Optical industry restructuring: The analysts' view

The view that the optical industry is due a shake-up has been aired periodically over the last decade. Yet the industry's structure has remained intact. Now, with the depressed state of the telecom industry, the spectre of impending restructuring is again being raised.

In Part 2, Gazettabyte asked several market research analysts - Heavy Reading's Sterling Perrin, Ovum's Daryl Inniss and Dell'Oro's Jimmy Yu - for their views.

Part II: The analysts' view

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen"

Sterling Perrin, Heavy Reading

Larry Schwerin, CEO of ROADM subsystem player Capella Intelligent Subsystems, believes optical industry restructuring is inevitable. Optical networking analysts largely agree with Schwerin's analysis. Where they differ is that the analysts say change is already evident and that restructuring will be gradual.

"The industry has not been in good shape for many years," says Sterling Perrin, senior analyst at Heavy Reading. "The operators are the ones with the power [in the supply chain] and they seem to be doing decently but it is not a good situation for the systems players and especially for the component vendors."

Daryl Inniss, practice leader for components at Ovum, highlights the changes taking place at the optical component layer. "There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader," says Inniss.

A typical rule of thumb for an industry in that you need the top three [firms] to own between two thirds and 80 percent of the market, says Inniss: "These are real market leaders that drive the industry; everyone else is a specialist with a niche focus."

But the absence of such dominant players should not be equated with a lack of change or that component companies don't recognise the need to adapt.

"Finisar looks more like an industry leader than we have had before, and its behaviour is that of market leader," says Inniss. Finisar is building an integrated company to become a one-stop-shop supplier, he says, as is the newly merged Oclaro-Opnext which is taking similar steps to be a vertically integrated company. Finisar acquired Israeli optical amplifier specialist RED-C Optical Networks in July 2012.

Capella's Schwerin also wonders about the long term prospects of some of the smaller system vendors. Chinese vendors Huawei and ZTE now account for 30 percent of the market, while Alcatel-Lucent is the only other major vendor with double-digit share.

The rest of the market is split among numerous optical vendors. "If you think about that, if you have 5 percent or less [optical networking] market share, that really is not a sustainable business given the [companies'] overhead expenses," says Schwerin.

However Jimmy Yu, vice president of optical transport research at Dell’Oro Group, believes there is a role for generalist and specialist systems suppliers, and that market share is not the only indicator of a company's economic health. “You have a few vendors that are healthy and have a good share of the market,” he says. “That said, when I look at some of these [smaller] vendors, I say they are better off.”

Yu cites the likes of ADVA Optical Networking and Transmode, both small players with less than 3 percent market share but they are some of the most profitable system companies with gross margins typically above 40 percent. “Do I think they are going to be around? Yes. They are both healthy and investing as needed.”

Innovation

Equipment makers are also acquiring specialist component players. Cisco Systems acquired coherent receiver specialist CoreOptics in 2010 and more recently silicon photonics player, Lightwire. Meanwhile Huawei acquired photonic integration specialist, CIP Technologies in January 2012. "This is to acquire strategic technologies, not for revenues but to differentiate and reduce the cost of their products," says Perrin.

"There is a problem with the rate of innovation coming from the component vendors," adds Inniss. This is not a failing of the component vendors as innovation has to come from the system vendors: a device will only be embraced by equipment vendors if it is needed and available in time.

Inniss also highlights the changing nature of the market where optical networking and the carriers are just one part. This includes enterprises, cloud computing and the growing importance of content service providers such as Google, Facebook and Amazon who buy components and gear. "It is a much bigger picture than just looking at optical networking," says Inniss.

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

"There is no one dominate [optical component] supplier driving the industry that you would say: This is undeniably the industry leader"

Daryl Inniss, Ovum

Huawei is one system vendor targeting these broader markets, from components to switches, from consumer to the data centre core. Huawei has transformed itself from a follower to a leader in certain areas, while fellow Chinese vendor ZTE is also getting stronger and gaining market share.

Moreover, a consequence of these leading system vendors is that it will fuel the emergence of Chinese optical component players. At present the Chinese optical component players are followers but Inniss expects this to change over the next 3-5 years, as it has at the system level.

Perrin also notes Huawei's huge emphasis on the enterprise and IT markets but highlights several challenges.

The content service providers may be a market but it is not as big an opportunity as traditional telecom. "It is also tricky for the systems providers to navigate as you really can't build all your product line to fit Google's specs and still expect to sell to a BT or an AT&T," says Perrin. That said, systems companies have to go after every opportunity they can because telecom has slowed globally so significantly, he says.

Inniss expects the big optical component players to start to distance themselves, although this does not mean their figures will improve significantly.

"This market is what it is - they [component players] will continue to have 35 percent gross margins and that is the ceiling," says Inniss. But if players want to improve their margins, they will have to invest and grow their presence in markets outside of telecom.

"I like the idea of a Cisco or a Huawei acquiring technology to use internally as a way to differentiate and innovate, and we are going to see more of that," says Perrin.

Thus the supply chain is changing, say the analysts, albeit in a gradual way; not the radical change that Capella's Schwerin suggests is coming.

"It is just a very slow, grinding process of adjustment; I am not sure that the next five years will be any different to what we've seen," says Perrin. "I just don't see why there is some catalyst that suggests it is going to be different to the past two years."

This is based on an article that appears in the Optical Connections magazine for ECOC 2012

60-second interview with .... Dell'Oro's Jimmy Yu

"For the year, it is going to be a fivefold growth rate [for 100 Gig transport]."

Jimmy Yu, Dell'Oro

Q: That fact that the market is down 5 percent on a year ago. Why is this?

A: There are a few factors. First, the macro-economy in Europe continues to get worse; that causes a slowdown.

A second factor is that in North America there was a decline in the second quarter, which is pretty unusual. Part of it, we think, might be that operators have caught up with a lot of the spending to increase broadband, after adding [to the network] for a couple of good years.

The third issue is that the China market has had a really slow start. And while there has been talk about the Chinese market softening, it seems that the CapEx [capital expenditure] is there for a strong second half.

What categories does Dell'Oro include when it talks about optical transport?

There are two main pieces: WDM [wavelength division multiplexing], both metro and long haul, and the multi-service multiplexer used for aggregation. The third piece, which is really small, is optical switching - optical cross-connect used in the core and lately more so in the metro.

According to Dell'Oro, wavelength division multiplexing was up 5 percent in the first half of 2012 compared to the same period a year ago, due to demand for 40 Gig and 100 Gig. What is happening in these two markets?

At 100 Gig we are at an inflection point where demand growth rates are really high. We've got a doubling in demand and shipments quarter-on-quarter [in the second quarter]. For the year, it is going to be a fivefold growth rate.

Also the 40 Gig is still growing. It has been around for a few years so its growth rate is not as strong [as 100 Gig transport] but it is still a significant part of the market.

Has the market settled on particular modulation scheme, especially at 40 Gig?

For 100 Gig the majority [deployed] is coherent. There is one company at least, ADVA Optical Networking, which is coming out with its direct-detection scheme for 100 Gig. This has now been shipping for one quarter. There is a market for the price point and the lower-span link of direct-detection.

For 40 Gig there is still a mix of modulations. Vendors coming out with 100 Gig coherent are also coming out with 40 Gig coherent options. So coherent at 40 Gig is now approaching half of the total market and is happening pretty quickly.

As for [40 Gig] DQPSK [differential quadrature phase-shift keying] modulation, it is probably a little bit more than DPSK [differential phase-shift keying].

You also report a rise in the adoption of optical packet products and that it contributed close to one-third of the optical market revenues in the first half 2012. Why is that?

The optical packet platform is a wider definition than just packet optical transport systems (P-OTS).

One reason why optical packet is growing is that with traditional P-OTS, you have cross-connect and switching capabilities in a WDM system so as you go to higher 40 and 100 Gig wavelengths you want some bandwidth management in that system.

Another thing is that people are trying to make the aggregation layer - the traditional SONET/SDH - more Ethernet friendly and MPLS-TP [multiprotocol label switching, transport profile] is gaining traction.

Combined, we are seeing this optical packet market has grown 12 percent year-on-year in the second quarter whereas the overall market has declined.

Dell'Oro said Huawei has 20 percent market share, which other vendors have double-digit market share?

Besides Huawei, the other vendors with double-digit percentage for the quarter - in order - are ZTE, Alcatel-Lucent and Ciena.

Did you see anything in this latest study that was surprising?

There was nothing in this quarter but I saw it last quarter. The legacy equipment – traditional SONET/SDH – is declining. Most of the market decline for optical is in legacy.

SONET/SDH sales in the second quarter of 2012 declined by 20 percent year-on-year. It is finally happening: the market is shifting away from SONET/SDH.

Has the restructuring of the optical industry already started?

The view that consolidation in the optical networking industry is needed is not new. For a decade, ever since the end of the optical boom in 2001, consolidation has been called for and has been expected. And while the many optical startups funded then have long exited or been acquired, the optical industry continues to support numerous optical networking and component generalist and specialists.

Given the state of the telecom market, is a more fundamental industry restructuring finally on its way?

"The business model of the communication sector needs to change, and change in a relatively short order"

Larry Schwerin, CEO of Capella Intelligent Subsystems

Larry Schwerin, CEO of Capella Intelligent Subsystems, believes change is inevitable. He argues that the industry supply chain will change, especially as firms become more vertically integrated.

"This is not to say that the market and demand are not there," says Schwerin, but the industry is stuck with a decade-old structure yet the market has changed.

Optical market dynamics

Schwerin starts his argument by highlighting certain fundamental drivers. IP traffic continues to grow at over 30% a year, while the nature of the traffic is changing, especially with cloud computing and as users generate more digital media content.

“The current rate of bandwidth growth coupled with the rate of CapEx spend, the gap is widening and the revenue-per-bit is dropping,” he says. “Some argue that bandwidth growth will slow down as operators charge [users] more, but to date this hasn't been seen.”

These trends are welcome for the optical companies, says Schwerin, as operators adopt lower layer, optical switching as a cheaper alternative to IP routing. “The number of [wavelength-selective] switches per node is growing quite dramatically," he says. "We are now seeing deployments with, on average, 6-8 switches per node and people are projecting as many as 20 as people start deploying colourless, directionless, contentionless-based switching."

But such demand is coupled with fierce competition among numerous players at each layer of the optical industry's supply chain.

"Some 80% of the optics used by system vendors are bought. How do you differentiate on features above and beyond what you are buying?"

Supply chain

The annual global operator market for wireless and wireline equipment is valued at US $250bn, says Schwerin, using market research and financial analyst firms' data.

The global optical networking equipment market is $15bn. The Chinese vendors Huawei and ZTE now account for 30% of the market, while Alcatel-Lucent is the only other major vendor with double-digit share. The rest of the market is split among numerous optical vendors. "If you think about that, if you have 5% or less [optical networking] market share, that really is not a sustainable business given the [companies'] overhead expenses," says Schwerin.

The global optical component market is valued at $5bn. It is likely larger, anything up to $8bn, argues Schwerin, because of the Chinese optical companies supplying Huawei and ZTE.

"You have a $5-8bn market selling products into $15bn, and then the $15bn is trying to repurpose that material and resell it to the carriers - is that really what is going on?" says Schwerin. To this vendor hierarchy is added contract manufacturers, with different players serving the component and the system vendors.

The slim profits operators are making on their services is forcing them to place significant pricing pressure on the system companies that already face fierce competition. Meanwhile, the optical component and contract manufacturers are also trying to make money in this environment.

Looking at gross margin data from Morgan Stanley, Schwerin says that the system vendors' figures range from 35% for the low end to 40% at the high end. "What the figures highlight is a lack of differentiation," he says. "And, in part, it is because they are buying all the same technology."

Schwerin says that some 80% of the optics used by system vendors are bought. "How do you differentiate on features above and beyond what you are buying?"

The optical components vendors' gross margins of a year ago were 30%. More recent data shows these figures are down, with the only segment showing a rise being optical sub-systems.

What next?

Schwerin says one way to improve the health of the industry is greater vertical integration. How this will be done - which players get consumed and how - will only become clear in the next 2-3 years but he is confident it will happen. "There are just too many layers of the ecosystem and it is just too fragmented," he says.

Operator mergers and slower spending put pressure on vendors at each layer of the supply chain, inducing revenue stalls. "These swings seems to be more and more violent," says Schwerin. "It is difficult for companies to maintain themselves in these cycles, let alone innovate."

Schwerin highlights Cisco System's acquisition of silicon photonics start-up, Lightwire, earlier this year, as an example of a system vendor embracing vertical integration while also acquiring innovation. Another example is Huawei's acquisition of optical integration specialist, CIP Technologies.

"The business model of the communication sector needs to change, and change in a relatively short order," says Schwerin, who believes it has already started. He cites the merger between the two large optical component vendors, Oclaro and Opnext, and expects a similar deal among the system vendors: "One of those 5 percenters will be absorbed."

As the market further consolidates, and as system companies drive fundamental technologies, the components' market will start to shrink. "It is then like a chain reaction; it forces itself," he says.

Schwerin's take is that rather than continue with the existing optical component and contract manufacturing model, what is more likely is that what will be supplied will be basic optical components. Differentiation will be driven by the system vendors.

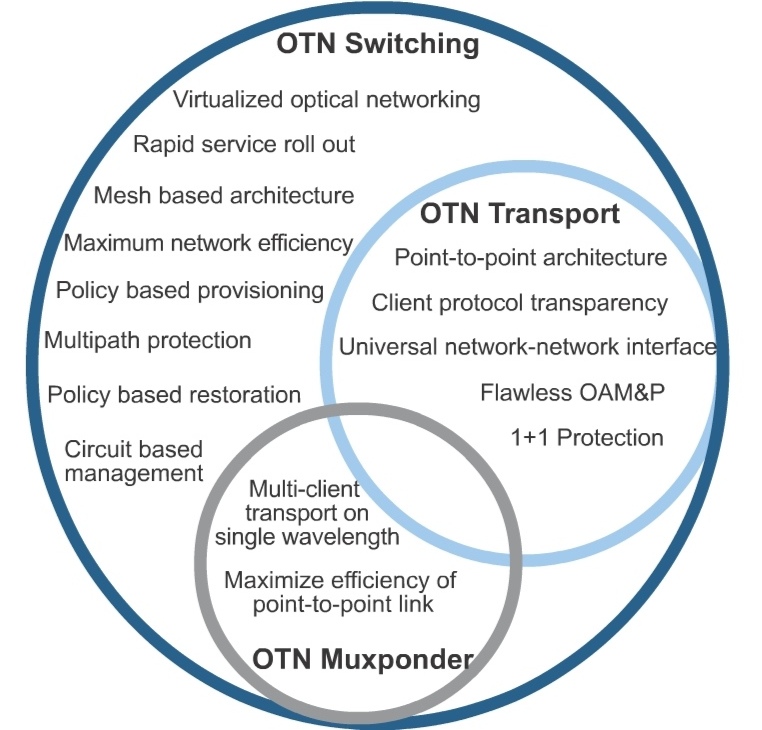

The OTN transport and switching market

Source: Infonetics Research

Source: Infonetics Research

The OTN transport and switching market is forecast to grow at a 17% compound annual growth rate (CAGR) from 2011 to 2016, outpacing the 5.5% CAGR of the optical equipment market (WDM, SONET/SDH). So claims a recent study on the OTN equipment marketplace by Infonetics Research.

A Q&A with report author, Andrew Schmitt, principal analyst for optical at Infonetics.

How should OTN (Optical Transport Network) be viewed? As an intermediate technology bridging the legacy SONET/SDH and the packet world? Or is OTN performing another, more fundamental networking role?

There is a deep misconception that once the voyage to an all-packet nirvana is complete, there is no need for SONET/SDH or an equivalent technology. This isn’t true. Networks that are 100% packet still need an OSI layer 1 mechanism, and to date this is mostly SDH and increasingly OTN.

OTN should be viewed as the carrier transport protocol for the foreseeable future. For many carriers, OTN will be used not just for carrying a single packet client, but for interleaving multiple clients onto the same wavelength. This is OTN switching, and it is a superset of OTN transport functionality.

Most people talk about the OTN market but they fail to distinguish between whether OTN is used as a point-to-point technology or as a switching technology that allows the creation of an electronic mesh network.

What is OTN doing within operators' networks that accounts for their strong investment in the technology?

OTN is the new physical layer protocol carrying out the OSI [Open Systems Interconnection] layer 1 functions. Carriers are investing in OTN as part of their continuing investments in WDM [wavelength division multiplexing] equipment, most of which supports OTN transport, a maturing market. The new market is that of OTN switching, which resembles the SONET/SDH multiplexing scheme, but with much better features and management.

OTN switching deployments are directly related to large scale deployments of 40G and 100G transport networks as part of what I like to call The Optical Reboot. As these new wavelength speeds are rolled out, often on unused fibre, other technologies are being introduced at the same time – things like OTN switching and new control plane methods.

"People are underestimating how hard it is to build this [OTN] hardware and combine it with control plane software"

Please explain the difference between the main platforms - OTN transport, OTN switching and P-OTS. And will they have the same relative importance by 2016?

OTN switching is a superset of OTN transport, and the differences are shown in a Venn diagram (chart above) from a recent whitepaper I wrote, Integrated OTN Switching Virtualizes Optical Networks. Somewhere between the two is the muxponder application, which is good for low-volume deployments but becomes expensive and tough to manage when used in quantity.

P-OTS (packet-optical transport systems) are boxes that combine both layer 1 (SONET/SDH and/or OTN switching) with layer 2 (Ethernet, MPLS-TP, other circuit-oriented Ethernet (COE) protocols) in the same hardware and management platform.

Cisco was one of the early leaders in this space with some creative brute-force upgrades to the venerable 15454 platform. Since then, many legacy SONET/SDH multi-service provisioning platforms (MSPPs) have seen upgrades to carry Ethernet. Some of the best examples of this platform type are the Fujitsu 9500, Tellabs' 7100, and Alcatel-Lucent's 1850.

You say a big vendor battle is brewing in the P-OTS space: Cisco, Tellabs, and Alcatel-Lucent are the top 3 vendors, but Fujitsu, Ciena, and Huawei are gaining. What factors will determine a vendor's P-OTS success here?

It really depends. In the metro-regional applications of bigger boxes, things like 100G optics and OTN switching will be more important, as the layer 2 functions are handed off to dedicated layer 2/3 machines. As you get closer to the edge, though, OTN switching will have no importance and everything will depend on the layer 2 and layer zero features.

For layer 2, this means supporting a lightweight circuit-oriented Ethernet protocol with awareness of all the various service types that might be in play. For layer zero, it is all about cheap tunable optics (tunable XFP and SFP+), but particularly ROADMs. I think BTI Photonics, Cyan, Transmode, and ADVA Optical Networking are some of the smaller players to watch here. Mobile backhaul, data centre interconnect, and enterprise data services are the big engines of growth here.

Were there any surprises as part of your research for the report?

There just are not that many vendors shipping OTN switching systems today. I think people are underestimating how hard it is to build this hardware and combine it with control plane software. In 2011, only Ciena, Huawei, and ZTE shipped OTN switching for revenue. This year we should see Alcatel-Lucent, Infinera, Nokia Siemens, and maybe a few more.

Is there one OTN trend currently unclear that you'd highlight as worth watching?

Yes: It isn’t clear to what degree carriers want integrated WDM optics in OTN switches. In the past, big SONET/SDH switches like Ciena’s CoreDirector were always shipped with short-reach optics that connected it to standalone WDM systems. I think going forward, OTN switching and the WDM transport functions must be built into the same hardware in order to get the benefits of OTN switching at the best price, and that’s why I wrote the Integrated OTN Switching white paper – to try to communicate why this is important. It is a shift in the way carriers use this equipment, though, and as you know, some carrier habits are hard to break.

Further reading

OTN Processors from the core to the network edge, click here

Is optical components becoming a buyer's market?

"An organisation's gross margins ride on these new products"

Daryl Inniss, Ovum Components.

The global optical component market was down 2% in the second quarter of 2011 at US $1.55 billion, according to Ovum.

The good news is that the market research company is forecasting that modest growth will resume this quarter now that the build-up in component inventory that led to the market contraction has largely been worked through.

But Ovum is warning that there are signs that the continued weak market conditions and fierce competition could lead to sharp price declines even for newer, high-valued products. "An organisation's gross margins ride on these new products," says Daryl Inniss, practice leader, Ovum Components.

Oclaro's CEO on a recent earnings call said he was being asked for price concessions on 40Gbps products. Ovum also says the ROADM and tunable laser XFPs markets are becoming more crowded and competitive.

Inniss stresses that there is no evidence that companies are cutting prices to gain an edge but while he expects volumes will grow, intense pricing pressure should now be expected.

LightCounting points out that the slowdown in sales of optical component and modules in early 2011 has been limited to products that did very well in 2010 or which had long lead times, like wavelength-selective switches for ROADMs and 40Gbps modules. It says there is little, if any, excess inventory of components accumulated across the broader market.

"The telecom transceiver market remained steady in Q1 2011, but it declined further in Q2 mostly due to lower sales of 40Gig client-side modules," says Vladimir Kozlov, CEO of LightCounting. "We expect that by the end of this year, the telecom market segment will be strong again."

Best in a decade

The second quarter market dip follows a period where the optical components industry experienced its strongest yearly growth for a decade. The market reached US $6 billion for the year ending first quarter 2011 - a first since 2001.

So long as network expansion keeps up with traffic, we are looking at sustainable growth”

So long as network expansion keeps up with traffic, we are looking at sustainable growth”

Vladimir Kozlov, LightCounting

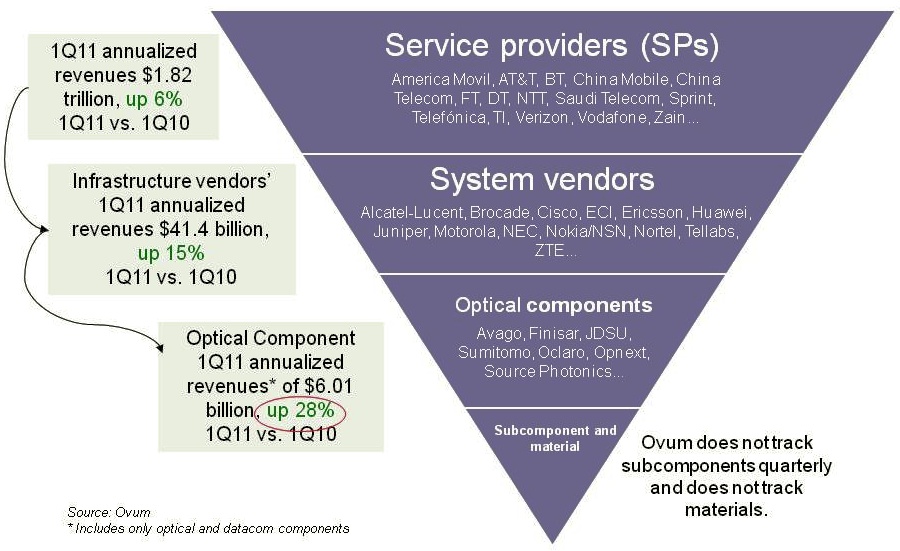

The six quarters of consecutive market growth up to the second quarter was due partly to the overall health of the telecom industry. The service provider industry - wireless and wireline - grew 6% year-on-year between 2Q10 and 1Q11, to reach $1.82 trillion. In turn, the equipment market, mainly telecom vendors but including the likes of Brocade, grew 15% to $41.4 billion.

Ovum attributes the 28% growth in optical components between 2Q10 and 1Q 2011 to strong growth in the fibre-to-the-x (FTTx) market as well as new revenues entering the market from datacom players. A third factor was optical equipment vendors over-ordering long lead-time items – such as ROADMs – to secure supply.

“ROADMS did grow nicely but if you look at wavelength-selective switches, it is not such a big market," says Kozlov. The market research firm says the wavelength-selective switch market was $280 million in 2010.

LightCounting says 10 Gigabit SFP+ optical transceivers was a market highlight in 2010, with volume shipments tripling. Ethernet SFP+ sales alone reached $180 million in 2010, and will grow to $250 million this year.

“The optical component market grew 36% in 2010, and in 2011 we’re projecting it will grow 7%,”says Inniss

But competition is intense. Finisar may be the market leader but only 4% market share separates the players in second through to sixth place, says Ovum. “It’s a very competitive market and there is no breakaway here,” says Inniss.

Another challenge is the emergence of the Chinese optical component players. The large-scale deployment of FTTx being undertaken by the main three Chinese operators means that there is a huge market opportunity for local optical component and module players. The Chinese market also accounts for half the all 40 Gigabit-per-second shipments, according to Infonetics Research.

“Looking at the western suppliers, everyone is reporting slowdowns and drops in the second quarter [of 2011],” says Kozlov. “Yet from the data we are getting from the Chinese optical component players, they grew 35% in 2010 and are on track for 30% growth this year.”

Another challenge is for firms to fund sufficient R&D. Share prices took a severe hit after the companies issued warnings about second-quarter sales. “The entire optical component market is depressed because of the localised correction,” says Inniss. “It will still grow but because it is so much smaller than 2010, capital markets are bashing the companies.”

Since the stock market is an important source of investment, it may take several years for the market to recover the share price levels at the start of 2011. “It won’t stop investment in technology but there is going to be real hard eyes on each decision that is made,” says Inniss.

The main challenge facing optical component players is not so much technical issues but more the requirement to continually decrease costs. This is not new but neither is it going away, says Inniss.

Positive outlook

Yet the analysts expect market growth to continue.

Inniss points to the growing role of optics for short-distance interfaces: “The I/O (input-output) bandwidth requirements are sufficiently high, whether it is the backplane or chip-to-chip connections, that the market realisation is that optics will play a role.”

Ovum also highlights consumer market developments such as the USB 3.0 interface which will drive the market for active optical cables. “It [the consumer market] is not going to happen tomorrow - meaning 2012 - but it is something that is coming and has the potential to transform the industry,” says Inniss.

“Companies such as Finisar and Avago [Technologies] are becoming more assertive in enforcing their intellectual rights,” says Kozlov. This is as a positive development that has been missing in the past: “Protecting your intellectual property ultimately helps you become profitable,” he says.

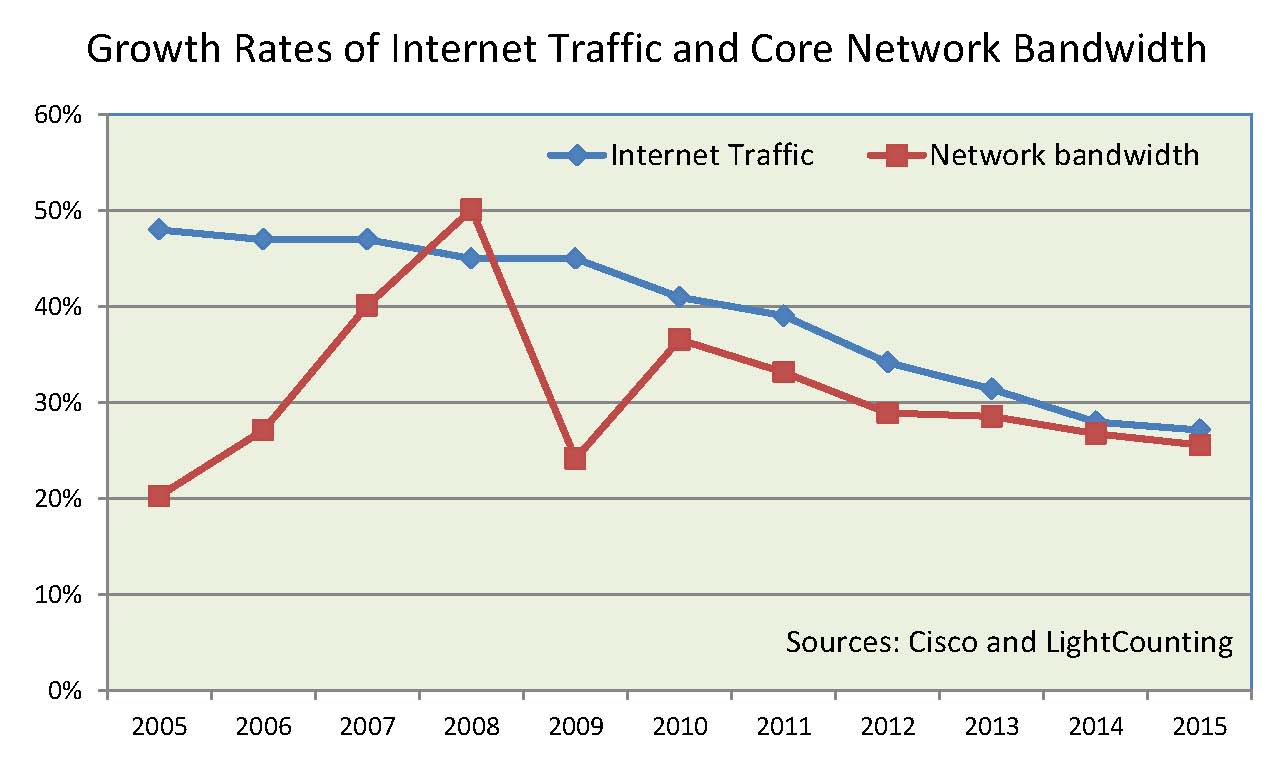

LightCounting also highlights the need for network investment to keep track with traffic growth. "So long as network expansion keeps up with traffic, we are looking at sustainable growth,” says Kozlov. See Plotting transceiver shipments versus traffic growth.

This article is based on a piece that appeared in the ECOC 2011 exhibition guide.

Plotting transceiver shipments versus traffic growth

Summing transceiver shipments in the core of the network and plotting the data against traffic growth provides useful insights into the state of the network.

"We use transceiver shipment data [from vendors] to calculate how fast the network is growing and compare it to the traffic growth," says Vladimir Kozlov, CEO of market research firm, LightCounting.

What it reveals is that in 2005-06 there was a significant discrepancy between traffic growth and installed capacity: there was 35-40% traffic growth while investment in dense wavelength division multiplex (DWDM) only grew 20-25%. This gap began to shrink in 2007-08.

LightCounting stresses that network investment must keep track with the traffic growth. "It is not going to be a one-to-one correlation as network efficiency improves over time," says Kozlov. But the gap in the past was too large and probably had to do with unused network capacity.

"As long as the network expansion is to continue just to keep up with traffic, we are looking at sustainable growth," says Kozlov.

Good long-term news for the optical component and module makers.

100 Gig: Is market expectation in need of a reality check?

“It could easily be ten to 15 years before we see 100Gbps in a big way on the public network side”

“It could easily be ten to 15 years before we see 100Gbps in a big way on the public network side”

Mark Lutkowitz, Telecom Pragmatics

Infonetics Research, in a published White Paper, says that 100Gbps technology will be adopted at a faster rate than 40Gbps was in its first years, and that the 100Gbps market will begin in earnest from 2013. Indeed this could even be sooner if China, which accounts for half of all 40Gbps ports being shipped, moves to 100Gbps faster than expected.

LightCounting, in its research, describes 100 Gbps optical transmission as a transformational networking technology for carriers, and forecasts that sales of 100Gbps dense wavelength division multiplexing (DWDM) line cards will grow to US $2.3 billion by 2015.

But one research firm, Telecom Pragmatics, is sounding a note of caution. It reports that the 40Gbps market is growing nicely and believes that it could be at least a decade before there is a substantial 100Gbps market.

“100G is not going to kill 40G and, if anything, we are bullish about 40G,” says Mark Lutkowitz, principal at Telecom Pragmatics. “I’m not talking about large volume ramp-up of 40G but there is arguably a ramp-up.”

100G Paradox

One reason, not often mentioned, why 40Gbps is being adopted is that it does not require as many networking changes as when 100Gbps technology is deployed. “There is additional compensation [needed] and it is not clear that all the fibres will work with 100G,” says Lutkowitz.

There is also what he calls the ‘100G Paradox’.

The 100Gbps technology will most likely be considered at pinch-points in the operators’ networks. Yet these are the same network pinch-points that were first upgraded to 10Gbps. As a result they are likely to have legacy DWDM systems such that upgrading to 100Gbps is a considerable undertaking. “It is questionable whether these systems can even work with 100G,” he says.

"We really think that 40G should be getting a lot more respect than it is getting”

”When you look at service providers they are willing to put up with a whole amount of pain before they buy something, and they will certainly not forklift electronics or fibre - they will only do that as a last resort.” Another attraction of 40Gbps for the operators is its growing maturity - it is a technology that has been available for several years.

Costs

Telecom Pragmatics also dismisses the argument made by component vendors that the market will move to 100Gbps especially if the cost-per-bit of 100G technology declines faster than expected.

“The first cost [point] is ten times 10G and really you need to get to something like six or seven times [the cost of] 10G before you consider 100G,” says Lutkowitz. But that is not the sole cost. Network protection is needed which means a second system and there are additional networking and operational costs associated with 100Gbps.

Moreover, to whatever extent 40G is deployed, it will put further pressure on 100Gbps as 40Gbps prices decline. “In the 10G market, prices continued to decline and that precluded 40G, now you have 40G - to whatever extent there is deployment - precluding 100G,” says Lutkowitz.

“It could easily be 10 to 15 years before we see 100G in a big way on the public network side,” says Lutkowitz. But he stresses that in the datacenter and for the enterprise, demand for 100Gbps technology will be a different story.

Meanwhile Telecom Pragmatics expects further operator trials at 100Gbps as well as new system announcements from vendors. “But we really think that 40G should be getting a lot more respect than it is getting,” says Lutkowitz.

Optical components: The six billion dollar industry

The service provider industry, including wireless and wireline players, is up 6% year-on-year (2Q10 to 1Q11) to reach US $1.82 trillion, according to Ovum. The equipment market, mainly telecom vendors but also the likes of Brocade, has also shown strong growth - up 15% - to reach revenues of over $41.4 billion. But the most striking growth has occurred in the optical components market, up 28%, to achieve revenues of over $6 billion, says the market research firm.

Source: Ovum

Source: Ovum

“This is the first time optical components has exceeded six billion since 2001,” says Daryl Inniss, practice leader, Ovum Components. Moreover, the optical component industry growth has continued over six consecutive quarters with the growth being more than 25% for the past four quarters. “None of the other [two] segments have performed in this way,” says Inniss.

Ovum cites three factors accounting for the growth. Fibre-to-the-x (FTTx) is experiencing strong growth while revenues have entered the market from datacom players from the start of 2010. “The [optical] component recovery was led by datacom,” says Inniss. “We speculate that some of that money came from the Googles, Facebooks and Yahoos!.” A third factor accounting for growth has been optical equipment vendors ordering more long lead-time items than needed – such as ROADMs – to secure supply.

Source: Ovum

Source: Ovum

The second chart above shows the different market segments normalised since the start of 1999. Shown are the capex spending for optical networking, optical networking equipment revenues, optical components and FTTx equipment spending.

Optical networking spending is some 3.5x that of the components. FTTx equipment revenues are lower than the optical component industry’s and is therefore multiplied by 2.25, while capex is 9.2x that of optical equipment. The peak revenue in 2001 is the optical component revenues during the optical boom.

Several points can be drawn from the normalised chart:

- The strong recent growth in FTTx is the result of the booming Chinese market.

- From 2003 to 2008, the overall market showed steady growth, as illustrated by the best-fit line.

- From 2003 to 2008, capex and optical networking revenues were in line, while two thirds of the optical component revenues were due to this telecom spending.

- From 2010 onwards, components deviated from these two other segments due to the datacom spending from new players and the strong growth in FTTx.

- Once the market crashed in early 2009, optical components, networking and capex all fell. FTTx recovered after only one quarter and was followed by optical components. Optical networking and capex, meanwhile, have still not fully recovered when compared with the underlying growth line.

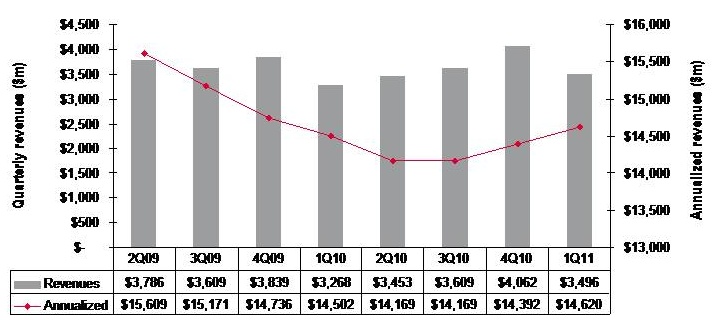

Optical networking market in rude health

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Quarterly market revenues, global optical networking (1Q 2011). Source: Ovum

Despite recent falls in optical equipment makers’ stock, the optical networking market remains in good health with analysts predicting 6-7% growth in 2011.

For Andrew Schmitt, directing analyst for optical at Infonetics Research, unfulfilled expectations are nothing new. Optical networking is a market of single-digit yearly growth yet in the last year certain market segments have grown above average: spending on ROADM-based wavelength division multiplexing (WDM) optical network equipment, for example, has grown 20% since the first quarter of 2010.

“Every few years people get this expectation that there is going to be this hockey stick [growth] and it is not,” says Schmitt. “There has been a lot of Wall Street money moving into this sector in the latter part of 2010 and first part of this year and they have just had their expectations reset, but operationally the industry is very healthy.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate”

Andrew Schmitt, Infonetics Research

But Schmitt acknowledges that there is industry concern about the market outlook. “There have been lots of client calls in the first half of the year wanting to talk numbers,” says Schmitt. “When the market is growing rapidly there is no need for such calls but when it is uncertain, customers put more time into understanding what is going on.”

Both Infonetics and market research firm Ovum say the optical networking market grew 7% globally in the last year (2Q10 to 1Q11).

Ovum says the market reached US $3.5bn in the first quarter of 2011 and it expects 6% growth this year. “Most of the growth will come from North America—general recovery, stimulus-related spending, and LTE (Long Term Evolution)-inspired spending; and from South and Central America mostly mobile and fixed broadband-related,” says Dana Cooperson, network infrastructure practice leader at Ovum.

Ovum also notes that optical networking annualised spending for the last four quarters (2Q10-1Q11) finally went into the black with 1% growth, to reach $14.6bn. Annualised share figures are a strong indicator of longer-term market trends, says Ovum.

Market growth

Factors accounting for the growth include optical equipment demand for mobile and broadband backhaul. Carriers are also embarking on a multi-year optical upgrade to 40 and 100 Gigabit transmission over Optical Transport Network (OTN) and ROADM-based networks. Infonetics notes that ROADM spending in particular set a new high in the first quarter, rising 4% sequentially.

Ovum expects overall growth to come from metro and backbone WDM markets and from LTE. “For metro it is a combination of new builds, as DWDM continues to take over the metro core from SONET/SDH, and expansions of ROADM and 40 Gigabit,” says Cooperson. “For backbone it is a combination of retrofits for 40 and 100 Gigabit and overbuilds with 40 and 100 Gigabit coherent-optimised systems.”

Many operators are also looking at OTN switching and how it can help with network efficiency and manageability, she says, while mobile backhaul continues to be a hot spot as well at the access end of the network.

The Americas are the regions accounting for market growth whereas in Asia-Pacific and Europe, Middle East and Africa the spending remains flat.

“We’re not as bullish on Europe as I’ve heard some others are,” says Cooperson. “We expected China to slow down as capital intensities in the 34-35% seen in 2008 and 2009 were unsustainable. We saw the cooling down a bit earlier in 2010 than we had expected, but it did cool down and will continue to.”

Ovum expects Asia-Pacific as a whole to be moribund. But at least the pullbacks in China will be countered by slow growth in Japan and a big upsurge in India after a huge decline last year due to delayed 3G-related builds among other issues.

Outlook

Ovum is optimistic about the optical networking market due to continued competitive pressures and traffic growth. “We don’t think traffic growth can just continue without attention to the underlying issues related to revenue pressure, regardless of competitive pressures,” says Cooperson. “But newer optical and packet systems offer significant improvements over the old in terms of power efficiency, manageability, and of course 40 and 100 Gigabit coherent and ROADM features.”

“Most of the growth will come from North America"

Dana Cooperson, Ovum.

Many networks worldwide are also due for a core infrastructure update to benefit capacity and efficiency while many other operators are upgrading their access networks for mobile backhaul and enterprise Ethernet services.

Schmitt stresses that while it is right to talk about a 'core reboot', there are all sorts of operators that make up the market: the established carriers, those focussed on Layer 2 and Layer 3 transport, dark fibre companies and cable companies.

“Everyone has a different business so there is not a whole lot of group-think in this industry,” says Schmitt. “So when you talk about a transition to 40 and 100 Gigabit, some carriers will make that transition earlier than others because the nature of their business demands it.”

However, there are developments in equipment costs that are leading to change. “Once you get out to 2013-14, 100 Gigabit [transport] looks really good relative to 40 Gigabit and tunable XFPs at 10 Gigabit look really, really good,” says Schmitt, who believes these are going to be two dominating technologies. “People are going to use 100 Gigabit and when they can afford to throw more 10 Gigabit at the [capacity] problem, in shorter metro and regional spans, they will use tunable XFPs,” he says. “That is a whole new level in terms of driving down cost at 10 Gigabit that people haven’t factored in yet.”

Pacier change

The move to 100 Gigabit will not lead to increased spending, stresses Schmitt. Rather its significance is as a ‘mix shift’: The adoption of 100 Gigabit will shift spending from older systems to newer ones so that the technology is interesting in terms of market share shift rather than by growing overall revenues.

That said, there are areas of optical spending where capital expenditure (capex) is growing faster than the single-digit trend. These include certain competitive telco providers and dark fibre providers like AboveNet, TimeWarner Telecom and Colt. “You look at their capex year-over-year and it is increasing in some cases more over 20% a year,” says Schmitt.

He also notes that while the likes of Google, Yahoo, Microsoft and Apple do not spend on optical equipment as much as established operators such as Verizon or AT&T, their growth rate is higher. “There are sectors of the market that are growing quickly, and competition that are positioned to service those sectors successfully are going to see above-trend growth,” says Schmitt.

He highlights three areas of innovations - ‘big vectors’- that are going to change the business.

One is optical transport's move away from simple on-off keying signalling that opens up all kinds of innovation. Another is the shift in the players buying optical equipment. “A lot more of the R&D is driven by the AboveNets, Time Warners, Comcasts and the Googles and less by the old time PTTs,” says Schmitt. “That is going to change the way R&D is done.”

The third is photonic integration which Schmitt equates to the very early state of the electronics business. While Infinera has done some interesting things with integration, its latest 500 Gigabit PIC (photonic integrated circuit) is a big leap in density, he says: “It will be interesting if that sort of technology crosses over into other applications such as short- and intermediate-reach applications.”

“Nothing in this business changes quickly but the pace of change is starting to accelerate,” says Schmitt. “These three things, when you throw them together in a pot, are going to result in some unpredictable outcomes.”

Chinese optical component vendors set for change

“If [Chinese optical component] companies get $100m from an IPO, they have the resources to really do things”

Vladimir Kozlov, LightCounting

The local OC players have benefitted from the prolonged growth of China’s economy, the rise of global telecom system vendors Huawei and ZTE, and the significant expansion in Chinese operators’ networks. But such domestic growth will not continue and will likely lead to a shake-up of the local OC firms.

“They [Chinese OC players] all have the same industry pitch: they all have huge capacity, they have tons of people and they are growing fast but when you research that, you uncover different approaches to doing business,” says Vladimir Kozlov, CEO at LightCounting.

The market research firm has identified several classes of OC player. There are quite a few mid-size companies that focus on niche local opportunities. “Very few of them have an ambition of becoming a global player,” says Kozlov. “They have been set up with local government support, primarily with the aim of employing local people and being involved in local telecom projects.”

But there are other players with broader ambitions and resources. Companies such as HiSense Broadband and HG Genuine, acknowledged manufacturers of electronics and consumer products, have formed OC business units recognising the growth potential of optical communications.

Another category that Western firms will do well to note, says Kozlov, is the Chinese OC players with a long history such as WTD and Accelink. “WTD is 30-years-old and grew from the Wuhan Research Institute that is also a founding body for Chinese system vendor FiberHome,” says Kozlov. WTD has been growing steadily and the pace has accelerated in the last two years. “WTD is becoming more aggressive and is gaining market share while Accelink has a successful IPO that brought in $100m,” he says.

Other companies will likely follow Accelink’s example and raise money through IPOs. But what will be interesting is whether such companies continue to focus on the Chinese market or start addressing issues such as what technologies they are missing and even make acquisitions, he says.

“A lot more companies will have access to financial markets as the regulation that limits how many companies can become public is relaxed,” says Kozlov. “If [Chinese OC] companies get [US] $100m from an IPO, they have the resources to really do things.”

“It is unlikely that Huawei will keep on growing as fast as it did over recent years and continue to take market share from Alcatel-Lucent, Ericsson and others for much longer”

Yet another Chinese OC player segment is start-ups funded by venture capitalists (VCs). One example is Innolight which has received funding from local VCs and a Western company. “VCs will push firms to be as ambitious as possible as they are after returns,” says Kozlov. Interest among the financial investment community is also growing given the rise of the stock price of the OC industry’s leading firms in the last year. Such interest will likely lead to investment and restructuring of local Chinese firms, he says.

Chinese OC vendors have been helped by the rise of the system vendors Huawei and ZTE. The Chinese equipment makers have been disruptive in adopting technology quickly while reducing their costs. But having become global players, Huawei and ZTE now face their own challenges.

“Both [system vendors] companies have caught up on the technology and the next step for them is to see whether they can become leaders in technology and stay ahead of an Alcatel-Lucent or a Ciena,” says Kozlov. “They have the ambition but can they do it?” Kozlov notes that Chinese companies are now highly active with patent applications: “Chinese firms recognise that this is how they will achieve a longer-term advantage and protect their own technologies.”

Another challenge facing the system vendors, common to many technology industries, is that no one player dominates a market. “Usually three global companies share the dominance; the same if it is a local market,” says Kozlov. “It is therefore unlikely that Huawei will keep on growing as fast as it did over recent years and continue to take market share from Alcatel-Lucent, Ericsson and others for much longer.”

This will require Huawei and ZTE to adapt to more moderate growth in future. Meanwhile North American and European system vendors have long responded to the competitive threat, moving their manufacturing to Asia Pacific - and China in particular - to benefit from reduced operating costs. For the Chinese OC vendors, yet to become global players, the chance to be as disruptive as the Chinese system vendors has gone since leading OC vendors have established local manufacturing.

Can Western companies learn from the experience of Chinese system and OC vendors? Kozlov is not so sure.

The Chinese have proved adept at learning the business and mastering new technologies. The examples of Huawei and ZTE that have disrupted the market by being as efficient as possible have proved a wake-up call for Western companies. “I don’t see anything beyond that that Western companies can learn; it is still the Chinese that are learning from Western companies,” says Kozlov. “This does not mean that the Western companies have nothing to worry about; there is plenty of room for improvement in the industry supply chain.”

Looking at the decade ahead, Kozlov expects Huawei to have a much greater penetration in the North American telecom market. “And as it [Huawei] builds up its own intellectual property, it will be better able to compete with Cisco Systems and H-P in the datacom market,” says Kozlov. And as Chinese companies get access to greater finance he also expects they will start acquiring Western firms to gain expertise and greater access to markets.