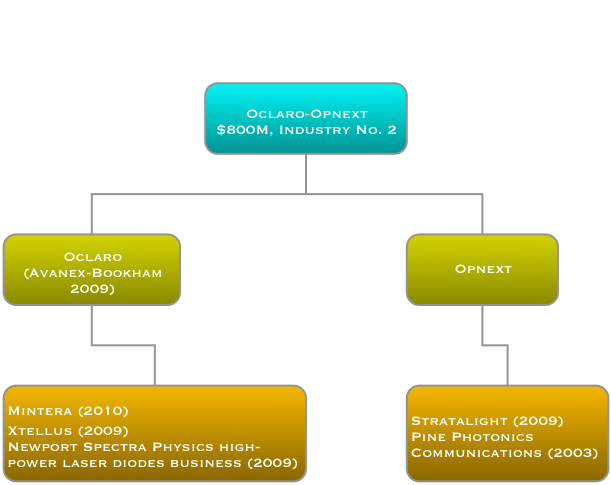

Oclaro-Opnext merger will create second largest optical component company

Oclaro has announced its plan to merge with Opnext. The deal, valued at US $177M, will result in Opnext's shareholders owning 42% of the combined company. The merger of the fifth and sixth largest optical component players, according to Ovum, will create a company with annual revenues of $800M, second only to Finisar. The deal is expected to be completed in the next 3-6 months.

Source: Gazettabyte

Source: Gazettabyte

Other details of the merger include:

- Combining the two companies will save between $35M-45M but will take 18 months to achieve.

- Restructuring and system integration will cost $20M-$30M.

- All five of the new company's fabs will be kept. The fabs are viewed as key assets.

- The new company will continue its use of contract manufacturers in Asia. Oclaro announced a recent deal with Venture, and that included the possibility of an Oclaro-Opnext merger.

- Oclaro's CEO, Alain Couder, will become the CEO of the new company. Harry Bosco, Opnext's CEO, will join the company's board of directors, made up of six Oclaro and four Opnext members.

- In 4Q 2011, Oclaro reported three customers, each accounting for greater than 10% sales: Fujitsu, Infinera and Ciena. Opnext reported 43% of its sales to Cisco Systems and Hitachi in the same period.

Industry scale

The motivation for the merger is to achieve industry scale, says Oclaro. "We have never been shy [of mergers and acquisitions] - we did Avanex and Bookham," says Yves LeMaitre, chief marketing officer for Oclaro. "We believe industry scale allows you to absorb certain fixed costs like fab infrastructure and the sales force." Scale also increases the absolute amount that can be invested in R&D, estimated at 12-13% of its revenues.

"It [the acquisition] is really about building a company that directly competes with Finisar," says Daryl Inniss, practice leader, components at Ovum. "It creates a stronger, vertically integrated company that starts at chips and goes all the way to the line card."

"We will be one of the most vertically integrated suppliers for 100 Gigabit coherent technology"

Mike Chan, Opnext

LightCounting believes the Oclaro-Opnext merger will be a success. Moreover, the market research firm expects further optical component M&As. Since the Oclaro-Opnext was announced, Sumitomo Electric Device Innovations has announced it will acquire Emcore's VCSEL and associated transceiver technology for $17M.

Meanwhile, Morgan Stanley Research is less positive about the merger, believing that the Opnext acquisition carries 'material risk'. It argues that the stated synergies are aggressive and that the integration of the two firms could distract Oclaro and lower its share price.

Products and technology

The deal expands Oclaro's transceiver portfolio, enhancing its offerings in telecom and strengthening its presence in datacom. It also expands the customer base: Opnext supplies Juniper, Google and H-P, new customers for Oclaro.

Common products shared by the two firms are limited, for high-end products the overlap is mainly 100 Gigabit coherent and tunable laser XFPs. LightCounting also points out that the two share some legacy SONET/SDH, WDM and Ethernet products: "Nothing that reduces competition significantly," it says in a research note.

"[With the Avanex-Bookham merger] There was a little bit of overlap in a few areas which we managed," says Oclaro's LeMaitre. "It is even easier in this case."

"We see potential, further down the road, for new very-short-reach optical interfaces"

Yves LeMaitre, Oclaro

Opnext acquired optical transmission subsystem vendor StrataLight in 2009 while Oclaro acquired Mintera in 2010. Both Oclaro and Opnext have used the expertise of the two subsystem vendors to become early market entrants of 100 Gigabit 168-pin multi-source modules.

But Oclaro makes the optical components for the modules - tunable lasers, lithium niobate modulators and integrated coherent transceivers - items that Opnext has to buy for its 100 Gig coherent module, says Ovum's Inniss: "Opnext has built decent gross margins when you consider that a lot of the optics they don't own themselves.” Oclaro's components will be used within Opnext's modules.

"We will be one of the most vertically integrated suppliers for key 100 Gigabit coherent technology moving forward," says Mike Chan, executive vice president of business development and marketing at Opnext.

Opnext stresses that it has its own programmes for integrated photonics. "We have been telling our customers that we have been working on some of these integrated photonics [for 100G coherent]," says Chan. "The StrataLight portion of Opnext also has a lot of work done, and IP created, in the coherent modem area."

Currently both companies' 100 Gigabit modules use NEL's coherent receiver DSP-ASIC. Oclaro has also made an investment in coherent chip start-up, ClariPhy. But for future coherent adaptive-rate designs, the joint company will be able to develop its own coherent chip. "We have the in-house know-how for the coherent modem chip," says Chan.

The merged company is well positioned to address client-side 100 Gigabit-ber-second (Gbps) transceivers. "Here the challenge is to achieve high density and low power [interfaces]," says Chan. Oclaro has VCSEL technology that can be used for very short reach 4x28Gbps arrays. Oclaro says it is the world's leading supplier of VCSELs for a variety of commercial applications and has now shipped over 150M units.

At OFC/NFOEC Opnext demonstrated a 1310nm LISEL (Lens-integrated Surface-Emitting distributed feedback Laser) array operating at 25-40Gbps. The surface-emitting distributed feedback (DFB) laser can also be used for the same 4x28Gbps design, says Chan. "Within the data centre 500m is the sweet-spot," says Chan. "It is not just the physical distance but the link-budget as the signal may have to go through a patch panel." The DFB can be used with multi-mode and single-mode fibre and Opnext believes it can achieve a 1km reach.

Oclaro does not rule out using its VCSEL technology to address such applications as optical engines, connecting racks and for backplanes. "We see potential, further down the road, for new very-short-reach optical interfaces into consumer, backplane, and board-to-board to really expand our addressable market," says LeMaitre

Further mergers

LightCounting argues that the 2011 floods in Thailand have added urgency to industry consolidation, with the Oclaro and Opnext merger being the first of several. Oclaro and Opnext were among the most impacted by the flood with Q4 2011 revenues being down 18% and 38%, respectively, says LightCounting.

Ovum also expects further mergers as companies strengthen their coherent and ROADM technologies.

Inniss believes ROADMs is the next area that Oclaro is likely to strengthen. Oclaro has acquired Xtellus but Ovum says the main ROADM leaders are Finisar, JDS Uniphase and CoAdna. Companies to watch include JDS Uniphase, Fujitsu Optical Components, CoAdna and Sumitomo, says Inniss.

A day after Ovum's and LightCounting's M&A comments, Sumitomo announced the acquisition of Emcore's VCSEL business unit.

100 Gigabit direct detection gains wider backing

More vendors are coming to market with 100 Gigabit direct detection products for metro and private networks.

The emergence of a second de-facto 100 Gigabit standard, a complement to 100 Gigabit coherent, has gained credence with 4x28 Gigabit-per-second (Gbps) direct detection announcements from Finisar and Oclaro, as well as backing from system vendor, ECI Telecom.

"We believe that in some cases operators will prefer to go with this technology instead of coherent"

Shai Stein, CTO, ECI Telecom

ECI Telecom and chip vendor MultiPhy announced at OFC/NFOEC that they have been collaborating to develop a 168-pin MSA, 5x7-inch 100 Gigabit-per-second (Gbps) direct detection module. Finisar and Oclaro used the show held in Los Angeles to announce their market entry with 100Gbps direct detection CFP pluggable optical modules.

Late last year ADVA Optical Networking announced the industry's first 100Gbps direct detection product. At the same time, MultiPhy detailed its MP1100Q receiver chip designed for 100Gbps direct detection.

According to ECI, by having the 168-pin MSA interface, one line card can support a 100Gbps coherent transponder or the 100Gbps direct detection. "This is important as it enables us to fit the technology and price to the needs of end customers," says Shai Stern, CTO of ECI Telecom.

100 Gigabit transmission

Coherent technology has become the de-facto standard for 100Gbps long-haul transmission. Using dense wavelength division multiplexing (DWDM), system vendors can achieve 1,500km and greater reaches using a 50GHz channel.

But coherent designs are relatively costly and 100Gbps direct detection offers a cost-conscious alternative for metro networks and for linking data centres, achieving a reach of up to 800km.

"It [100 Gig direct detection] provides needed performance at an attractive cost, in particular when you are looking at private optical networks," says Per Hansen, vice president of product marketing, optical networks solutions at Oclaro.

Such networks need not be owned by private enterprises, they can belong to operators, says Hansen, but they are typically simple point-to-point connections or 3- to 4-node rings serving enterprises. "Bonding adjacent [4x28Gbps] wavelengths to create a 100Gbps channel that connects efficiently to your [IP] router is very attractive in such networks," says Hansen.

For more complex mesh metro networks, coherent is more attractive. "Simply because of the spectral resources being taken up through the mesh [with 4x28Gbps], and the operational aspect of routeing that," says Hansen.

ECI Telecom says that it has yet to decide whether it will adopt 100Gbps direct detection. But it does see a role for the technology in the metro since the 100Gbps technology works well alongside networks with 10 and 40 Gigabit on-off keying (OOK) channels. "We believe that in some cases operators will prefer to go with this technology instead of coherent," says Stein.

Some operators have chosen to deploy coherent over new overlay networks, to avoid the non-linear transmission effects that result from mixing old and new technologies on the one network. "With this technology, operators can stay with their existing networks yet benefit from 100 Gig high capacity links," says Stein.

Finisar says 100Gbps direct detection is also suited to low-latency applications. "The fact that it is not coherent means it doesn't include a DSP chip, enabling it to be used for low latency applications," says Rafik Ward, vice president of marketing at Finisar.

Implementation

The announced 100Gbps direct detection designs all use 4x28Gbps channels and optical duo-binary (ODB) modulation, although MultiPhy also promotes an 80km point-to-point OOK version (see Table).

Source: Gazettabyte

Source: Gazettabyte

The module input is a 10x10Gbps electrical interface: a CFP interface or the 168-pin line side MSA. A 'gearbox' IC is used to translate between the 10x10Gbps electrical interface and the four 28Gbps channels feeding the optics.

"There are a few suppliers that are offering that [gearbox IC]," says Robert Blum, director of product marketing for Oclaro's photonic components. AppliedMicro recently announced a duplex multiplexer-demultiplexer IC.

MultiPhy's receiver chip has a digital signal processor (DSP) that implements the maximum likelihood sequence estimation (MLSE) algorithm, which is says enables 10 Gig opto-electronics to be used for each channel. The result is a 100Gbps module based on the cost of 4x10Gbps optics. However, over-driving the 10Gbps opto-electronics creates inter-symbol interference, where the energy of a transmitted bit leaks into neighbouring signals. MultiPhy's DSP using MLSE counters the inter-symbol interference.

100G direct detection module showing MultiPhy's MP1100Q chip. Source: MultiPhy

100G direct detection module showing MultiPhy's MP1100Q chip. Source: MultiPhy

Oclaro and Finisar claim that using ODB alone enables the use of lower-speed opto-electronics. "This is irrespective of whether you use MLSE or hard decision," says Blum. "The advantage of using optical duo-binary modulation is that you can use 10G-type optics."

Finisar's Ward points out that by using ODB, the 100Gbps direct-detection module avoids the price/ power penalty associated with a receiver DSP running MLSE to compensate for sub-optimal optical components.

Oclaro, however, has not ruled out using MLSE in future. The company endorsed MultiPhy's MLSE device when the product was first announced but its first 100G transceiver is not using the IC.

Finisar and Oclaro's modules require 200GHz to transmit the 100Gbps signal: 4x50GHz channels, each carrying the 28Gbps signal. "This architecture will enable 2.5x the spectral efficiency of tunable XFPs," says Ward. Using XFPs, ten would be needed for a 100Gbps throughput, each channel requiring 50GHz or 500GHz in total.

MultiPhy claims that it can implement the 100Gbps in a 100GHz channel, 5x the efficiency but still twice the spectrum used for 100Gbps coherent.

Finisar demonstrated its 100Gbps CFP module with SpectraWave, a 1 rack unit (1U) DWDM transport chassis, at OFC/NFOEC. "It provides all the things you need in line to enable a metro Ethernet link: an optical multiplexer and demultiplexer, amplification and dispersion compensation," says Ward. Up to four CFPs can be plugged into the SpectraWave unit.

Operator interest

In a recent survey published by Infonetics Research, operators had yet to show interest in 100Gbps direct detection. Infonetics attributed the finding to the technology still being unavailable and that operators hadn't yet assessed its merits.

"Operators are aware of this technology," says ECI's Stein. "It is true they are waiting to get a proof-of-concept and to test it in their networks and see the value they can get.

"That is why ECI has not yet decided to go for a generally-available product: we will deliver to potential customers, get their feedback and then take a decision regarding a commercial product," says Stein.

However MultiPhy claims that this is the first technology that enables 100Gbps in a pluggable module to achieve a reach beyond 40km. That fact coupled with the technology's unmatched cost-performance is what is getting the interest. "Every time you show a potential user some way they can save on cost, they are interested," says Neal Neslusan, vice president of sales and marketing at MultiPhy.

Direct detection roadmap

Recent announcements by Cisco Systems, Ciena, Alcatel-Lucent and Huawei highlight how the system vendors will use advanced modulation and super-channels to evolve coherent to speeds beyond 100Gbps. Does direct detection have a similar roadmap?

"I don't think that this on-off keying technology is coming instead of coherent," says Stein. "Once we move to super-channel and the spectral densities it can achieve, coherent technology is a must and will be used." But for 40Gbps and 100Gbps, what ECI calls intermediate rates, direct detection extends the life of OOK and existing network infrastructure.

ECI and MultiPhy are members of the Tera Santa Consortium developing 1 Terabit coherent technology, and MultiPhy stresses that as well as its direct detection DSP chips, it is also developing coherent ICs.

Further reading: 100 Gigabit: The coming metro opportunity

PMC-Sierra delivers silicon for 10 Gigabit EPON

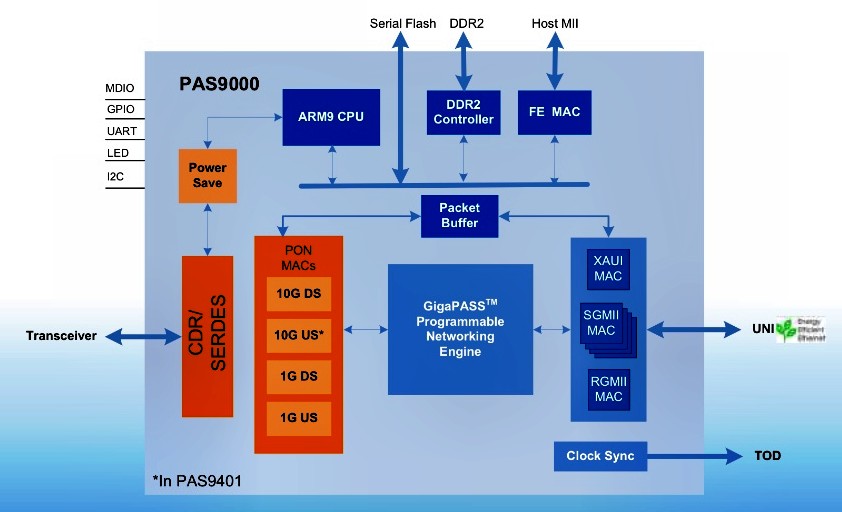

PMC-Sierra has announced the availability of symmetric 10 Gigabit EPON chips. The devices complete the company's 10 Gigabit PON portfolio which also includes XGPON designs.

The 10G-EPON devices comprise two PAS9000 optical networking unit (ONU) and four PAS8000 optical line terminal (OLT) chips that support asymmetrical and symmetrical 10G-EPON: 10Gbps downstream (to the user) and 1Gbps upstream, and 10Gbps downstream and upstream, respectively. PMC-Sierra claims it is the first to market with a dual-mode 10G-EPON ONU device.

The PAS9000 optical network unit chip architecture. There are two devices in the family. One, the PAS9401, also supports 10G-EPON symmetric mode. Source: PMC-Sierra.

The PAS9000 optical network unit chip architecture. There are two devices in the family. One, the PAS9401, also supports 10G-EPON symmetric mode. Source: PMC-Sierra.

PON Market

PMC-Sierra says that the total market for PON is set for strong growth through 2015.

Using market data from Gartner and IDC, PMC says the 2010 market for EPON silicon was US $120M, growing to $180M for EPON and 10G-EPON speeds in 2015. In contrast, the GPON market was $35M in 2010 but will total $175M for both GPON and XGPON by 2015.

"China is going to be a very large market [for PON] compared to elsewhere," says Rammy Bahalul, senior marketing manager, FTTH division at PMC-Sierra.

Field trials of 10G-EPON have already been conducted in South Korea, Japan and China, says Bahalul: "We see Japan being the first to move to 10G-EPON, followed by Korea and China."

PMC expects 10G-EPON deployments to start in 2013, with the first application being multi-dwelling units. Meanwhile, the company expects first deployments of XGPON in 2014, with field trials starting in 2013. China is expected to deploy XGPON first, followed by North America.

10G-EPON ICs

The 40nm CMOS PAS8000 OLT family comprises four devices.

The PAS8301 and PAS8311 support asymmetric (1Gbps upstream) 10G-EPON. The two chips differ in that the PAS8311 has an on-chip traffic manager/ packet processor which inspects and classifies packets as well as rate-limits particular service flows.

The remaining two devices, the PAS8401 and PAS8411, support symmetric and asymmetric modes. However, the PAS8401 does not include the traffic manager/ packet processor.

All four have the Power Save mode which PMC claims halves the power consumption compared to existing ONUs. For example, it allows the ONU to be shut down when appropriate. The OLT devices also support synchronisation protocols required for mobile backhaul.

Another feature of the PAS8000 family is an on-chip optical time-domain reflectometer (OTDR). The OTDR function enables operators to locate fibre faults without using standalone test equipment, and can diagnose the nature and location of a fault to within a 2m accuracy, says Bahalul.

The PAS9000 ONU family comprises two devices: the asymmetric PAS9301 and the asymmetric/ symmetric PAS9401. The devices support the power save mode and mobile backhaul. And by delivering 10G-EPON symmetric and asymmetric modes, the PAS9401 ONU IC enables operators to plan five years ahead using silicon available now, says Bahalul.

Meanwhile, the company's XGPON OLT and ONU are asymmetric designs - 10Gbps downstream and 2.5Gbps upstream. The system-on-chip XGPON versions have still to be taped out with the designs currently implemented as FPGAs. The XGPON design was part of a recent successful interoperability test, conducted by industry body FSAN (Full Service Access Network), says PMC.

PMC-Sierra says it has a single software development kit that allows software developed on one platform to be reused across all its products.

The post-100 Gigabit era

Feature: Beyond 100G - Part 4

The latest coherent ASICs from Ciena and Alcatel-Lucent coupled with announcements from Cisco and Huawei highlight where the industry is heading with regard high-speed optical transport. But the announcements also raise questions too.

Source: Gazettabyte

Source: Gazettabyte

Observations and queries

- Optical transport has had a clear roadmap: 10 to 40 to 100 Gigabit-per-second (Gbps). 100Gbps optical transport will be the last of the fixed line-side speeds.

- After 100Gbps will come flexible speed-reach deployments. Line-side optics will be able to implement 50Gbps, 100Gbps, 200Gbps or even faster speeds with super-channels, tailored to the particular link.

- Variable speed-reach designs will blur the lines between metro and ultra long-haul. Does a traditional metro platform become a trans-Pacific submarine system simply by adding a new line card with the latest coherent ASIC boasting transmit and receive digital signal processors (DSPs), flexible modulation and soft-decision forward error correction?

Source: Gazettabyte

Source: Gazettabyte

- The cleverness of optical transport has shifted towards electronics and digital signal processing and away from photonics. Optical system engineers are being taxed as never before as they try to extend the reach of 100, 200 and 400Gbps to match that of 10 and 40Gbps but what is key for platform differentiation is the DSP algorithms and ASIC design.

- Optical is the new radio. This is evident with the adding of a coherent transmit DSP that supports the various modulation schemes and allows spectral shaping, bunching carriers closer to make best use of the fibre's bandwidth.

- The radio analogy is fitting because fibre bandwidth is becoming a scarce resource. Usable fibre capacity has more than doubled with these latest ASIC announcements. Moving to 400Gbps doubles overall capacity to some 18 Terabits. Spectral shaping boosts that even further to over 23 Terabits. Last week 8.8 Terabits (88x100Gbps) was impressive.

- Maximising fibre capacity is why implementing single-carrier 100Gbps signals in 50GHz channels is now important.

- Super-channels, combining multiple carriers, have a lot of operational merits (see the super-channel section in the Cisco story). Infinera announced its 500Gbps super-channel over 250GHz last year. Now Ciena and Alcatel-Lucent highlight how a dual-carrier, dual-polarisation 16-QAM approach in 100GHz implements a 400Gbps signal.

- Despite all the talk of 16-QAM and 400Gbps wavelengths, 100Gbps is still in its infancy and will remain a key technology for years to come. Alcatel-Lucent, one of the early leaders in 100Gbps, has deployed 1,450 100 Gig line units since it launched its system in June 2010.

- Photonic integration for coherent will remain of key importance. Not so much in making yet more complex optical structures than at 100Gbps but shrinking what has already been done.

- Is there a next speed after 100Gbps? Is it 200Gbps until 400Gbps becomes established? Is it 500Gbps as Infinera argues? The answer is that it no longer matters. But then what exactly will operators use to assess the merits of the different vendors' platforms? Reach, power, platform density, spectral efficiency and line speeds are all key performance parameters but assessing each vendor's platform has clearly got harder.

- It is the system vendors not the merchant chip makers that are driving coherent ASIC innovation. The market for 100Gbps coherent merchant chips will remain an important opportunity given the early status of the market but how will coherent merchant chip vendors compete, several of them startups, with the system vendors' deeper pockets and sophisticated ASIC designs?

- Optical transponder vendors at least have more scope for differentiation but it is now also harder. Will one or two of the larger module makers even acquire a coherent ASSP maker?

- Infinera announced its 100G coherent system last year. Clearly it is already working on its next-generation ASIC. And while its DTN-X platform boasts a 500Gbps super-channel photonic chip, its overall system capacity is 8 Terabit (160x50Gbps, each in 25GHz channels). How will Infinera respond, not only with its next ASIC but also its next-generation PIC, to these latest announcements from Ciena and Alcatel-Lucent?

Latest coherent ASICs set the bar for the optical industry

Feature: Beyond 100G - Part 3

Alcatel-Lucent has detailed its next-generation coherent ASIC that supports multiple modulation schemes and allow signals to scale to 400 Gigabit-per-second (Gbps).

The announcement follows Ciena's WaveLogic 3 coherent chipset that also trades capacity and reach by changing the modulation scheme.

"They [Ciena and Alcatel-Lucent] have set the bar for the rest of the industry," says Ron Kline, principal analyst for Ovum’s network infrastructure group.

"We will employ [the PSE] for all new solutions on 100 Gigabit"

"We will employ [the PSE] for all new solutions on 100 Gigabit"

Kevin Drury, Alcatel-Lucent

Photonic service engine

Dubbed the photonic service engine (PSE), Alcatel-Lucent's latest ASIC will be used in 100Gbps line cards that will come to market in the second half of 2012.

The PSE compromises coherent transmitter and receiver digital signal processors (DSPs) as well as soft-decision forward error correction (SD-FEC). The transmit DSP generates the various modulation schemes, and can perform waveform shaping to improve spectral efficiency. The coherent receiver DSP is used to compensate for fibre distortions and for signal recover.

The PSE follows Alcatel-Lucent's extended reach (XR) line card announced in December 2011 that extends its 100Gbps reach from 1,500 to 2,000km. "This [PSE] will be the chipset we will employ for all new solutions on 100 Gigabit," says Kevin Drury, director of optical marketing at Alcatel-Lucent. The PSE will extend 100Gbps reach to over 3,000km.

Ciena's WaveLogic 3 is a two-device chipset. Alcatel-Lucent has crammed the functionality onto a single device. But while the device is referred to as the 400 Gigabit PSE, two PSE ASICs are needed to implement a 400Gbps signal.

"They [Ciena and Alcatel-Lucent] have set the bar for the rest of the industry"

Ron Kline, Ovum

"There are customers that are curious and interested in trialling 400Gbps but we see equal, if not higher, importance in pushing 100Gbps limits," says Manish Gulyani, vice president, product marketing for Alcatel-Lucent's networks group.

In particular, the equipment maker has improved 100Gbps system density with a card that requires two slots instead of three, and extends reach by 1.5x using the PSE.

Performance

Alcatel-Lucent makes several claims about the performance enhancements using the PSE:

- Reach: The reach is extended by 1.5x.

- Line card density: At 100Gbps the improvement is 1.5x. The current 100Gbps muxponder (10x10Gbps client input) and transponder (100Gbps client) line card designs occupy three slots whereas the PSE design will occupy two slots only. Density will be improved by 4x by adopting a 400Gbps muxponder that occupies three slots.

- Power consumption: By going to a more advanced CMOS process and by enhancing the design of the chip architecture, the PSE consumes a third less power per Gigabit of transport: from 650mW/Gbps to 425mW/Gbps. Alcatel-Lucent is not saying what CMOS process technology is used for the PSE. The company's current 100Gbps silicon uses a 65nm process and analysts believe the PSE uses a 40nm process.

- System capacity: The channel width occupied by the signal can be reduced by a third. A 50GHz 100Gbps wavelength can be compressed to occupy a 37.5GHz. This would improve overall 100Gbps system capacity from 8.8 Terabit-per-second (Tbps) to 11.7Tbps. Overall capacity can be improved from 88, 100Gbps ports to 44, 400Gbps interfaces. That doubles system capacity to 17.6Tbps. Using waveform shaping, this is improved by a further third, to greater than 23Tbps.

"We are not saying we are breaking the 50GHz channel spacing today and going to a flexible grid, super-channel-type construct," says Drury. "But this chip is capable of doing just that." Alcatel-Lucent will at least double network capacity when its system adopts 44 wavelengths, each at 400Gbps.

400 Gigabit

To implement a 400Gbps signal, a dual-carrier, dual-polarisation 16-QAM coherent wavelength is used that occupies 100GHz (two 50GHz channels). Alcatel-Lucent says that should it commercialise 400Gbps using waveform shaping, the channel spacing would reduce to 75GHz. But this more efficient grid spacing only works alongside a flexible grid colourless, directionless and contentionless (CDC) ROADM architecture.

A 400Gbps PSE card showing four 100 Gigabit Ethernet client signals going out as a 400Gbps wavelength. The three-slot card is comprised of three daughter boards. Source: Alcatel-Lucent.

A 400Gbps PSE card showing four 100 Gigabit Ethernet client signals going out as a 400Gbps wavelength. The three-slot card is comprised of three daughter boards. Source: Alcatel-Lucent.

Alcatel-Lucent is not ready to disclose the reach performance it can achieve with the PSE using the various modulation schemes. But it does say the PSE supports dual-polarisation bipolar phase-shift keying (DP-BPSK) for longest reach spans, as well as quadrature phase-shift keying (DP-QPSK) and 16-QAM (quadrature amplitude modulation).

"[This ability] to go distances or to sacrifice reach to increase bandwidth, to go from 400km metro to trans-Pacific by tuning software, that is a big advantage," says Ovum's Kline. "You don't then need as many line cards and that reduces inventory."

Market status

Alcatel-Lucent says that it has 55 customers that have deployed over 1,450 100Gbps transponders.

A software release later this year for Alcatel-Lucent's 1830 Photonic Service Switch will enable the platform to support 100Gbps PSE cards.

A 400Gbps card will also be available this year for operators to trial.

Cisco Systems' 100 Gigabit spans metro to ultra long-haul

Cisco Systems has demonstrated 100 Gigabit transmission over a 3,000km span. The coherent-based system uses a single carrier in a 50GHz channel to transmit at 100 Gigabit-per-second (Gbps). According to Cisco, no Raman amplification or signal regeneration is needed to achieve the 3,000km reach.

Feature: Beyond 100G - Part 2

"The days of a single modulation scheme on a part are probably going to come to an end in the next two to three years"

Greg Nehib, Cisco

The 100Gbps design is also suited to metro networks. Cisco's design is compact to meet the more stringent price and power requirements of metro. The company says it can fit 42, 100Gbps transponders in its ONS 15454 Multi-service Transport Platform (MSTP), which is a 7-foot rack. "We think that is double the density of our nearest competitor today," claims Greg Nehib, product manager, marketing at Cisco Systems.

Also shown as part of the Cisco demonstration was the use of super-channels, multiple carriers that are combined to achieve 400 Gigabit or 1 Terabit signals.

Single-carrier 100 Gigabit

Several of the first-generation 100Gbps systems from equipment makers use two carriers (each carrying 50Gbps) in a 50GHz channel, and while such equipment requires lower-speed electronics, twice as many coherent transmitters and receivers are needed overall.

Alcatel-Lucent is one vendor that has a single-carrier 50GHz system and so has Huawei. Ciena via its Nortel acquisition offers a dual-carrier 100Gbps system, as does Infinera. With Ciena's announcement of its WaveLogic 3 chipset, it is now moving to a single-carrier solution. Now Cisco is entering the market with a single-carrier system.

"When you have a single carrier, you can get upwards of 96 channels of 100Gbps in the C-band," says Nehib. "The equation here is about price, performance, density and power."

What has been done

Cisco's 100Gbps design fits on a 1RU (rack unit) card and uses the first 100Gbps coherent receiver ASIC designed by the CoreOptics team acquired by Cisco in May 2010.

The demonstrated 3,000km reach was made using low-loss fibre. "This is to some degree a hero experiment," says Nehib. "We have achieved 3,000km with SMF ULL fibre from Corning; the LL is low loss." Normal fibre has a loss of 0.20-0.25dB/km while for ULL fibre it is in the 0.17dB/km range.

"You can do the maths and calculate the loss we are overcoming over 3,000km. We just want to signal that we have very good performance for ultra long-haul," says Nehib, who admits that results will vary in networks, depending on the fibre.

Nehib says Cisco's coherent receiver achieves a chromatic dispersion tolerance of 70,000 ps/nm and 100ps differential group delay. Differential group delay is a non-linear effect, says Nehib, that is overcome using the DSP-ASIC. The greater the group delay tolerance, the better the distance performance. These metrics, claims Cisco, are currently unmatched in the industry.

The company has not said what CMOS process it is using for its ASIC design. But this is not the main issue, says Nehib: "We are trying to develop a part that is small so that it fits in many different platforms, and we can now use a single part number to go from metro performance all the way to ultra long-haul."

Another factor that impacts span performance is the number of lit channels. Cisco, in the test performed by independent test lab EANTC, the European Advanced Network Test Center, used 70 wavelengths. "With 70 channels the performance would have been very close to what we would have achieved with [a full complement of] 80 channels," says Nehib.

Super-channels

A super-channel refers to a signal made up of several wavelengths. Infinera, with its DTN-X, uses a 500Gbps super-channel, comprising five 100Gbps wavelengths.

Using a super-channel, an operator can turn up multiple 100Gbps channels at once. If an operator wants to add a 100Gbps wavelength, a client interface is simply added to a spare 100Gbps wavelength making up the super-channel. In contrast turning up a 100Gbps wavelength in current systems usually requires several days of testing to ensure it can carry live traffic alongside existing links.

Another benefit of super-channels is scale by turning up multiple wavelengths simultaneously. As traffic grows so does the work load on operators' engineering teams. Super-channels aid efficiency.

"There is one other point that we hear quite often," says Nehib. "One other attraction of super-channels is overall spectral efficiency." The carriers that make up the signal can be packed more closely, expanding overall fibre capacity.

"Just like with 10 Gig, we think at some point in the future the 100 Gig network will be depleted, especially in the largest networks, and operators will be interested in 400 Gig and Terabit interfaces," says Nehib. "If that wavelength can further benefit from advanced modulation schemes and super-channels through flex[ible] spectrum deployment then you can get more total bandwidth on the fibre and better utilisation of your amplifiers."

Cisco's 100Gbps lab demonstration also showed 400 Gigabit and 1 Terabit super-channels, part of its research work with the Politechnico di Torino. "We are going to move on to other advanced modulation techniques and deliver 400 Gigabit and Terabit interfaces in future," says Nehib.

Existing 100Gbps systems use dual-polarisation, quadrature phase-shift keying (DP-QPSK). Using 16-QAM (quadrature amplitude modulation) at the same baud rate doubles the data rate. Using 16-QAM also benefits spectral utilisation. If the more intelligent modulation format is used in a super-channel format, and the signal is fitted in the most appropriate channel spacing using flexible spectrum ROADMs, overall capacity is increased. However, the spectral efficiency of 16-QAM comes at the expense of overall reach.

"You are able to best match the rate to the reach to the spectrum," says Nehib. "The days of a single modulation scheme on a part are probably going to come to an end in the next two to three years."

Cisco has yet to discuss the addition of a coherent transmitter DSP which through spectral shaping can bunch wavelengths. Such an approach has just been detailed by Ciena with its WaveLogic 3 and Alcatel-Lucent with its 400 Gig photonic service engine.

For the Terabit super-channel demonstration, Cisco used 16-QAM and a flexible spectrum multiplexer. "The demo that we showed is not necessarily indicative of the part we will bring to market," says Nehib, pointing out that it is still early in the development cycle. "We are looking at the spectral efficiency of super-channels, different modulation schemes, flex-spectrum multiplexer, availability, quality, loss etc.," says Nehib. "We have not made firm technology choices yet."

Cisco's 100Gbps system is in trials with some 40 customers and can be ordered now. The product will be generally available in the near future, it says.

Further reading:

Light Reading: EANTC's independent test of Cisco's CloudVerse architecture. Part 4: Long-haul optical transport

Altera optical FPGA in 100 Gigabit Ethernet traffic demo

Altera is demonstrating its optical FPGA at OFC/NFOEC, being held in Los Angeles this week. The FPGA, coupled to parallel optical interfaces, is being used to send and receive 100 Gigabit Ethernet packets of various sizes.

The technology demonstrator comprises an Altera Stratix IV FPGA with 28, 11.3Gbps electrical transceivers coupled to two Avago Technologies' MicroPod optical modules.

"FPGAs are now being used for full system level solutions"

"FPGAs are now being used for full system level solutions"

Kevin Cackovic, Altera

The MicroPods - a 12x10Gbps transmitter and a 12x10Gbps optical transceiver - are co-packaged with the FPGA. "All the interconnect between the serdes and the optics are on the package, not on the board," says Steve Sharp, marketing program manager, fiber optic products division at Avago. Such a design benefits signal integrity and power consumption, he says: "It opens up a different world for FPGA users, and for system integration for optic users."

Both Altera and Avago stress that the optical FPGA has been designed deliberately using proven technologies. "We wanted to focus on demonstrating the integration of the optics, not pushing either of the process technologies to the absolute edge," says Sharp.

The nature of FPGA designs has changed in recent years, says Kevin Cackovic, senior strategic marketing manager of Altera's transmission business unit. Many designs no longer use FPGAs solely to interface application-specific standard products to ASICs, or as a co-processor. "FPGAs are now being used for full system level solutions, things like a framer or MAC technology, forward error correction at very high rates, mapper engines, packet processing and traffic management," he says.

Having its FPGAs in such designs has highlighted for Altera current and upcoming system bottlenecks. "This is what is driving our interest in looking at this technology and what is possible integrating the optics into the FPGA," says Cackovic. Applications requiring the higher bandwidth and the greater reach of optical - rack-to-rack rather than chip-to-module - include next-generation video, cloud computing and 3D gaming, he says.

Altera has still to announce its product plans regarding the optical FPGA dsign. Meanwhile Avago says it is looking at higher-speed versions of MicroPod.

"The request for higher line rates is obviously there," says Sharp. "Whether it goes all the way to 28 [Gigabit] or one of the steps in-between, we are not sure yet."

Ciena: Changing bandwidth on the fly

Ciena has announced its latest coherent chipset that will be the foundation for its future optical transmission offerings. The chipset, dubbed WaveLogic 3, will extend the performance of its 100 Gigabit links while introducing transmission flexibility that will trade capacity with reach.

Feature: Beyond 100 Gigabit - Part 1

"We are going to be deployed, [with WaveLogic 3] running live traffic in many customers’ networks by the end of the year"

"We are going to be deployed, [with WaveLogic 3] running live traffic in many customers’ networks by the end of the year"

Michael Adams, Ciena

"This is changing bandwidth modulation on the fly," says Ron Kline, principal analyst, network infrastructure group at market research firm, Ovum. “The capability will allow users to dynamically optimise wavelengths to match application performance requirements.”

WaveLogic 3 is Ciena's third-generation coherent chipset that introduces several firsts for the company.

- The chipset supports single-carrier 100 Gigabit-per-second (Gbps) transmission in a 50GHz channel.

- The chipset includes a transmit digital signal processor (DSP) - which can adapt the modulation schemes as well as shape the pulses to increase spectral efficiency. The coherent transmitter DSP is the first announced in the industry.

- WaveLogic 3's second chip, the coherent receiver DSP, also includes soft-decision forward error correction (SD-FEC). SD-FEC is important for high-capacity metro and regional, not just long-haul and trans-Pacific routes, says Ciena.

The two-ASIC chipset is implemented using a 32nm CMOS process. According to Ciena, the receiver DSP chip, which compensates for channel impairments, measures 18 mm sq. and is capable of 75 Tera-operations a second.

Ciena says the chipset supports three modulation formats: dual-polarisation bipolar phase-shift keying (DP-BPSK), quadrature phase-shift keying (DP-QPSK) and 16-QAM (quadrature amplitude modulation). Using a single carrier, these equate to 50Gbps, 100Gbps and 200Gbps data rates. Going to 16-QAM may increase the data rate to 200Gbps but it comes at a cost: a loss in spectral efficiency and in reach.

"This software programmability is critical for today's dynamic, cloud-centric networks," says Michael Adams, Ciena’s vice president of product & technology marketing.

WaveLogic 3 has also been designed to scale to 400Gbps. "This is the first programmable coherent technology scalable to 400 Gig," says Adams. "For 400 Gig, we would be using a dual-carrier, dual-polarisation 16-QAM that would use multiple [WaveLogic 3] chipsets."

Performance

Ciena stresses that this is a technology not a product announcement. But it is willing to detail that in a terrestrial network, a single carrier 100Gbps link using WaveLogic 3 can achieve a reach of 2,500+ km. "These refer to a full-fill [wavelengths in the C-Band] and average fibre," says Adams. "This is not a hero test with one wavelength and special [low-loss] fibre.”

Metro to trans-Pacific: The different reaches and distances over terrestrial and submarine using Ciena's WaveLogic 3. SC stands for single carrier. Source: Ciena/ Gazettabyte

Metro to trans-Pacific: The different reaches and distances over terrestrial and submarine using Ciena's WaveLogic 3. SC stands for single carrier. Source: Ciena/ Gazettabyte

When the modulation is changed to BPSK, the reach is effectively doubled. And Ciena expects a 9,000-10,000km reach on submarine links.

The same single-carrier 50GHz channel reverting to 16-QAM can transmit a 200Gbps signal over distances of 750-1,000km. "A modulation change [to 16-QAM] and adding a second 100 Gigabit Ethernet transceiver and immediately you get an economic improvement," says Adams.

For 400Gbps, two carriers, each 16-QAM, are needed and the distances achieved are 'metro regional', says Ciena.

The transmit DSP also can implement spectral shaping. According to Ciena, by shaping the signals sent, a 20-30% bandwidth improvement (capacity increase) can be achieved. However that feature will only be fully exploited once networks deploy flexible grid ROADMs.

At OFC/NFOEC. Ciena will be showing a prototype card that will demonstrate the modulation going from BPSK to QPSK to 16-QAM. "We are going to be deployed, running live traffic in many customers’ networks by the end of the year," says Adams.

Analysis

Sterling Perrin, senior analyst, Heavy Reading

Heavy Reading believes Ciena's WaveLogic 3 is an impressive development, compared to its current WaveLogic 2 and to other available coherent chipsets. But Perrin thinks the most significant WaveLogic 3 development is Ciena’s single-carrier 100Gbps debut.

Until now, Ciena has used two carriers within a 50GHz, each carrying 50Gbps of data.

"The dual carrier approach gave Ciena a first-to-market advantage at 100Gbps, but we have seen the vendor lose ground as Alcatel-Lucent rolled out its single carrier 100Gbps system," says Perrin in a Heavy Reading research note. "We believe that Alcatel-Lucent was the market leader in 100Gbps transport in 2011."

Other suppliers, including Cisco Systems and Huawei, have also announced single-carrier 100Gbps, and more single-wavelength 100Gbps announcements will come throughout 2012.

Heavy Reading believes the ability to scale to 400Gbps is important, as is the use of multiple carriers (or super-channels). But 400 Gigabit and 1 Terabit transport are still years away and 100Gbps transport will be the core networking technology for a long time yet.

"The vendors with the best 100G systems will be best-positioned to capture share over the next five years, we believe," says Perrin.

Ron Kline, principal analyst for Ovum’s network infrastructure group.

For Ron Kline, Ciena's announcement was less of a surprise. Ciena showcased WaveLogic 3's to analysts late last year. The challenge with such a technology announcement is understanding the capabilities and how it will be rolled out and used within a product, he says.

"Ciena's WaveLogic 3 is the basis for 400 Gig," says Kline. "They are not out there saying 'we have 400 Gig'." Instead, what the company is stressing is the degree of added capacity, intelligence and flexibility that WaveLogic 3 will deliver. That said, Ciena does have trials planned for 400 Gig this year, he says.

What is noteworthy, says Ovum, is that 400Gbps is within Ciena's grasp whereas there are still some vendors yet to record revenues for 100Gbps.

"Product differentiation has changed - it used to be about coherent," says Kline. "But now that nearly all vendors have coherent, differentiation is going to be determined by who has the best coherent technology."

Challenges, progress & uncertainties facing the optical component industry

In recent years the industry has moved from direct detection to coherent transmission and has alighted on a flexible ROADM architecture. The result is a new level in optical networking sophistication. OFC/NFOEC 2012 will showcase the progress in these and other areas of industry consensus as well as shining a spotlight on issues less clear.

Optical component players may be forgiven for the odd envious glance towards the semiconductor industry and its well-defined industry dynamics.

The semiconductor industry has Moore’s Law that drives technological progress and the economics of chip-making. It also experiences semiconductor cycles - regular industry corrections caused by overcapacity and excess inventory. The semiconductor industry certainly has its challenges but it is well drilled in what to expect.

Optical challenges

The optical industry experienced its own version of a semiconductor cycle in 2010-11 - strong growth in 2010 followed by a correction in 2011. But such market dynamics are irregular and optical has no Moore's Law.

Optical players must therefore work harder to develop components to meet the rapid traffic growth while achieving cost efficiencies, denser designs and power savings.

Such efficiencies are even more important as the marketplace becomes more complex due to changes in the industry layers above components. The added applications layer above networks was highlighted in the OFC/NFOEC 2012 news analysis by Ovum’s Karen Liu. The analyst also pointed out that operators’ revenues and capex growth rates are set to halve in the years till 2017 compared to 2006-2010.

Such is the challenging backdrop facing optical component players.

Consensus

Coherent has become the defacto standard for long-haul high-speed transmission. Optical system vendors have largely launched their 100Gbps systems and have set their design engineers on the next challenge: addressing designs for line rates beyond 100Gbps.

Infinera detailed its 500Gbps super-channel photonic integrated circuit last year. At OFC/NFOEC it will be interesting to learn how other equipment makers are tackling such designs and what activity and requests optical component vendors are seeing regarding the next line rates after 100Gbps.

Meanwhile new chip designs for transport and switching at 100Gbps are expected at the show. AppliedMicro is sampling its gearbox chip that supports 100 Gigabit Ethernet and OTU4 optical interfaces. More announcements should be expected regarding merchant 100Gbps digital signal processing ASIC designs.

An architectural consensus for wavelength-selective switches (WSSes) - the key building block of ROADMs - are taking shape with the industry consolidating on a route-and-select architecture, according to analysts.

Gridless - the ROADM attribute that supports differing spectral widths expected for line rates above 100Gbps - is a key characteristic that WSSes must support, resulting in more vendors announcing liquid crystal on silicon designs.

Client-side 40 and 100 Gigabit Ethernet (GbE) interfaces have a clearer module roadmap than line-side transmission. After the CFP comes the CFP2 and CFP4 which promise denser interfaces and Terabit capacity blades. Module form factors such as the QSFP+ at 40GbE and in time 100GbE CFP4s require integrated photonic designs. This is a development to watch for at the show.

Others areas to note include tunable-laser XFPs and even tunable SFP+, work on which has already been announced by JDS Uniphase.

Lastly, short-link interfaces and in particular optical engines is another important segment that ultimately promises new system designs and the market opportunity that will unleash silicon photonics.

Optical engines can simplify high-speed backplane designs and printed circuit board electronics. Electrical interfaces moving to 25Gbps is seen as the threshold trigger when switch makers decide whether to move their next designs to an optical backplane.

The Optical Internetworking Forum will have a Physical and Link Layer (PLL) demonstration to showcase interoperability of the Forum’s Common Electrical Interface (CEI) 28Gbps Very Short Reach (VSR) chip-to-module electrical interfaces, as well as a demonstration of the CEI-25G-LR backplane interface.

Companies participating in the interop include Altera, Amphenol, Fujitsu Optical Components, Gennum, IBM, Inphi, Luxtera, Molex, TE Connectivity and Xilinx.

Altera has already unveiled a FGPA prototype that co-packages 12x10Gbps transmitter and receiver optical engines alongside its FPGA.

Uncertainties

OFC/NFOEC 2012 also provides an opportunity to assess progress in sectors and technology where there is less clarity. Two sectors of note are next-generation PON and the 100Gbps direct-detect market.

For next-generation PON, several ideas are being pursued, faster extensions of existing PON schemes such as a 40Gbps version of the existing time devision multiplexing PON schemes, 40G PON based on hybrid WDM and TDM schemes, WDM-PON and even ultra dense WDM-PON and OFDM-based PON schemes.

The upcoming show will not answer what the likely schemes will be but will provide an opportunity to test what the latest thinking is.

The same applies for 100 Gigabit direct detection.

There are significant cost advantages to this approach and there is an opportunity for the technology in the metro and for data centre connectivity. But so far announcements have been limited and operators are still to fully assess the technology. Further announcements at OFC/NFOEC will highlight the progress being made here.

The article has been written as a news analysis published by the organisers before this year's OFC/NFOEC event.

Photonic integration specialist OneChip tackles PON

Briefing: PON

Part 1: Monolithic integrated transceivers

OneChip Photonics is moving to volume production of PON transceivers based on its photonic integrated circuit (PIC) design. The company believes that its transceivers can achieve a 20% price advantage.

"We will be able to sell [our integrated PON transceivers] at a 20% price differential when we reach high volumes"

Andy Weirich, OneChip Photonics

OneChip Photonics has already provided transceiver engineering samples to prospective customers and will start the qualification process with some customers this month. It expects to start delivering limited quantities of its optical transceivers in the next quarter.

The company's primary products are Ethernet PON (EPON) and Gigabit PON (GPON) transceivers. But it is also considering selling a bi-directional optical sub-assembly (BOSA), a component of its transceivers, to those system providers that want to attach the BOSA directly to the printed circuit board (PCB) in their optical network units (ONUs).

"The BOSA is the sub-assembly that contains all the optics, usually the TIA [trans-impedance amplifier] and sometimes the laser driver," says Andy Weirich, OneChip Photonics' vice president of product line management.

The company will roll out its Ethernet PON (EPON) ONU transceivers in the second quarter of 2012, followed by GPON ONU transceivers in the third quarter.

PON Technologies

EPON operates at 1.25 Gigabit-per-second (Gbps) upstream and downstream. OneChip had planned to develop a 2.5Gbps EPON variant which, says OneChip, has been standardised by the China Communications Standards Association (CCSA). But the company has abandoned the design since volumes have been extremely small and there have been no deployments in China.

GPON is a 2.5Gbps downstream/ 1.25Gbps upstream technology. The main differences between GPON and EPON transceiver optical components are the requirement of the ONU's receiver optics and circuitry, and the laser type, says Weirich. GPON's Class B+ specification, used for nearly all the GPON deployments, calls for a 28-29dB sensitivity. This is a more demanding specification requirement to meet than EPON's. GPON also calls for a Distributed Feedback (DFB) laser, whereas an EPON ONU may use either a Fabry-Perot laser or a DFB laser.

OneChip uses the same DFB for GPON and EPON ONUs. Where the PIC designs differ is the receiver assembly where GPON requires amplification. This, says Weirich, is achieved using either an avalanche photodiode (APD) or a semiconductor optical amplifier (SOA).

OneChip will start with an APD but will progress to an SOA. Once it integrates an SOA as part of the PIC, a simpler, cheaper photo-detector can be used.

Weirich admits that it has taken OneChip longer than it expected to develop its monolithically-integrated design.

Part of the challenge has been the issue of packaging the PIC. "Because of our integrated approach and non-alignment-requiring assembly, we have had to solve a few more technology problems," he says. "Our suppliers have had a challenge with some of those issues, and it has taken a couple of iterations to solve."

OneChip says that the good news is that the price erosion of EPON transceivers has slowed down in the last two years. So while Weirich admits the market is more competitive now, what is promising is that volumes have continued to grow.

"There is no sign of saturation happening either in the EPON or GPON markets," he says. And OneChip believes it can compete on price. "What we are saying is that we will be able to sell [our monolithically integrated PON transceivers) at a 20% price differential when we reach high volumes." That is because the monolithic design is simpler and the optical components that make up the design are cheaper, says the company.

10G EPON and XGPON

OneChip believes the end of 2012 will be when 10G EPON volumes start to ramp. "10G EPON is a significantly larger market than 10G GPON [XGPON]," says Weirich, pointing out that some of the largest operators such as China Telecom have backed 10G EPON.

With 10G EPON there are two flavours: the asymmetric (10Gbps downstream and 1.25Gbps upstream) and the symmetric (10Gbps bidirectional) versions.

For an asymmetric 10Gbps ONU transceiver, the laser does not need to change but the optics and electronics at the receiver do, because of the 10Gbps receive signal and because operators want 28-29dB optical link budgets so that 10G EPON can run on the same fibre plant as EPON. "This is an order of magnitude more difficult from a sensitivity perspective than for EPON," says Weirich.

There is demand for the 10G symmetric EPON but it is much lower than the asymmetric version primarily due to cost. "The ONU transceiver with its 10 Gbps laser and photo-detector is quite a bit more costly," says Weirich, complicating the PON's business case.

OneChip says it has a 10G EPON in its product roadmap, but it has not yet made any announcements or made any demonstrations to customers.

Challenges

OneChip is not aware of any other company developing a monolithic integrated design for PON transceivers, in part due to the challenge. It has to be made cheaply enough to compete with the traditional TO-can design. The key is to develop low-cost integration techniques and processes right at the start of the PIC design, he says.

The company says that it is also exploring using its PIC technology to address data centre connectivity.

OneChip Photonics at a glance

OneChip employs some 80 staff and is headquartered in Ottawa, Canada, where it has a 4,000 sq. ft. cleanroom. The start-up also has a regional office in Shenzhen, China which includes a test lab to serve regional customers.

The company is primarily a transceiver supplier and its main target customers are the tier-one system vendors that supply OLT and ONU equipment. "When you think of the big three players in China, Huawei, ZTE and Fiberhome would be among those we are targeting," says Steve Bauer, vice president of marketing and communications, as well as players such as Alcatel-Lucent and Motorola. As mentioned, the company is also considering selling its BOSA design to ONU makers.

In May 2011 the company received $18M in its latest round of funding. "We are transitioning from product development to becoming operationally ready to manufacture in volume," says Bauer.

Fabrinet and Sanmina-SCI are two contract manufacturers that the company is using for transceiver testing and assembly while it has partnerships with several other fabs for supply of wafers, wafer fabrication and silicon optical benches.