-on-chip optical integration could include Ethernet switch ICs (See example switch ICs from Broadcom and Intel (Fulcrum)) and network interface cards. Another example highlighted by Tlalka is CPU-memory interfaces.

However such applications are at least five years away and there are significant hurdles to be overcome. These include resolving the business model of such designs as well as the technical challenges of coupling the ASIC to the optics and the associated mechanical design.

Standards

Luxtera's 100Gbps transceiver chip supports a variety of standards.

Operating at 25Gbps per channel, the chip supports 100GbE and Enhanced Data Rate (EDR) Infiniband. The ability to go to 28Gbps per channel means that the transceiver can also support the OTN (optical transport network) standard as well as proprietary backplane protocols that add overhead to the basic 25Gbps data rate.

In addition the chip supports the OIF's short reach and very short reach interfaces that define the interface between an ASIC and the optical module.

The chip is also suited for some of the IEEE Next Generation 100Gbps Optical Ethernet Study Group standards now in development. These interfaces will cover a reach of 30m to 2km.

400GbE and HDR Infiniband

Luxtera says that it is working on different channel ’flavours' of 100G. It is also following developments such as Infiniband Hexadecimal Data Rate (HDR) and 400GbE.

HDR will use 40Gbps channels while there is still an industry debate as to whether 400GbE will be implemented using ten channels, each at 40Gbps, or as a 16x25Gbps design.

BroadLight awarded a dynamic bandwidth allocation patent

Passive optical networking (PON) chip company, Broadlight, has been awarded a patent by the US Patent Office entitled: ‘Method and grant scheduler for cyclically allocating time slots to optical network units’.

Why is this important?

Dynamic bandwidth allocation (DBA) performs a key role in point-to-multipoint PON networks. A PON comprises an optical line terminal (OLT) at an operator’s central office connected to several optical network units (ONUs) via fibre. An ONU typically resides in the building basement or in a home.

The OLT broadcasts data downstream to the ONUs. In a gigabit PON (GPON), the downstream data rate is 2.5Gbps. Each ONU identifying the data meant for it using a unique packet header. In the upstream path – for GPON it is 1.25Gbps - only one ONU broadcasts at a time.

DBA is needed to make efficient use of the uplink capacity by assigning slots when each ONU can transmit its data. DBA must also take into account quality of service (QoS) requirements associated with the various traffic types (video, voice and data). “DBA increases revenue for the network provider by ensuring that bandwidth is not wasted,” says Eli Elmoalem, a system architect at Broadlight.

Method used:

Broadlight’s patent implements two approaches to DBA. The first, dubbed status reporting DBA, involves periodically polling the ONUs to determine their latest traffic needs. The second approach - traffic monitoring DBA – requires the OLT to run an algorithm that predicts the ONUs’ bandwidth needs based on their traffic bandwidth usage history.

Broadlight’s patented technique for GPON runs either or both approaches to determine how much bandwidth to allocate to each ONU. The patent also details how best to partition the tasks between the OLT silicon and software executed on the chip.

This is Broadlight’s second DBA patent award. The first, entitled “Method of providing QoS and bandwidth allocation in a point to multi-point network” is a generic DBA approach, says Eli Weitz, Broadlight’s CTO, applicable to any point-to-multipoint network whether it is cable, Broadband PON (BPON), GPON or Ethernet PON (EPON).

What next?

Developing DBA for 10G GPON. The development work for 10G PON is being undertaken by Full Service Access Network (FSAN) and will be standardised by the ITU-T.

DBA for 10G GPON will be more demanding: the split ratio - the number of ONUs served by one OLT – is higher with as many as 512 ONUs per PON, as is the upstream bandwidth. For 10G GPON, two upstream rates are being proposed: 2.5Gbps and 10Gbps.

References:

[1] “Predictive DBA: The ‘Right’ Method for Dynamic Bandwidth Allocation in Point-to-MultiPoint FTTH Networks”, a white paper by Broadlight

[2] “The Importance of Dynamic Bandwidth Allocation in GPON Networks,” a white paper by PMC-Sierra.

[3] “A Comparison of Dynamic Bandwidth Allocation for EPON, GPON and Next Generation TDM PON.” IEEE Communications Magazine, March 2009